Still Want to Be Late to the Duration Party?

Published August 2, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Throughout the course of the current Federal Reserve rate hike cycle, and the attendant increase in the U.S. Treasury (UST) 10-Year yield, I periodically get asked whether it is time to go long on duration. My answer has been a very consistent one: I’d rather be late than early to the duration party. With the UST 10-Year yield once again passing the 4% threshold, I thought it would be a good idea to revisit this topic. And, alas, my answer still hasn’t changed.

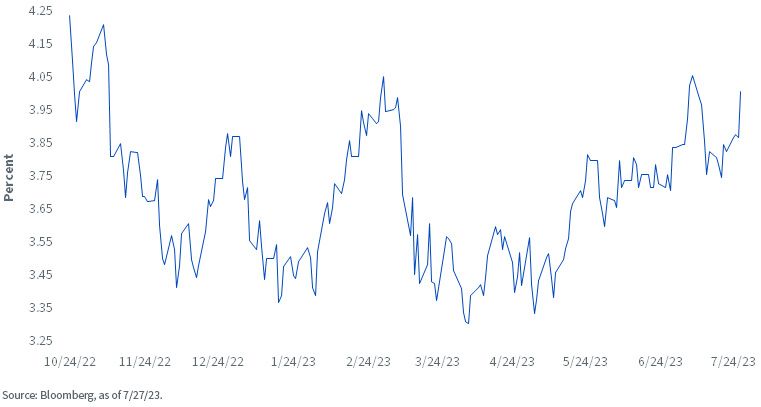

U.S. Treasury 10-Year Yield

In answering the duration question, I think it is useful to show the pattern of the UST 10-Year yield since it hit its most recent peak of roughly 4.25% (4.33% in intra-day trading) in October of last year. Yes, after reaching this high-water mark in the fall, the 10-Year yield did decline in a rather startling fashion, falling by 80 basis points (bps) to a little over 3.40% in December. However, just as quickly, this decline was reversed and another upward move occurred heading into the year-end. In fact, if you look closely at the enclosed graph, it becomes clear how this “up and down, then up again” trend has played out over the last nine months.

The most recent episode occurred beginning in early March. As the reader will recall, Fed Chairman Powell gave rather hawkish testimony to Congress in early March and yields all along the Treasury yield curve rose considerably as a result. In fact, the UST 2-Year yield rose above 5% and the 10-Year yield eclipsed the 4% mark yet again. Then the regional bank turmoil hit, and all bets were off as UST yields plummeted. In fact, the 10-Year ultimately fell to 3.31% in early April, another sizeable decline of 70 bps.

However, let’s fast-forward to the present, where that 70-bps plunge in yield has once again been completely reversed. Indeed, as of this writing, the UST 10-Year yield has retraced all the way back over 4% one more time, posting a 4.01% reading.

Conclusion

With the Fed in “higher for longer” mode, a reasonable outcome for the 10-Year could be to remain in a range-bound pattern, with the yield skewed toward the upper limit. In fact, another run at the aforementioned high point of 4.25% should not be ruled out either. This type of trading pattern would not be conducive to going long on duration in a bond portfolio.

In addition, the historical inversion of the Treasury yield curve offers no incentive, or urgency, to take on such positioning. Against this backdrop, investors should consider Treasury floating rate notes, which provide income without the volatility that has been witnessed in the 10-Year sector. The WisdomTree Floating Rate Treasury Fund (USFR) offers investors a means of tapping into this strategy.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.