DDWM

Dynamic International Equity Fund

Published March 25, 2024

Director of Modern Alpha

In the complex world of global investing, currency risk plays a significant role. When investors allocate funds to foreign equities, they implicitly expose themselves to foreign exchange fluctuations. Currency hedging strategies aim to mitigate this risk while preserving the original equity exposure.

At times, distinguishing risk enhancements stemming from currency movements from those originating from stock portfolios can be challenging. Within our suite of offerings, we present three distinct strategies where the equity portfolio remains the same, and the sole variation is the currency approach.

This transparency provides investors with a concise view of the impact of currency hedging. In general, whether dynamically managed or fully hedged, currency hedging has consistently reduced overall portfolio risk.

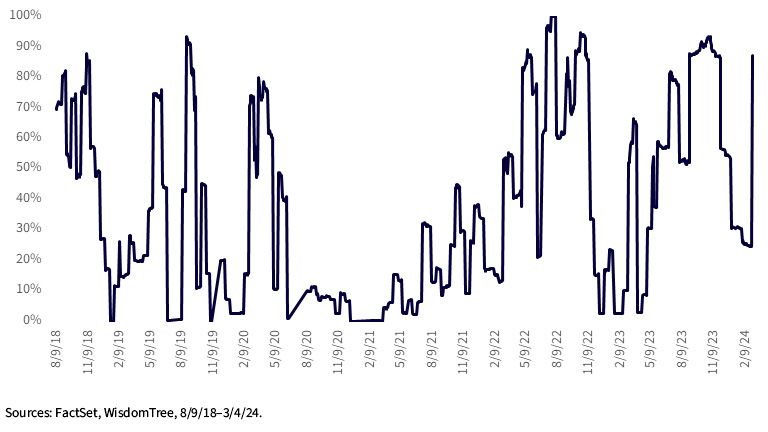

At WisdomTree, we employ bottom-up factor-based strategies (such as momentum and low volatility) for our active currency hedging models. Over the long term, our dynamic currency model has consistently added value. While the alpha generated by the currency model may vary in shorter time periods, one consistent trend remains: dynamic currency hedging effectively reduced portfolio risk.

Let’s examine two specific scenarios:

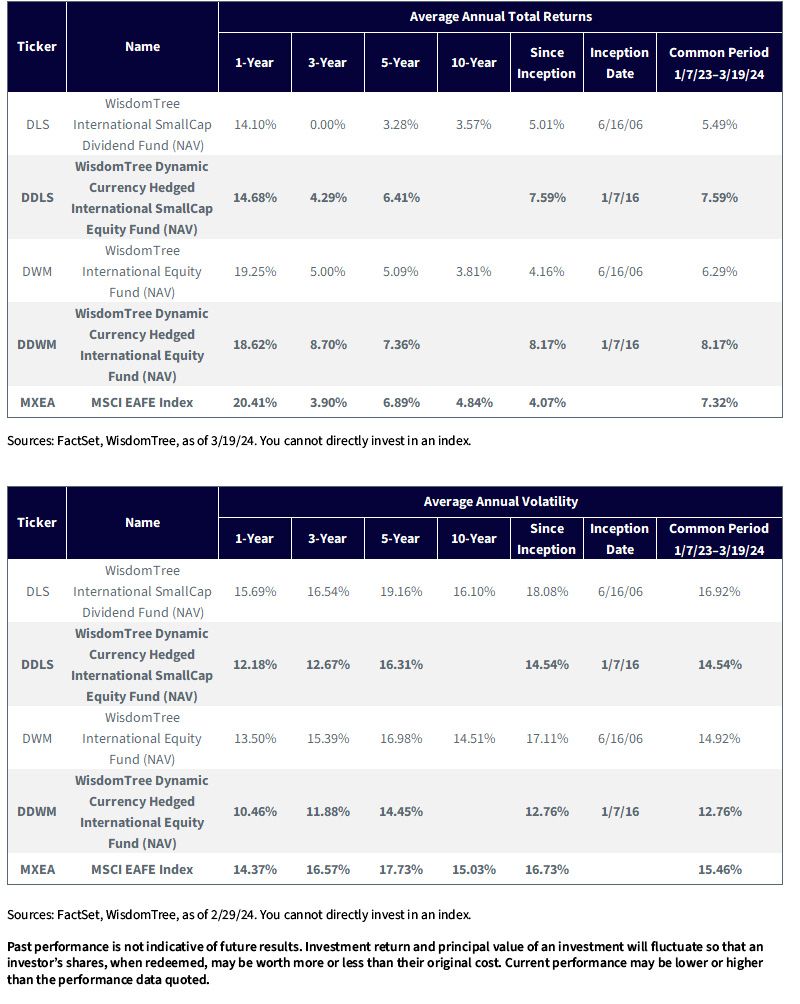

1. International Dividend-Weighted Large-Cap ETFs:

2. International Smaller-Cap ETFs:

For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: DLS, DDLS, DWM, DDWM.

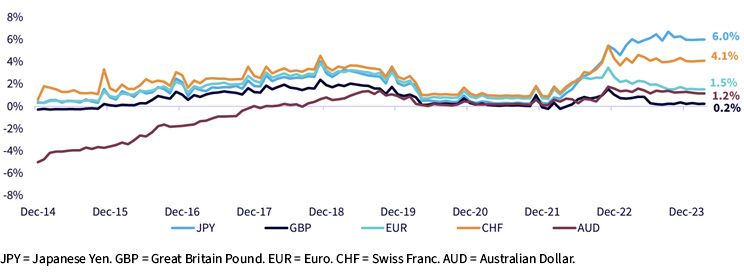

In the current geopolitical environment, adding a weak dollar bet via your foreign equity exposures is no longer necessarily the best baseline allocation. Rather, a strong dollar could become a headwind to U.S. earnings—and so adding more long U.S. dollar exposures is a more interesting diversifier.

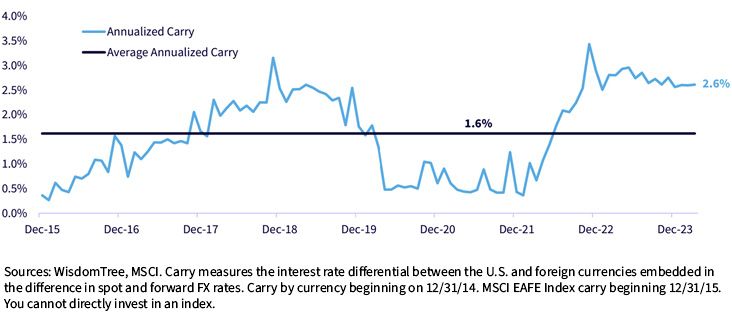

Currently, even as the U.S. is expected to lower interest rates, the 2.6% interest rate differential (carry) earned by hedging will be lowered but continue to be positive for a while.

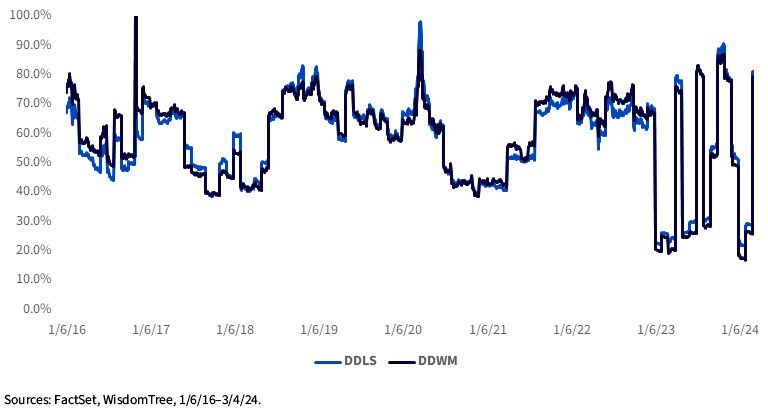

Historically, momentum tends to be the strongest factor in currency hedging. Our revamped dynamic currency model has about 60% weight in the momentum factor for both developed and emerging markets.

For the international developed universe, the weight of the momentum factor is higher from 2023, resulting in more varied hedge ratios. However, the currency overlay continued to reduce portfolio risk after the revamp, even as more momentum was introduced for the hedge ratio itself.

Prior to the revamp, the dynamic emerging markets currency model also heavily relied on the momentum factor. Consequently, the volatility of the portfolio hedge ratio was similar before and after 2023.

In summary, the risk reduction of currency hedging was evident across the board, in our other currency-hedged strategies, such as the WisdomTree Japan Hedged Equity Fund (DXJ), the WisdomTree International Hedged Quality Dividend Growth Fund (IHDG), the dynamic currency hedging WisdomTree International Multifactor (DWMF) and Emerging Markets Multifactor (EMMF) Funds.

Macro currency calls are harder to incorporate into a systematic portfolio, thus in most active currency spaces, we’ve stuck with a factor-based active model to capture some benefits of dynamic currency hedging. And we recommend clients consider some exposure to currency hedging strategies to reduce portfolio risk in this uncertain environment.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty.

DWM: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DDWM: The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. A Fund that has exposure to one or more sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from one or more third parties, and the Index may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DLS: Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DDLS: The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. A Fund that has exposure to one or more sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. The composition of the Index underlying the Fund is heavily dependent on quantitative models and data from one or more third parties, and the Index may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Director of Modern Alpha

Liqian Ren, Ph.D., joined WisdomTree as Director of Modern Alpha in 2018. She leads WisdomTree’s quantitative investment capabilities and serves as a thought leader for WisdomTree’s Modern Alpha® approach. Liqian was previously at Vanguard, where she worked for 12 years, most recently as a portfolio manager in the Quantitative Equity Group managing Vanguard’s active funds and conducting research on factor strategies. Prior to joining Vanguard, she was an associate economist at the Federal Reserve Bank of Chicago. Liqian received her bachelor’s degree in Computer Science from Peking University in Beijing, her master’s in Economics from Indiana University—Purdue University Indianapolis, and her MBA and Ph.D. in Economics from the University of Chicago Booth School of Business. Liqian co-hosts a podcast on China and Asian markets with Jeremy Schwartz, WisdomTree’s Global Head of Research, and she is a co-host on the Wharton Business Radio program Behind the Markets on SiriusXM 132.