Does What Goes Up Have to Come Down?

Published August 23, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

For those looking for a summer respite for the bond market in August…think again. Based on trading activity as I write this, the U.S. Treasury (UST) market had something else in mind, specifically what has transpired for the UST 10-Year yield. This is a topic I blogged about a couple of weeks ago from a portfolio duration perspective. However, for this post, I wanted to get into the root causes of the recent increase in the 10-Year yield and whether it is reasonable to expect a reversal any time soon.

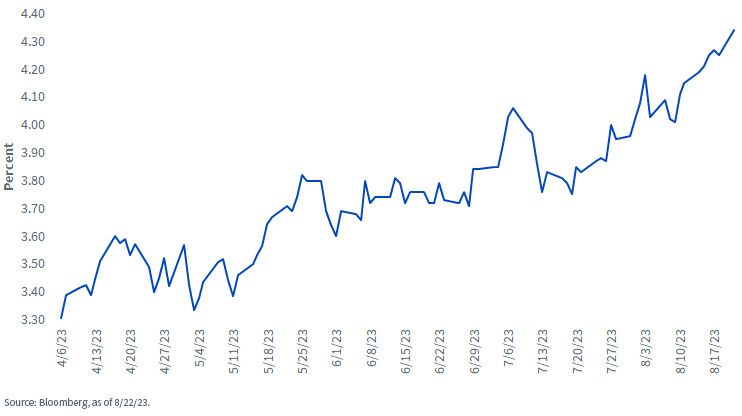

U.S. Treasury 10-Year Yield

Although there’s been somewhat of a seesaw pattern, the rise in the UST 10-Year yield really began back in early April. Since hitting its post-SVB low-water mark of 3.30%, the 10-Year reached as high as 4.34%, as of this writing, marking an incredible 100-basis point move to the upside, and eclipsing the prior high point of 4.24% that was printed back in October.

With the UST 10-Year yield now at its highest level in roughly 16 years, investors are wondering what comes next. In order to answer that question, we need to take a look at the reasons for this most recent move to the upside.

One does need to begin the process with the Fed. Although Powell & Co. are at, or close to, the end of this rate hike cycle, the policy makers continue to leave the door open for rate hikes. More importantly, the money and bond markets have now completely ruled out rate cuts for this year, pushing the timing for the potential first Fed Funds decrease to the end of Q1 next year, at the earliest. After much resistance from the money and bond markets, they have finally embraced the ‘higher for longer’ scenario.

Next up is the resiliency of the U.S. economy, especially the labor markets, where a widely expected recession for 2023 has essentially been removed from the equation, at least for this year. Along the same lines, even though inflation continues to cool overall, core price pressures have remained above the Fed’s 2% threshold. Add to these macro factors increasing supply concerns for Treasuries from trillion-dollar deficits, and voila, the next thing you know, the UST 10-Year yield expereinced a technical breakout to the upside utilizing Fibonacci retracement levels.

So back to the title of this blog post. In order for the UST 10-Year yield to fall on a sustained basis from here, you have to peck away at the aforementioned factors. To begin with, the economy needs to show definitive signs of heading for a downturn (look to labor market data), with some added cooling in inflation. This could potentially push the Fed into a more friendly narrative on just how long rates have to stay in restrictive territory. Unfortunately, the supply issue is not going away any time soon and could get worse as Treasury announced that more increases in coupon auction sizes could be coming in October.

Conclusion

Considering the recent momentum to the upside for the UST 10-Year yield, some consolidation could be expected in the near term. However, the path of least resistance, at this point, seems for the 10-Year yield to remain elevated.

Categories

Related articles

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

Nowhere to Hide…Except Maybe Treasury Floating Rate Notes

How to Mitigate Software Exposure in Bonds

Fed Watch: Between a Rock and a Hard Place

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.