Reviewing Our Exposure to Small and Mid-Cap Regional Banks

Published March 22, 2024

Equity Strategist

Though U.S. equity markets are at all-time highs, regional banks remain mired in the fallout from last year’s crisis that felled several companies in dramatic fashion.

Silicon Valley Bank’s failure in March 2023 stoked panic selling across the sector amid fears of contagion and prompted scrutiny of other banks’ liquidity positions and asset-liability profiles.

Today, commercial real estate exposures are the preeminent concern, and markets remain deeply unsettled. The latest irritant contaminating sentiment is New York Community Bank, which needed a $1 billion capital injection from a consortium of outside investors to keep it afloat. It installed a new CEO and created several new board seats for the investor group as a result. Its shares are on life support after falling 67%1 to start the year.

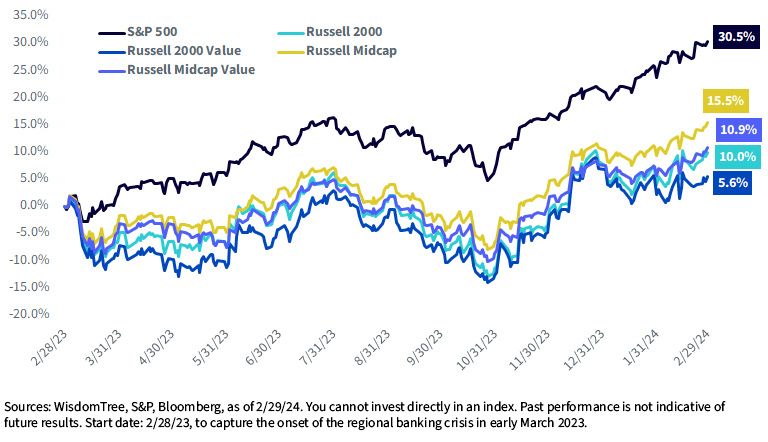

The KBW Regional Banking Index and S&P Regional Banks Select Industry Index have each fallen by about 15% since the onset of the crisis last March.1 Meanwhile, the S&P 500 is up 30%, demonstrating the severity of markets’ concerns about the health of the regional banking system.

Poor sentiment remains a headwind for small and mid-cap equity indexes, which have notable allocations to regional banks, despite broader equity market strength. The Russell 2000 and 2000 Value Indexes (up 10% and 5.6%, respectively) are still lagging large caps by more than 20% over the last year. Mid-caps have barely fared any better with the Russell Midcap and Midcap Value indexes up 15.5% and 10.9% over the same period.

U.S. Large Caps Have Been the Most Reliable Market Since the 2023 Regional Banking Crisis

Despite the pessimism pervading the industry, we believe there are still ways to maintain exposure to regional banks within small and mid-cap equity allocations without suffering drastically poor performance or sacrificing business quality.

But we also understand that headline risks influence market narratives and direction, so it’s important to review the composition of WisdomTree’s small and mid-cap products to identify and understand existing exposures.

Company Nightmares Had Little Impact

Among the banks that made headlines in 2023, we had minimal exposure to PacWest Bancorp (PACW) and Signature Bank (SBNY) within the WisdomTree U.S. MidCap (EZM), U.S. MidCap Dividend (DON) and U.S. SmallCap Dividend (DES) Funds, resulting in negligible performance impacts during the crisis.

Neither Silicon Valley Bank (formerly SIVB) nor First Republic Bank (formerly FRC) was held in any WisdomTree small-cap or mid-cap product when they failed and had not been in eight years.

The most recent headache, New York Community Bancorp (NYCB), is held within EZM and DON and has obviously weighed on performance, but not as much as the collapse in share price might suggest.

Market-Like Exposures within WisdomTree Small Caps

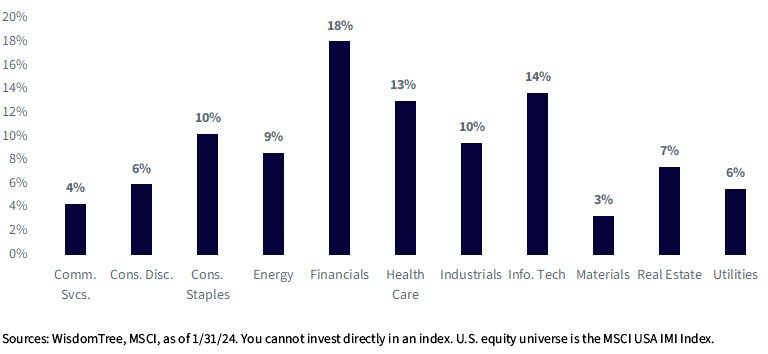

Banks often exhibit characteristics synonymous with value investing, including low price-to-earnings (P/E) multiples and large dividend payments. Financials usually pay the largest proportion of dividends among U.S. sectors, often dwarfing other heavyweight payers like Health Care and Information Technology by 4% to 5%.

Sector Contribution to Dividend Stream- MSCI USA IMI Index

As a result, value indexes tend to have larger exposures to banks than those predicated on other investment styles.

WisdomTree’s three oldest U.S. small-cap Indexes also skew toward value by emphasizing similar fundamentals, like earnings and dividends, that ultimately place banks in the same category.

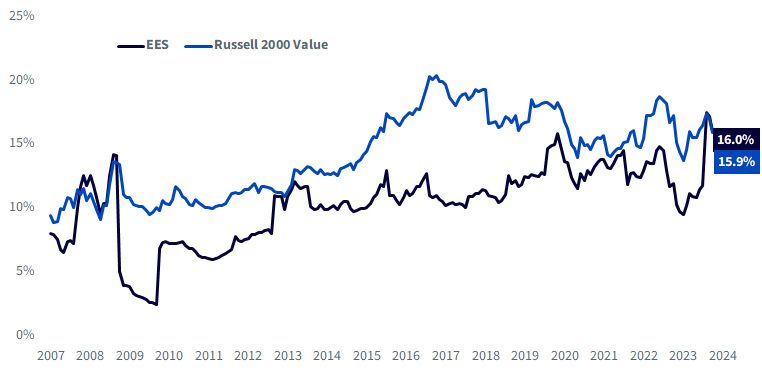

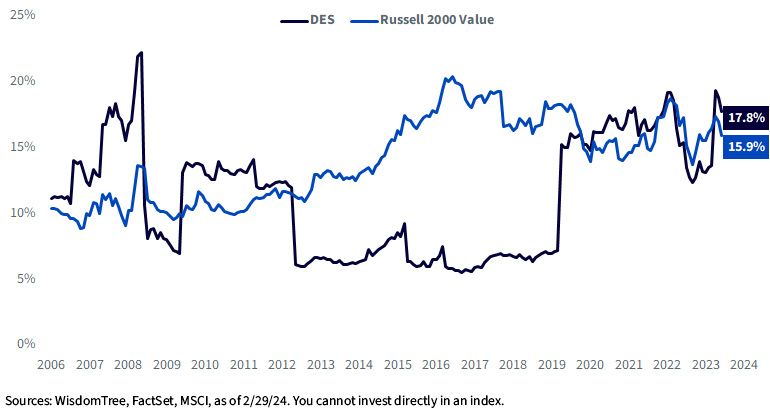

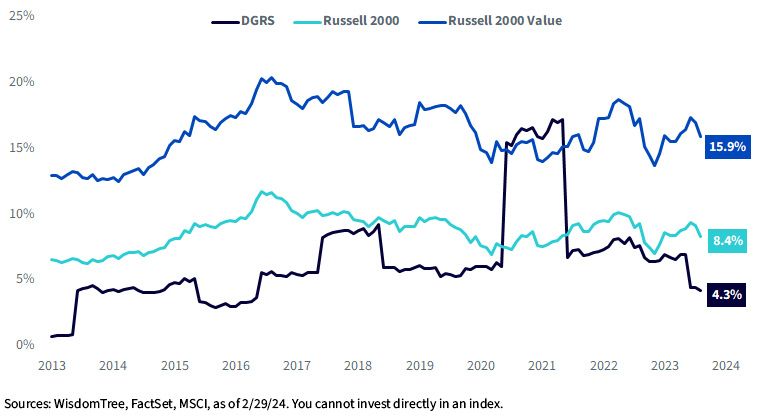

Both the earnings-weighted WisdomTree U.S. SmallCap Fund (EES) and dividend-weighted DES exhibit market-like regional bank exposures today, though they’ve historically been under-weight in the Russell 2000 Value Index.

Weight in Regional Banks over Time: EES vs. Russell 2000 Value

Weight in Regional Banks over Time: DES vs. Russell 2000 Value

The recent pickups resulted from our annual rebalance process in December 2023, and reflect regional banks’ growing proportion of aggregate earnings and dividends among U.S. small caps, despite headline noise concerning specific companies.

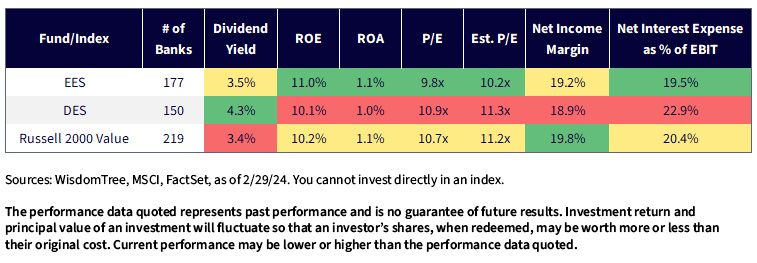

Among the regional banks within DES, dividends are the primary feature. Collectively, they offer nearly 100 basis points of additional yield over those in the Russell 2000 Value while approximating the Russell index across most other metrics.

EES's regional banks, which are earnings-weighted, result in a higher quality composite than those in the Russell 2000 Value. There’s a notable improvement in earnings and return on equity (ROE) that reduces prevailing P/E multiples by about one point each. It also shaves a percentage point off banks’ aggregate net interest expense as a percentage of EBIT, perhaps signaling a healthier debt burden.

Small Caps—Weighted Average Fundamentals of Regional Banks in Each Fund/Index

For the most recent month-end standardized performance, please the respective ticker: EES, DES.

WisdomTree’s High-Quality Small Caps Are an Exception

The WisdomTree U.S. SmallCap Quality Dividend Growth Fund (DGRS), however, introduces another component that indirectly reduces regional bank exposures relative to the broader market. DGRS systematically selects the top 50% companies within the dividend-paying U.S. small-cap universe with the highest quality scores. By screening for ROE and return on assets (ROA) within our quality definition, many regional banks are avoided since they tend to report high ROE but lower ROA by nature of their business.

Weight in Regional Banks over Time: DGRS vs. Russell Small Cap Indexes

By design, DGRS's regional bank exposure is regularly under-weight in the Russell 2000 and 2000 Value indexes.

The sole exception was a result of our 2020 rebalance and the additional emphasis on earnings growth estimates in our quality framework. Banks had high earnings growth estimates in the aftermath of the pandemic and were rewarded with larger allocations. This proved to be beneficial as Financials were the top sector contributor for DGRS during 2021 relative to the Russell 2000 Value Index.

Throughout its full history, however, DGRS has routinely been under-weight in regional banks by promoting high-quality small caps.

Modest Over-Weight Allocations across WisdomTree Mid-Cap Indexes

Although regional banks are not as prevalent in market cap-weighted mid-cap indexes as they are in small-cap indexes, dividend- and earnings-weighted methodologies have similar influences on overall exposures.

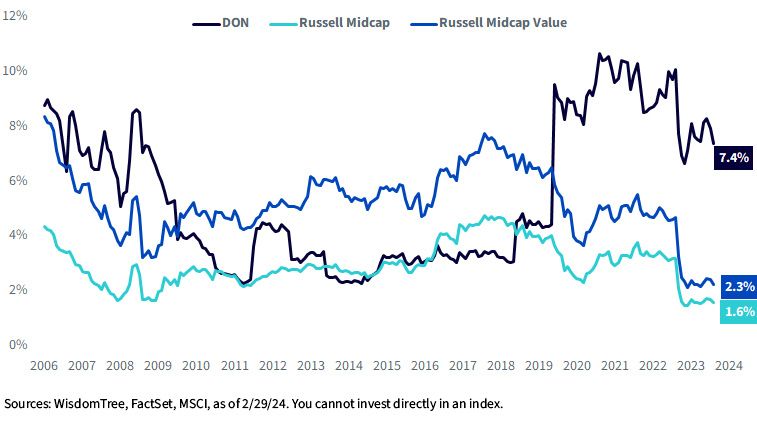

The regular over-weight allocation to regional banks within DON is a byproduct of their preference for dividends and larger relative contribution to the U.S. mid-cap Dividend Stream™.

Weight in Regional Banks over Time: DON vs. Russell Midcap Indexes

There’s a similar effect within EZM, which weights by earnings rather than dividends.

Weight in Regional Banks over Time: EZM vs. Russell Midcap Indexes

Here, over-weight allocations reflect exposure to companies already generating substantial profits within the aggregate U.S. mid-cap Earnings Stream™.

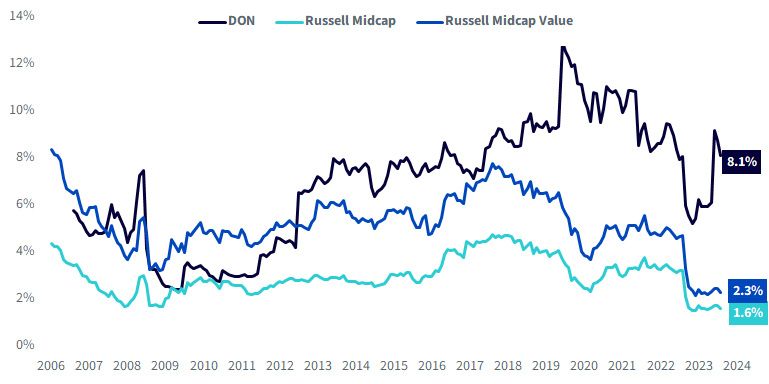

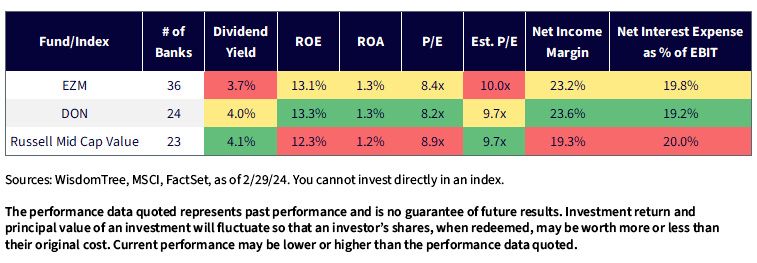

Both the dividend- and earnings-weighted approaches improve upon the fundamentals of the regional banks within the Russell Midcap Value Index, most notably in quality metrics. Each adds a bit more to ROE and ROA while reducing trailing P/Es by about half a point.

Perhaps most important, however, is the improvement in net income margin, which adds about 4% versus the market in each Index. This is paired with slight reductions in interest expenses as a percentage of EBIT, which conveys that bank exposures in each Index currently offer healthier profits with proportionally reduced financing costs.

Mid-Caps—Weighted Average Fundamentals of Regional Banks in Each Fund/Index

For the most recent month-end standardized performance, please the respective ticker: EZM, DON.

Fortunately, forward multiples are not sacrificed for these improvements, either. Estimated P/Es for the bank exposures remain similar to those of the Russell Midcap Value.

A Preference for Fundamentally Weighted Small/Mid-Caps

Overall, we believe that earnings- and dividend-weighted allocations to regional banks may be a preferred way to endure the industry’s headwinds without selling into a down market, as they offer fundamental improvements that may better insulate bank holdings from ongoing volatility.

And if investors like the valuations within the small-cap value segment of the market but want to avoid further deterioration in regional banks, the DGRS could fit that bill.

More broadly, we are optimistic on U.S. small-caps and mid-caps and overweight size within WisdomTree’s Model Portfolios, with a focus on dividend-payers and reduced multiples that were priced for recession. Consistent with Professor Siegel’s views, we anticipate broader equity market participation during 2024 (as opposed to last year’s concentrated, narrow leadership within mega-cap technology names) to be fueled by reduced probabilities of recession. The possibility of a subsequent “catch-up” rally as recession risks subside and the Fed pivots to more accommodative monetary policy helps support our upgraded view on size.

Our Model Portfolio Investment Committee (MPIC) added to DGRS at the end of 2023 to enact our views, and we’re optimistic that the marriage of size and quality will be additive in 2024.

1 Source: Bloomberg, as of 3/8/24.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

EZM/EES: Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DON/DES/DGRS: Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.