More Wise Words from Warren

Published February 29, 2024

Jeremy Schwartz, CFA

Global Chief Investment Officer

Warren Buffett’s annual letter is always rich in history, stories and lessons worth heeding.

Four of my favorite passages this year deal with familiar topics to readers of our blog:

1. Quality investing versus value investing

2. A focus on high-quality, long-term dividend growers

3. The Japan value thesis and the importance of not betting on currencies, i.e., the case for hedging FX

4. The gambling culture expanding in stock trading

1. The True Architect of the Quality Investing Style: Warren’s Pivot from Value

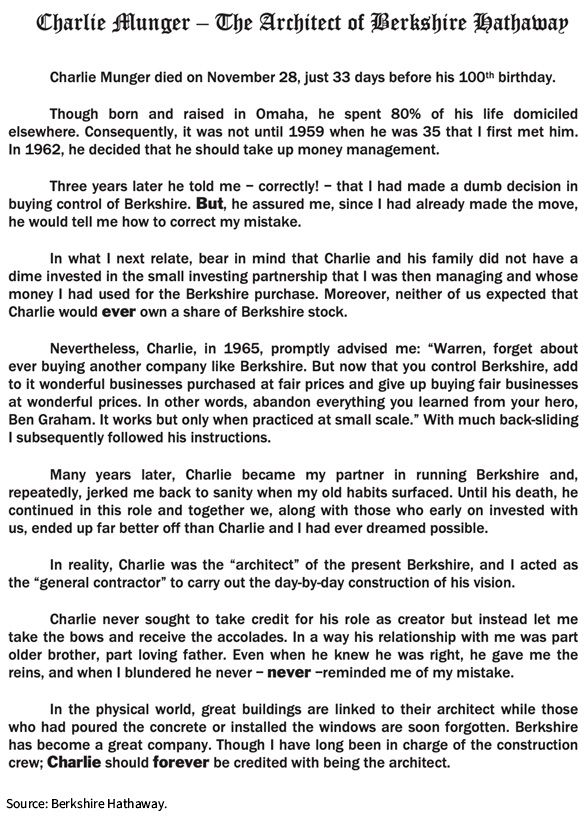

The first passage of Warren’s letter I snipped in its entirety was a tribute to Charlie Munger. Warren refers to Charlie as the architect of Berkshire Hathaway.

Warren repeats one of my favorite passages on quality investing: buying ‘fair businesses’ at value prices is inferior to a strategy of buying high-quality businesses at fair prices.

Warren attributes this foundational idea, which is Berkshire’s current ethos, to Charlie, who convinced Warren to move beyond the classic Ben Graham value discipline. The real long-term winners at Berkshire were not traditional low-priced value stocks but the high-quality and growing franchises.

When I first started investigating dividend investing with Jeremy Siegel, we did it from the lens of a value investor focusing on higher-dividend-yielding baskets.

But over 10 years ago, WisdomTree made a similar quality pivot when we launched our quality dividend growth Index franchise, and now our flagship Fund (WisdomTree U.S. Quality Dividend Growth Fund, DGRW) has over $11 billion in assets and is our largest equity ETF. We’ve since expanded the quality focus to small caps, international markets and even a non-dividend paying universe.

But half of the ranking system for DGRW I have often described as the Buffett factor, which focuses on high ROE businesses using little debt to drive up that ROE (which is why we included ROA in the selection process as well).

Buffett’s homage to Munger in this year’s letter leaves no doubt all quality investors must stand united and refer to Charlie Munger as the original architect of the quality investing style, while Buffett was the world’s best general contractorfor this factor.

2. The Importance of Long-Term Dividend Growers Is Related to Quality Investing

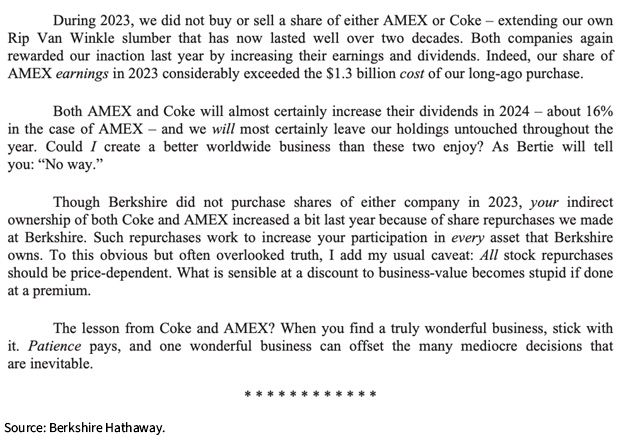

Last year, we highlighted the dividend growth prominent in American Express and Coca-Cola, two companies Berkshire has held over the last 30 years.

In this year’s letter, Warren again emphasized the importance of the long-term dividend compounding that comes from these high-quality businesses.

Our piece summarizing why our quality dividend growth Indexes have held exposure to these same stocks is linked here.

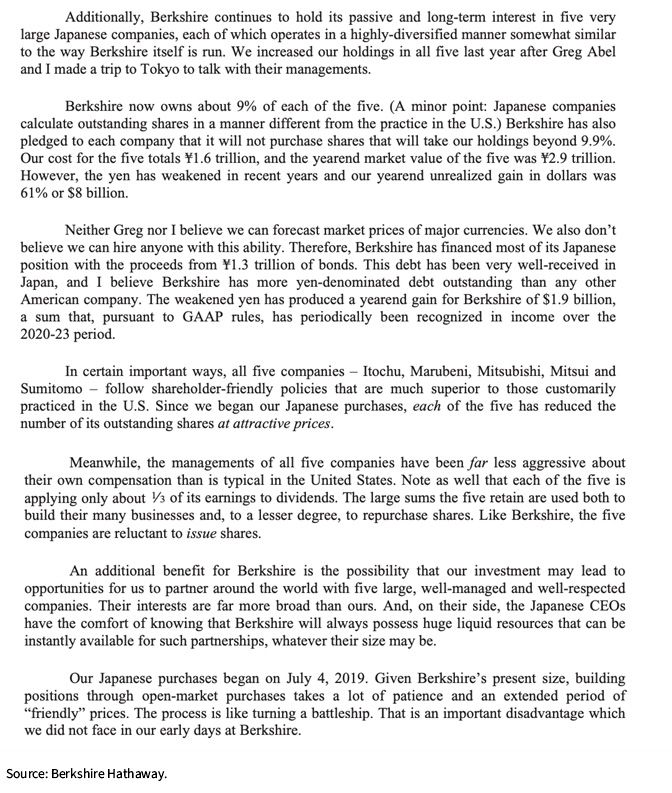

3. Japan Remains a Top Idea Outside the U.S.

My team has authored at least four separate pieces—starting in September 2020 after Berkshire’s purchases first became public—to follow Warren into the Japan trade (1st, 2nd, 3rd and 4th).

When Warren first issued yen-denominated debt to finance his Japanese equity purchases, his motives were not clear. But the latest letter clarifies his decision: Warren doesn’t think anyone has the ability to predict currency movements, so he wanted to neutralize his exposure.

It is a good thing he did: Berkshire gained almost $2 billion from hedging the yen. Since his first purchases in 2019, the yen’s weakness would have subtracted from the results of picking good stocks. We believe investors habitually make a big mistake by always betting on the U.S. dollar’s demise and taking on foreign currency risk like they do.

Plus, in Japan, U.S. investors earn over 5% to hedge the yen due to prevailing interest rate differentials. You can execute a strategy similar to Buffet’s decision to issue yen bonds by using WisdomTree’s currency-hedged ETFs.

More broadly, Buffett acknowledges that many things can go wrong on an investment thesis, and he doesn’t want to let currency be that issue.

We still like Japan as a top idea for investing outside the U.S. And while many want to say the yen looks cheap and it is time to go unhedged, we’d remind you of Warren’s point:

“Neither Greg nor I believe we can forecast market prices of major currencies. We also don't believe we can hire anyone with this ability.”

More allocators should follow his lead and stay neutral on currencies rather than trying to time it or remaining unhedged. Remember, unhedged exposure is a perpetual bet that the dollar will weaken versus the yen.

4. The Gambling Culture Today in Stock Trading

While many believe the market is becoming more efficient and harder to beat over time (and the evidence shows active managers are struggling to keep up with passive, and flows are increasingly going passive), Buffett believes the emotional tendencies of the market, in some ways, are getting worse.

Though the stock market is massively larger than it was in our early years, today’s active participants are neither more emotionally stable nor better taught than when I was in school. For whatever reasons, markets now exhibit far more casino-like behavior than they did when I was young. The casino now resides in many homes and daily tempts the occupants.

For those investors who stay grounded in Warren’s wise words, strategies like our quality dividend growth focus can help them stick to long-term, prudent strategies that try to capitalize on the casino-like mentality that causes stocks to deviate from fair value. Market prices are not so efficient. They are noisy, and we think rebalancing back to a concept of relative value will be rewarded over the long run.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Related Video

Related articles

Rules Over Headlines: WisdomTree’s Approach to Growth Investing

Japan Is Back

Built for Any Market: How Blending Growth and Value Creates a Stronger Core

Dividend Growth Is Not One Strategy

Quality as a Foundation in an Uncertain World

From Trading Houses to Tokio Marine: Buffett’s Expanding Bet on Japan

A Playbook for the Currency Opportunity in Today’s Market

The Company at the Center of the AI Economy

A Dog, a Diagnosis and a Different Way to Understand AI

About the contributor

Jeremy Schwartz, CFA

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.