Generating Yield in an Evolving Market Environment

Published October 6, 2022

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Scott Welch, CIMA ®

Chief Investment Officer, Model Portfolios

This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

We have been writing a series of blog articles under the umbrella of “generating yield in a volatile market,” most recently in June, and it is time to revisit the topic.

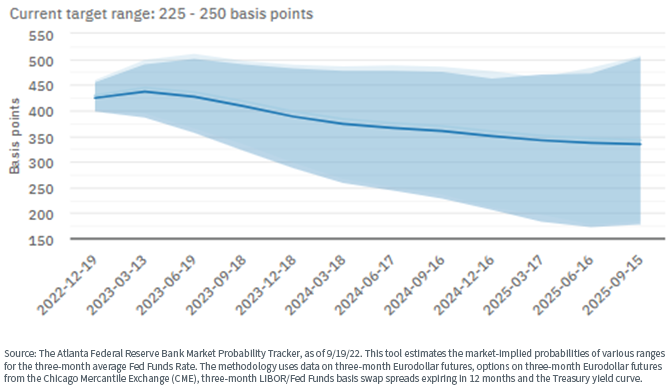

Let’s start by surveying the current market environment. As we write this, the Fed seems determined to maintain its hawkish rate hike policy in an attempt to drive down inflation—raising the Fed Funds Rate by 75 basis points (bps) (0.75%) in June, July and September, with expectations for further rate hikes in its remaining two meetings this year, and potentially into early 2023 as well.

According to the Atlanta Fed, the market certainly seems to expect additional rate hikes going forward, with Fed Funds perhaps reaching 4.00%–4.50% by year-end, though it is also pricing in potential rate cuts as we move through 2023. For some additional perspective, the June 2023 Fed Funds Futures contract is priced for a nearly 4.50% target as of this writing

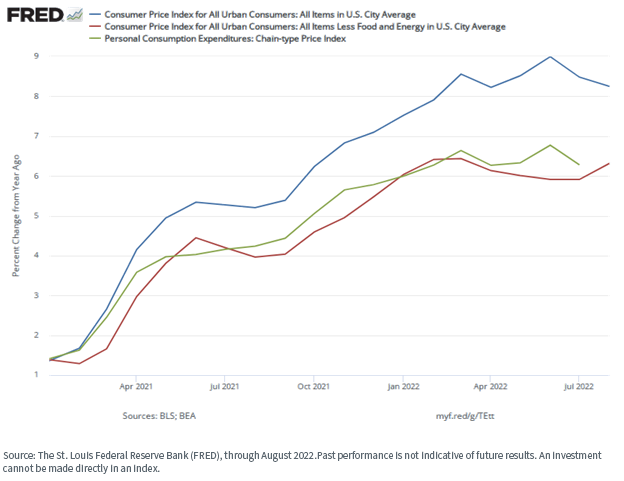

At the same time, while inflation remains high, it seemingly has peaked and may be moving downward.

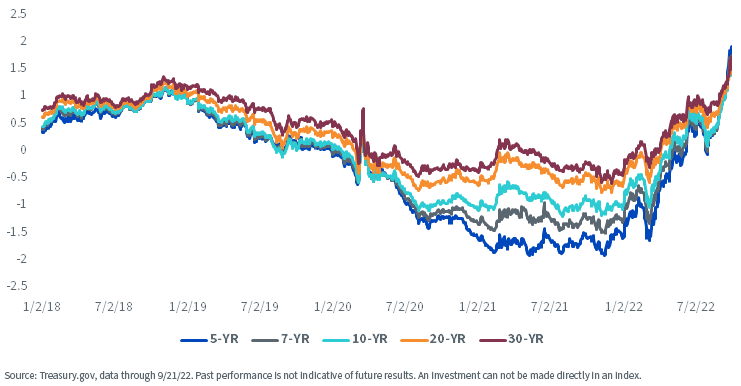

After being negative for more than two years, Treasury real yield rates moved into positive territory across the maturity spectrum sometime in mid-June and seem to be continuing this upward trend.

U.S. Treasury Real Yields (%)

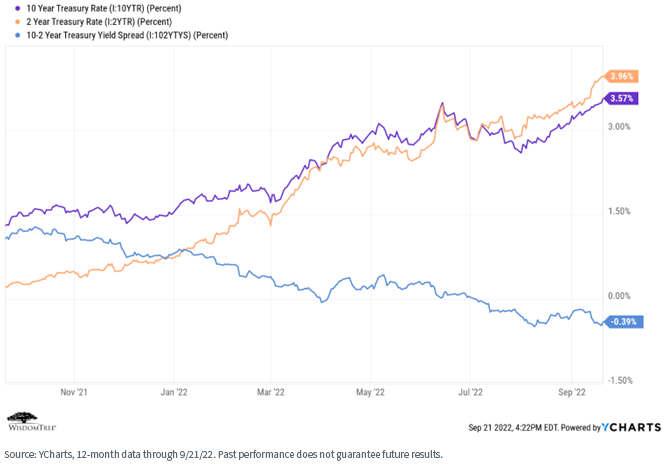

Nominal Treasury rates have also been rising, with the short end rising sharply in the face of the Fed’s tightening program. The yield curve has been inverted (as measured by the 10-Year minus 2-Year yield spread) since early July, resulting in calls of recession by many economists and advisors. Perhaps, but the market is sending “mixed messages” regarding slowing economic activity versus a still-robust labor environment.

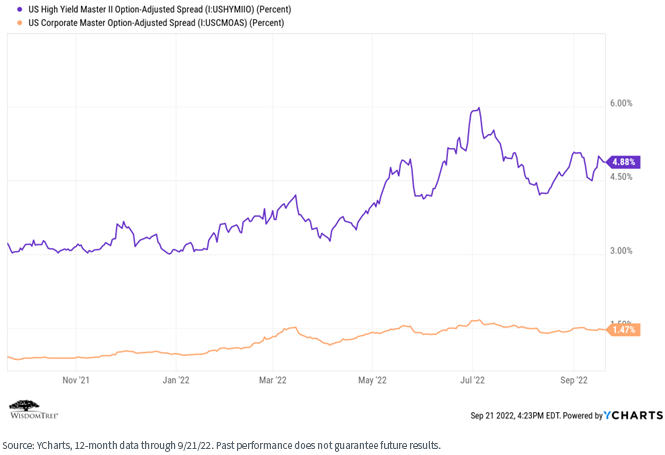

Finally, credit spreads have trended upward over the past 12 months, with heightened volatility especially in high-yield spreads, as the market tries to determine if we are in or heading toward recession or not.

For definitions of terms in the table, please visit the glossary.

What Is a Yield-Seeking Investor to Do?

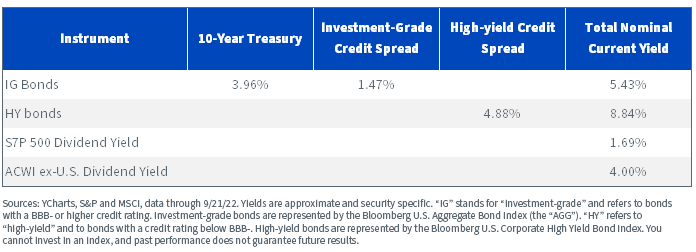

One of the themes in several of our recent blog posts is “there is income back in fixed income.” Let’s compare nominal current yields in the fixed income versus equity markets.

For definitions of terms in the table, please visit the glossary.

It seems, indeed, that there is “income back in fixed income,” although it is also true that, so far this year, bonds have not provided the “hedge” to equity risk they have historically. However, given the generally solid shape of most corporate balance sheets, an “8 handle” on high-yield bonds may deserve some attention.

Product/Strategy Ideas

With flat and/or inverted yield curves, investors are not being compensated for moving out in duration in fixed income. One solution for a “rate-hiking Fed” that also can supplement income is Treasury (UST) floating rate notes, which are reset with the weekly UST 3-Month t-bill auction. This reset enables investors to adjust their yield higher with the Fed as it raises rates, without taking on duration risk. The WisdomTree Floating Rate Treasury Fund (USFR) is a solution that seeks to track the experience within the UST FRN market.

On the credit side of the spectrum, as illustrated above, the U.S. high-yield arena has now arguably moved back into its more traditional role of providing income opportunities within a bond portfolio. However, concerns about where the U.S. economy could be headed can be an important consideration when investing in HY credit. The WisdomTree U.S. High Yield Corporate Bond Fund (WFHY) employs a strategy that screens for quality to potentially mitigate default risk while also tilting toward income.

Model Portfolio Ideas

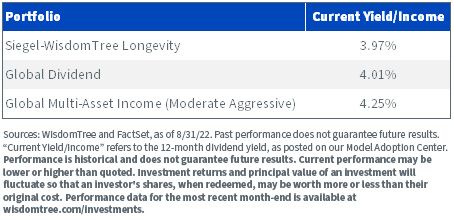

In addition to our product lineup, WisdomTree manages three Model Portfolios we think fit nicely into today’s yield environment, depending on investor objectives: an all-equity Global Dividend model, Multi-Asset Income models of different risk bands and the Siegel-WisdomTree Longevity model, which we manage in collaboration with since-WisdomTree-inception strategic advisor Professor Jeremy Siegel.

All these models focus on generating all or much of the current yield out of the equity allocations versus the fixed income allocations.

Let’s look at the current yield of these portfolios (as of August 31, 2022). “Current Yield/Income” refers to the most recently posted 12-month dividend yield, as indicated here.

For standardized performance and the 30-Day SEC Yield for the underlying fund's please click the respective model: Siegel-WisdomTree Longevity, Global Dividend, Global Multi-Asset Income (Moderate Aggressive). All yield and total return information for these model portfolios and all of the underlying securities within those models can be found in our Model Adoption Center.

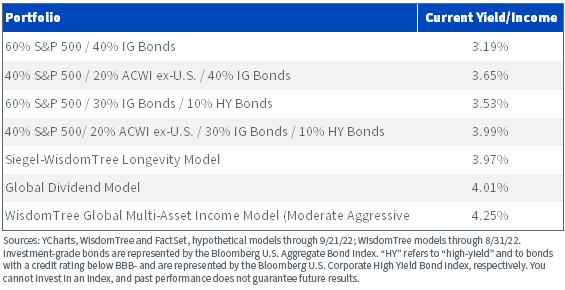

Let’s examine some hypothetical “typical” client portfolios.

Conclusions

For investors seeking yield, we believe there are multiple ways to achieve this investment goal without taking on excessive risk, including incorporating quality-screened high-yield and dividend-focused equities within the portfolio. For investors wishing not to take on duration risk while benefiting from the Fed rate hiking regime, our Floating Rate U.S. Treasury product may fit the bill as well.

You can get all the details on our individual strategies and our Model Portfolios on the WisdomTree website.

Important Risks Related to this Article

For retail investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. The performance of your account may differ from the performance shown for a variety of reasons, including but not limited to: your investment advisor, and not WisdomTree, is responsible for implementing trades in the account; differences in market conditions; client-imposed investment restrictions; the timing of client investments and withdrawals; fees payable; and/or other factors. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from the information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

For financial advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy. In providing WisdomTree Model Portfolio information, WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor or end client, and has no responsibility in connection therewith, and is not providing individualized investment advice to any advisor or end client, including based on or tailored to the circumstance of any advisor or end client. The Model Portfolio information is provided “as is,” without warranty of any kind, express or implied. WisdomTree is not responsible for determining the securities to be purchased, held and/or sold for any advisor or end client accounts, nor is WisdomTree responsible for determining the suitability or appropriateness of a Model Portfolio or any securities included therein for any third party, including end clients.

Advisors are solely responsible for making investment recommendations and/or decisions with respect to an end client and should consider the end client’s individual financial circumstances, investment time frame, risk tolerance level and investment goals in determining the appropriateness of a particular investment or strategy, without input from WisdomTree. WisdomTree does not have investment discretion and does not place trade orders for any end client accounts. Information and other marketing materials provided to you by WisdomTree concerning a Model Portfolio—including allocations, performance and other characteristics—may not be indicative of an end client’s actual experience from investing in one or more of the funds included in a Model Portfolio. Using an asset allocation strategy does not ensure a profit or protect against loss, and diversification does not eliminate the risk of experiencing investment losses. There is no assurance that investing in accordance with a Model Portfolio’s allocations will provide positive performance over any period. Any content or information included in or related to a WisdomTree Model Portfolio, including descriptions, allocations, data, fund details and disclosures, is subject to change and may not be altered by an advisor or other third party in any way.

WisdomTree primarily uses WisdomTree Funds in the Model Portfolios unless there is no WisdomTree Fund that is consistent with the desired asset allocation or Model Portfolio strategy. As a result, WisdomTree Model Portfolios are expected to include a substantial portion of WisdomTree Funds, notwithstanding that there may be a similar fund with a higher rating, lower fees and expenses or substantially better performance. Additionally, WisdomTree and its affiliates will indirectly benefit from investments made based on the Model Portfolios through fees paid by the WisdomTree Funds to WisdomTree and its affiliates for advisory, administrative and other services.

Jeremy Siegel serves as Senior Investment Strategy Advisor to WisdomTree Investments, Inc., and its subsidiary, WisdomTree Asset Management, Inc. (“WTAM” or “WisdomTree”). He serves on the Model Portfolio Investment Committee for the Siegel-WisdomTree Model Portfolios of WisdomTree, which develops and rebalances WisdomTree’s Model Portfolios. In serving as an advisor to WisdomTree in such roles, Mr. Siegel is not attempting to meet the objectives of any person, does not express opinions as to the investment merits of any particular securities and is not undertaking to provide and does not provide any individualized or personalized advice attuned or tailored to the concerns of any person.

The Siegel-WisdomTree Longevity Model Portfolio seeks to address increasing longevity by shifting the focus to potential long-term growth through a higher stock allocation versus more traditional “60/40” portfolios.

USFR: There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new, and the amount of supply will be limited. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WFHY: There are risks associated with investing, including the possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile

Categories

Related articles

A ‘Warsh’ Out at the Fed

Model Portfolios Are Mainstream. Now Advisors Want Personalization.

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

WisdomTree Model Portfolio Positioning Update

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

The Missing Link in a Scalable Models-Based Practice: Free Trading and Rebalancing

About the contributors

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.