Shelter From the Storm?

Published March 1, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Last week, I blogged on the theme of the recent shifting narrative in the money and bond markets. One of the key catalysts behind this changing dynamic came from two inflation readings (CPI & PPI), which revealed that the ‘cooling’ effect that had been on display in Q4, had been dialed back a bit to begin 2023. Well, now we can add the Fed’s preferred inflation gauge to the conversation as well.

For the record, this preferred measure is known as the Personal Consumption Expenditure Price Index (PCEPI). For January, the year-over-year rates for both the overall and core measures actually increased by 0.4pp each, to 5.4% and 4.7%, respectively. Needless to say, this news only provided more fuel to the aforementioned narrative shift, pushing Treasury yields higher, accordingly.

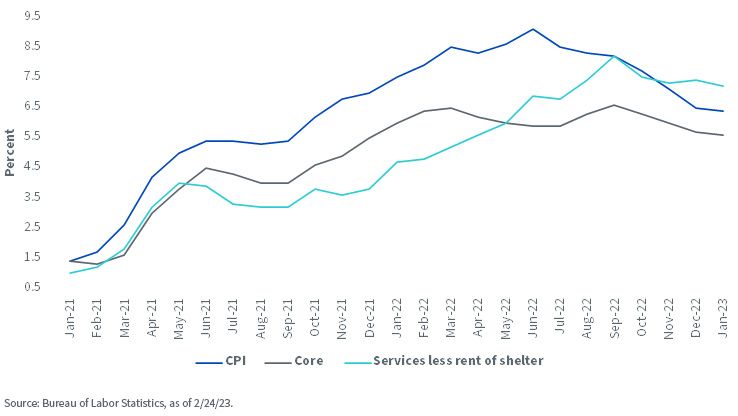

CPI Gauges – 12-month % Change

Interestingly, market conversation had been turning toward a ‘disinflation’ theme prior to these latest readings on price pressures. For the sake of simplicity, this blog post is going to focus exclusively on trends within the most widely followed inflation measure, CPI. The first graph highlights why market participants were cheered by the notion that price pressures had finally reached an apex and were beginning to come down in a visible fashion.

After reaching a peak reading of 9.1% in June, the year-over-year increase for overall CPI had fallen to 6.5% to end 2022. Although not as formidable, the core measure also revealed a declining trend as the annualized gain declined from a high of 6.6% to 5.7%.

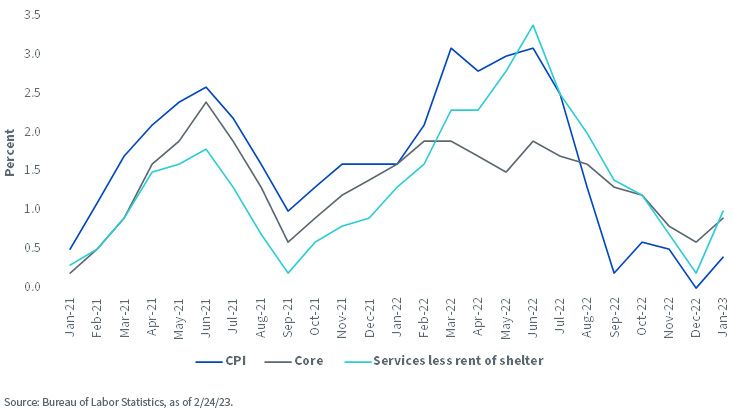

CPI Gauges – 3-month % Change

This takes us to where we may be headed. While progress was being made on the core inflation front, it appeared to have a more ‘sticky’ component to it. One of the key points centered around how the Bureau of Labor Statistics (BLS) measures housing, or shelter costs. Indeed, a compelling argument was being made that the BLS data overestimated housing inflation. As a result, the ‘services less rent of shelter’ component within the CPI release began to garner more attention. Looking at inflation from a three-month interval perspective, there was a definitive downward trajectory to this category prior to the January 2023 report, which reinforced the ‘overestimating’ case. To be sure, the three-month change plunged from 3.4% in June to only a scant 0.2% in December. Interestingly, this component reversed course completely to open 2023 by rising 1%.

Conclusion

Where does that leave us? While inflation does appear to have peaked last summer, unfortunately for the Fed, and by extension the bond market, the future road may not be as much of a one-way street to the downside as we saw during the autumn months. Nevertheless, a continued broader cooling in price pressures still remains a reasonable case scenario. However, against this backdrop, the Fed will continue to operate under the assumption it ‘has more work to do’.

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.