Generating Yield in a Volatile Market, Continued

This article is relevant to financial professionals who are considering offering Model Portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

It has been a little more than two months since we last visited the topic of generating yield in a volatile market, but market conditions continue to evolve, so it is time to visit it again. The Fed seemingly remains on its fairly aggressive “rate hike regime” and has now added “quantitative tightening” as it begins to reduce its balance sheet. It will continue to walk a proverbial tightrope as it attempts to balance economic growth against high inflation. Right now, fighting inflation is the primary concern, but the Fed suggests it will be “data dependent” as we move through the summer.

So, with rates and credit spreads volatile and the stock market in a swoon, how best to navigate generating reasonable yield in this environment?

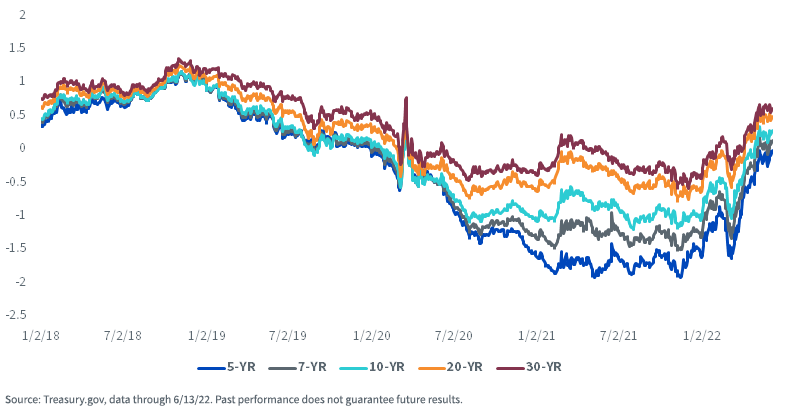

Let’s start with the Treasury yield curve. In the wake of the Fed’s current policy, real Treasury rates have now risen visibly above zero across the entire maturity spectrum. This is meaningful when evaluating fixed income investments—investors are no longer locking in a guaranteed loss of purchasing power if they buy longer-dated Treasuries.

U.S. Treasury Real Yields

Nominal Treasury rates have also been rising, with the short end rising sharply in the face of the Fed’s tightening program. The market got “jittery” in late March when the yield curve inverted for a day or two, and those fears resurfaced over the past week or so as the yield curve flattened again. We think, with fits and starts, this upward rate trend will continue, with the caveat that, should the market perceive the Fed is being too aggressive and is correspondingly shutting down the economy, we may see a new decline. The Fed seemed “locked in” to 50-basis-point (bps) hikes this summer, but the most recent CPI print of 8.6% proved to be the catalyst for a more aggressive stance, pushing fed funds up by a historically high move of 75bp at the June FOMC meeting.

Our “house view” is that (a) inflation may be peaking but likely will be “sticky” for some time to come, and (b) the Fed is somewhat between a rock and a hard place right now but combatting inflation is its primary objective, perhaps even at the expense of economic growth in the second half of the year.

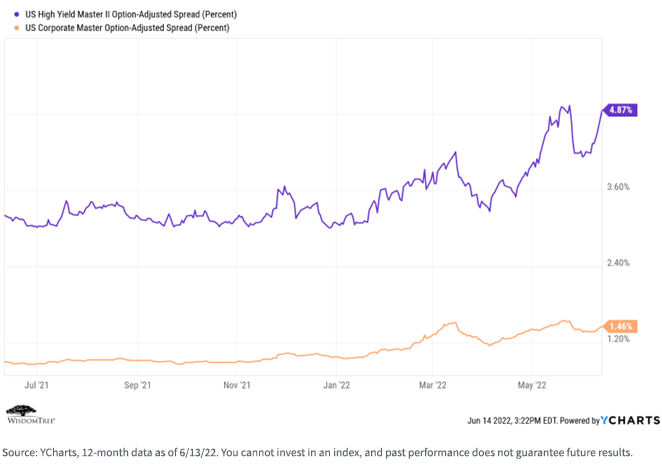

Finally, volatility in credit spreads has increased—a trend we expect to continue as we head into uncertain economic and inflationary times.

For definitions of terms in the table, please visit the glossary.

What Is a Yield-Seeking Investor to Do?

This is not an easy time to find reasonable risk-adjusted yield in the fixed income markets, though pockets of relative opportunity should appear from time to time. At this point, we do not recommend taking on additional duration or credit risk in a “reach” for yield, though our views on duration may evolve as we move through the summer.

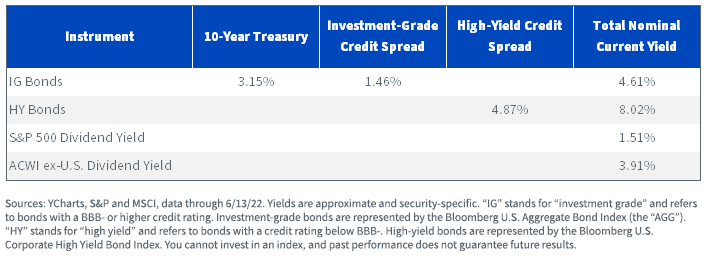

What about finding yield in the equity markets? Using the information from above, let’s compare current nominal fixed income yields to current equity dividend yields.

For definitions of terms in the table, please visit the glossary.

We are starting to see more “normalized” fixed income yields, and available data suggest corporate balance sheets are in good shape. So, while the total return picture may not be overly optimistic, “coupon clippers” may find solace in today’s market environment.

Our own fixed income Model Portfolios remain short duration and over-weight in credit, with a focus on quality security selection, compared to the Bloomberg U.S. Aggregate Bond Index (the “AGG”). We are not looking to take excessive risk in our fixed income portfolios in a “reach for yield.”

Here are some other ideas and solutions that may be of interest.

Product/Strategy Ideas

Within the fixed income universe, the rise in yields thus far in 2022 has altered the backdrop for income-focused investors. Questions surrounding duration remain and will more than likely continue for the second half of this year and into 2023.

Given this uncertainty, investors may want to consider a barbell approach to fixed income investing. Our “in-house” barbell consists of the WisdomTree Yield Enhanced U.S. Aggregate Bond Fund (AGGY) at one end and the WisdomTree Floating Rate Treasury Fund (USFR) as the other “weight.” This barbell offers a core strategic solution designed to help fixed income investors navigate the uncharted waters ahead without making a high-conviction bet on where Treasury yields may ultimately be headed.

Model Portfolio Ideas

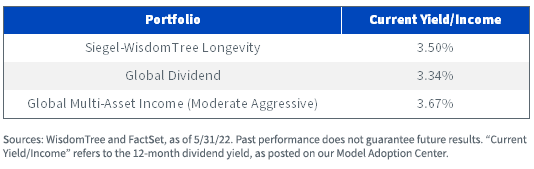

WisdomTree manages three Model Portfolios that we think fit nicely into today’s yield environment, depending on investor objectives:

- The Global Dividend model is an all-equity model designed specifically to generate optimal yield and current income without taking excessive risk. This can be used as a stand-alone model, but many advisors use it as a complementary sleeve to their existing equity portfolios in an attempt to generate additional income.

- The Global Multi-Asset Income model attempts to optimize risk-controlled current yield and income. In addition to equities, it includes fixed income and other yield-generating strategies (e.g., preferred securities and energy master limited partnerships (MLPs)).

- The Siegel-WisdomTree Longevity model, built and managed in collaboration with our since-inception Strategic Advisor, Professor Jeremy Siegel. This model attempts to “build a better mousetrap” to the traditional “60/40” portfolio by over-weighting in yield and dividend-focused equities (75% allocation) while using the fixed income allocation (25%) as a source of risk-controlled income and a hedge to the equity risk of the overall portfolio.

These three models focus on generating all or much of the current yield from the equity allocations versus the fixed income allocations.

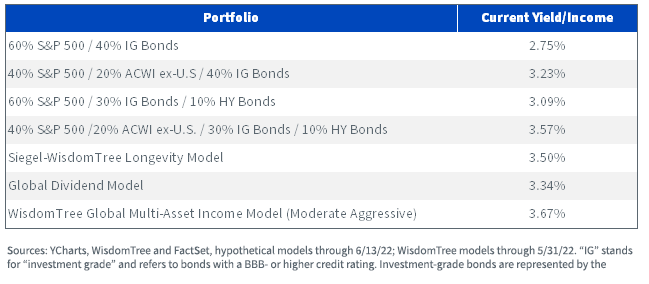

Let’s look at the current yield of these portfolios (as of May 31, 2022). “Current Yield/Income” refers to the most recently posted 12-month dividend yield.

Now let’s examine some hypothetical “typical” client portfolios.

Conclusions

We are approaching a more “normal” market environment, where investors can generate respectable yield out of their fixed income portfolio. While this is a reversal of market conditions in the past two years, it actually represents a more historical environment. There are products and strategies, as discussed above, that have the potential to generate reasonable risk-adjusted yields and performances.

At the same time, we still believe another approach is to focus on the global equity markets to generate yield while still maintaining an adequate fixed income allocation, both for income generation and as a hedge to equity beta risk.

In today’s yield-starved world, we believe you can build intelligent portfolios that generate an acceptable level of risk-adjusted yield without taking excessive risk.

You can get all the details on our individual strategies and our Model Portfolios on the WisdomTree website.

Important Risks Related to this Article

For retail investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. The performance of your account may differ from the performance shown for a variety of reasons, including but not limited to: your investment advisor, and not WisdomTree, is responsible for implementing trades in the account; differences in market conditions; client-imposed investment restrictions; the timing of client investments and withdrawals; fees payable; and/or other factors. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from the information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

For financial advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy. In providing WisdomTree Model Portfolio information, WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor or end client, and has no responsibility in connection therewith, and is not providing individualized investment advice to any advisor or end client, including based on or tailored to the circumstance of any advisor or end client. The Model Portfolio information is provided “as is,” without warranty of any kind, express or implied. WisdomTree is not responsible for determining the securities to be purchased, held and/or sold for any advisor or end client accounts, nor is WisdomTree responsible for determining the suitability or appropriateness of a Model Portfolio or any securities included therein for any third party, including end clients.

Advisors are solely responsible for making investment recommendations and/or decisions with respect to an end client and should consider the end client’s individual financial circumstances, investment time frame, risk tolerance level and investment goals in determining the appropriateness of a particular investment or strategy, without input from WisdomTree. WisdomTree does not have investment discretion and does not place trade orders for any end client accounts. Information and other marketing materials provided to you by WisdomTree concerning a Model Portfolio—including allocations, performance and other characteristics—may not be indicative of an end client’s actual experience from investing in one or more of the funds included in a Model Portfolio. Using an asset allocation strategy does not ensure a profit or protect against loss, and diversification does not eliminate the risk of experiencing investment losses. There is no assurance that investing in accordance with a Model Portfolio’s allocations will provide positive performance over any period. Any content or information included in or related to a WisdomTree Model Portfolio, including descriptions, allocations, data, fund details and disclosures, is subject to change and may not be altered by an advisor or other third party in any way.

WisdomTree primarily uses WisdomTree Funds in the Model Portfolios unless there is no WisdomTree Fund that is consistent with the desired asset allocation or Model Portfolio strategy. As a result, WisdomTree Model Portfolios are expected to include a substantial portion of WisdomTree Funds, notwithstanding that there may be a similar fund with a higher rating, lower fees and expenses or substantially better performance. Additionally, WisdomTree and its affiliates will indirectly benefit from investments made based on the Model Portfolios through fees paid by the WisdomTree Funds to WisdomTree and its affiliates for advisory, administrative and other services.

Jeremy Siegel serves as Senior Investment Strategy Advisor to WisdomTree Investments, Inc., and its subsidiary, WisdomTree Asset Management, Inc. (“WTAM” or “WisdomTree”). He serves on the Model Portfolio Investment Committee for the Siegel-WisdomTree Model Portfolios of WisdomTree, which develops and rebalances WisdomTree’s Model Portfolios. In serving as an advisor to WisdomTree in such roles, Mr. Siegel is not attempting to meet the objectives of any person, does not express opinions as to the investment merits of any particular securities and is not undertaking to provide and does not provide any individualized or personalized advice attuned or tailored to the concerns of any person.

The Siegel-WisdomTree Longevity Model Portfolio seeks to address increasing longevity by shifting the focus to potential long-term growth through a higher stock allocation versus more traditional “60/40” portfolios.

AGGY: There are risks associated with investing, including the possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated or defaulted on. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

USFR: There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new, and the amount of supply will be limited. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links