Focus on the Fed Series: Global Equities

Published February 1, 2024

Bradley Krom

U.S. Head of Research

At the end of every year, it’s important to take stock of what worked and what didn’t. However, before investors get too focused on calendar year returns, it’s also important to assess where we are with respect to monetary policy. On March 17, 2022, the U.S. Federal Reserve kicked off a dramatic tightening cycle from zero to 5.25%–5.50% in order to bring down inflation. In recent weeks, the focus has seemed to shift from rate hikes to rate cuts. What has this meant for markets? In this piece we take stock of the impact of Fed policy on global equities and share our best ideas for 2024.

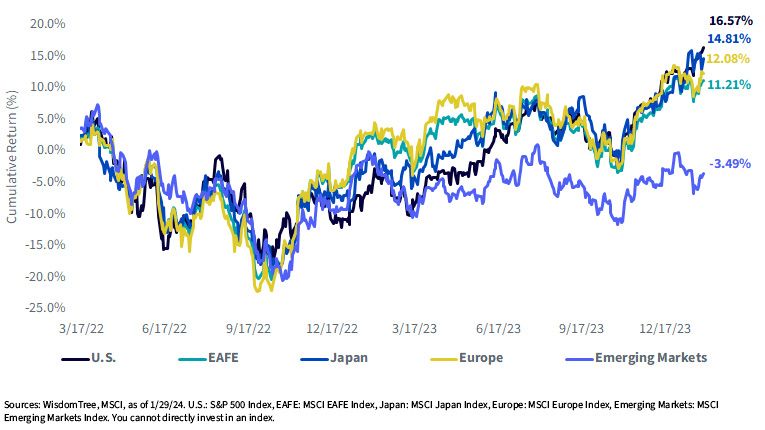

Global Equity Performance: 3/17/22–1/29/24

For definitions of terms in the graph above, please visit the glossary.

Key Takeaways

#1 Equity Returns Converge

After much hand-wringing about U.S. exceptionalism and narrow market leadership, an interesting result of looking at returns since the Fed rate hiking cycle began is a convergence in global equity returns. While the U.S. has seemingly been a persistent outperformer, many investors would be surprised to know that European equities have actually outperformed the U.S. up until the last few days for the period. Additionally, Japan (along with MSCI EAFE) generated strong returns on the back of the Fed pivot.

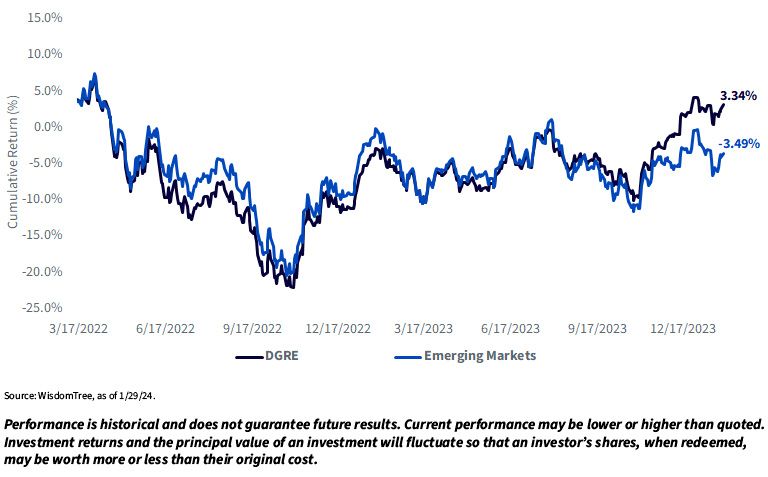

#2 Emerging Markets Languish

If we were going to focus on an outlier for equities since the Fed began its tightening cycle, it has been in emerging markets. The challenge that EM investors currently face is from concentration in Chinese stocks that have generally underperformed. Due to this risk, some of the brighter spots in global markets, like India, Taiwan and South Korea, have been masked.

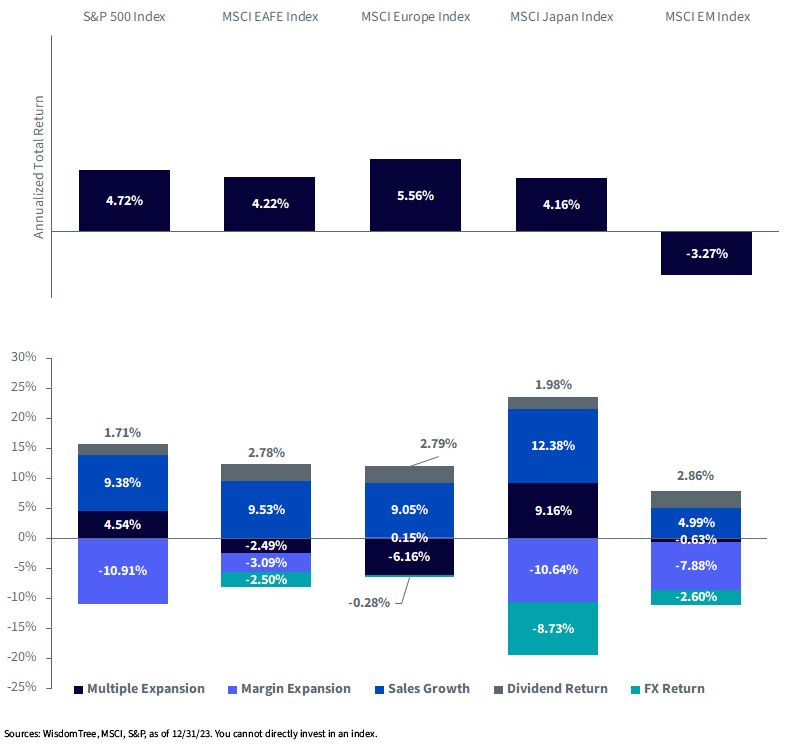

#3 Drivers of Returns Diverge

One of the most interesting facts about global equity returns has actually come from the drivers of total return. While it’s easy to get lost in headline numbers, we think looking deeper is a good idea when trying to assess where markets may be heading next. We remain favorable in our views on Japan, despite a strong year in 2023. While we remain constructive on the U.S., we are anticipating a broadening in performance into names outside of the Magnificent Seven.

Digging deeper, all developed markets generated sales growth north of 9% over the period. Japan rebound sharply, and also saw its multiples expand by nearly twice the U.S., albeit from much lower starting levels. In Europe (and EAFE), you actually saw multiples continue to contract as sentiment remained subdued. For Europe, the biggest mitigating factor is that currency served as much less of a headwind than in Japan. On average, emerging markets were a disappointment as concentration in China has led to a decline in fundamentals.

Return Attribution: 2/28/22–12/31/23

#4 Focus on FX & Valuations

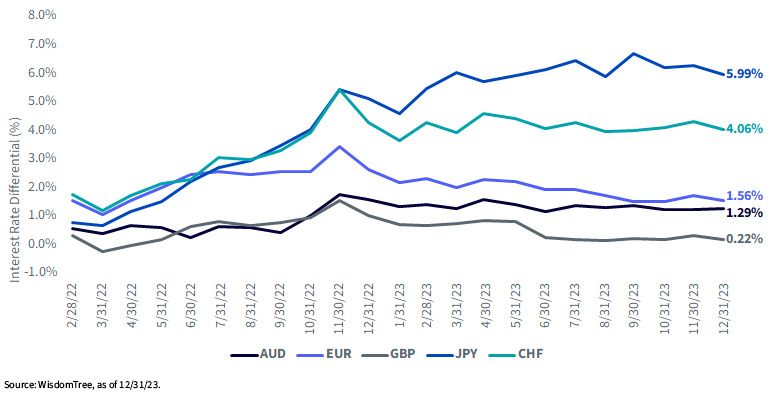

While strong returns have come from the U.S. on account of businesses generally delivering strong results, we view the potential for multiple expansion as limited. We contrast this with regions like developed international which may be in the earlier innings. Additionally, foreign currencies may be poised to strengthen after a period of broad-based dollar strength during the tightening cycle. However, there is still a meaningful advantage for U.S.-based investors to currency hedge. As we show below, the primary driver of the cost of hedging currencies is the interest rate differential. Given that U.S. rates are currently higher than other developed markets, currency hedged investors receive this difference in rates when hedging. Put another way, in order for unhedged investors to outperform hedged strategies, the foreign currencies must appreciate by more than this rate differential. In the U.K., this is quite low (0.22%), whereas in countries like Japan, this rate is nearly 6%.

U.S. vs. Foreign Carry: 2/28/22–12/31/23

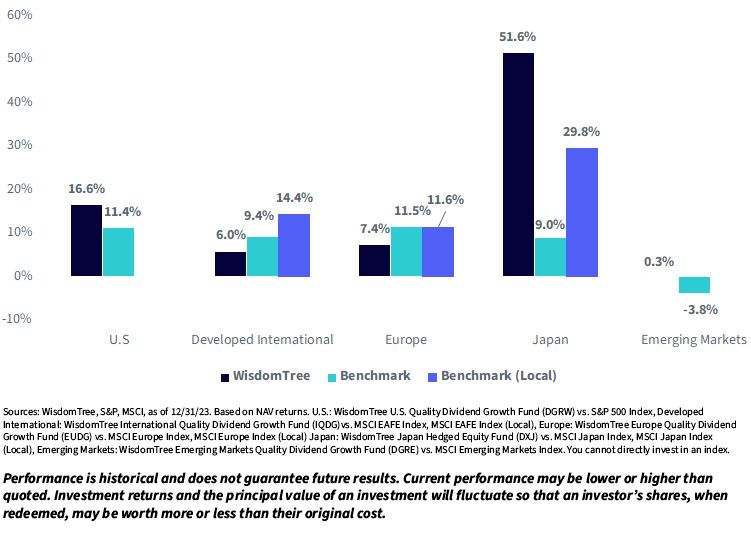

In light of these developments, some of our top ideas for 2024 revolve around Japan and quality. In Japan, we still prefer a currency hedged approach like the WisdomTree Japan Hedged Equity Fund (DXJ). While the yen may strengthen from here, it remains unclear if this level of appreciation will outstrip the significant carry advantage from hedging the yen on an annual basis. Given the potential for volatility, we still believe currency hedging makes sense in the current environment.

Fed Hikes Performance: 3/17/23–12/31/23

Performance data for the most recent quarter-end and month-end is available at the respective tickers: DGRW, IQDG, EUDG, DXJ, DGRE.

For definitions of terms in the chart above please visit the glossary.

In terms of quality, we like the idea of anchoring to the quality factor globally. In the U.S., the WisdomTree U.S. Quality Dividend Growth Fund (DGRW) remains a core holding in most of our Models. Internationally, the WisdomTree International Quality Dividend Growth Fund (IQDG) could also make sense for investors seeking to diversify away from the U.S.

EM Equity Performance: 3/17/22–1/29/24

Performance data for the most recent quarter-end and month-end is available here.

In emerging markets, quality may offer the most meaningful impact. While China could still deliver strong returns in 2024, we like the idea of maintaining core exposure to the WisdomTree Emerging Markets Quality Dividend Growth Fund (DGRE). As we discussed during our rebalance, we currently prefer to be overweight India versus China. While it has only been a few months, this decision has resulted in a meaningful uptick in returns versus the MSCI Emerging Markets Index.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal.

DXJ: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, and derivative investments, which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DGRW: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

IQDG: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Heightened sector exposure increases the Fund’s vulnerability to any single economic, regulatory or other development impacting that sector. This may result in greater share price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DGRE: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Fund’s focusing on a single sector generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than developed markets and are subject to additional risks, such as of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

EUDG: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in Europe, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Dividends are not guaranteed and a company currently paying dividends may cease paying dividends at any time. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

Two Prices, One Fund: Understanding NAV and Market Price in ETFs

Japan Is Back

When AI Leaves the Screen and Enters the Physical World

Behind the Charts: Is the Energy Trade Running Out of Fuel?

Quality as a Foundation in an Uncertain World

From Trading Houses to Tokio Marine: Buffett’s Expanding Bet on Japan

A Playbook for the Currency Opportunity in Today’s Market

The Company at the Center of the AI Economy

A Dog, a Diagnosis and a Different Way to Understand AI

About the contributor

Bradley Krom

U.S. Head of Research

Bradley Krom joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.