Focus on the Fed Series: Taking Stock of Fixed Income

While fixed income investors received a nice gift from the Federal Reserve in the final quarter of 2023, we think a better way to assess total returns is looking at the cumulative impact of Fed Rate hikes. On March 17, 2022, the Fed kicked off a dramatic tightening cycle from zero to 5.25%–5.50% in order to bring down inflation. In recent weeks, the focus seems to have shifted from rate hikes to rate cuts. What has this meant for markets? In part two of this series, we assess the risks in fixed income markets and discuss some of our best ideas for 2024.

Glass Half-Empty or Half-Full?

The great thing about fixed income investing is that returns often exhibit a center of gravity around yields. At the start of the Fed rate hike cycle, yields were near all-time lows. What ensued was one of the most challenging environments for fixed income investors in history. Today, we’re still at some of the highest yields we’ve seen in quite some time. Unfortunately, returns in all flavors of fixed income have underperformed cash. While we know that bond returns are inversely correlated with interest rates, returns since the Fed started hiking have resulted in meaningfully negative returns for core holdings like the Bloomberg U.S. Aggregate Bond Index (Agg). High yield generally outperformed on account of tightening credit spreads and a shorter duration than investment-grade benchmarks like the Agg.

Fixed Income Performance: 3/17/22–2/7/24

For definitions of terms in the chart above, please visit the glossary.

Drivers of Return

Bond yields across the yield curve remain higher than when the Fed started hiking. This means interest rate risk has not added value over this period. However, we feel confident that the max drawdown for fixed income has passed. The question now is how much to extend duration. This is tricky given the yield curve is still inverted, meaning that any bet in longer duration has a timing element of when yields will fall. With hindsight, we know that 5% was a good time to invest in 10-year Treasuries, but what about today? In our view, maintaining a shorter duration position could pay off should the Fed not cut rates as aggressively as the market is hoping. In the meantime, investors derive a carry benefit by investing at shorter tenors.

Impact of Credit

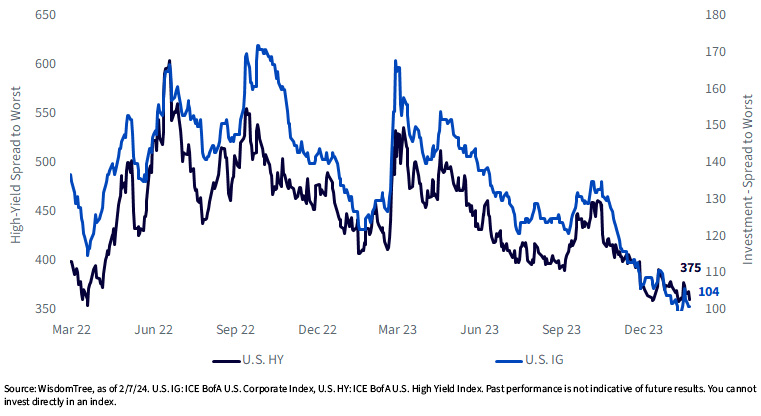

With equity markets around the world near all-time highs, it should be no surprise that credit spreads are at some of the tightest levels of the cycle. With concerns about credit generally subdued, we still like being over-weight. However, high yield may require a slightly more defensive positioning. Investors in index-based high-yield strategies are effectively betting that credit conditions will continue to improve. While this is possible, it also exposes investors to returns that are more correlated to risk markets like equities.

U.S. Credit Spreads: 3/17/22–2/7/24

For definitions of terms in the chart above, please visit the glossary.

Top Ideas

While we continue to be strong proponents of the WisdomTree Floating Rate Treasury Fund (USFR), investors looking to extend duration in a risk-conscious manner should also consider the WisdomTree U.S. Short-Term Corporate Bond Fund (SFIG). While the long end may be susceptible to bouts of volatility from the Fed, we view the shorter end of the curve as a comparatively safer bet. Additionally, while credit may not necessarily be cheap, we believe that our fundamental approach can add value should fundamentals begin to deteriorate. At 100 basis points over Treasuries, we think investment-grade corporates at the short end of the curve have the potential to outperform cash with only incremental risk in 2024.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal.

USFR: Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

SFIG: Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links