The Russia-Ukraine Conflict & the Potential Impact on Gold

Published March 4, 2022

At the time of writing, many commodity prices are rallying on the news. Oil, natural gas, wheat, corn, palladium, aluminum and nickel are all trading higher, including gold. While other commodities have rallied in the past year, gold has been sitting in the shadows. Gold is often thought of as a geopolitical hedge instrument.

Geopolitical risk is an inherently difficult thing to quantify. Quantifying the relationship between an asset price and geopolitical risks is even more difficult. Looking back at periods when there has been a perception of elevated geopolitical events, it is hard to say that asset prices have behaved in a consistent manner. Any positive or negative price movement needs to be viewed in the context of broader economic activity at the time.

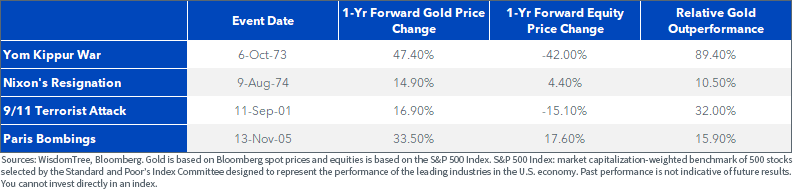

Nevertheless, we can point to some geopolitical case studies that have shown a very strong positive reaction from gold. The table below gives four examples where gold has significantly outperformed equities in the aftermath of a geopolitical shock.

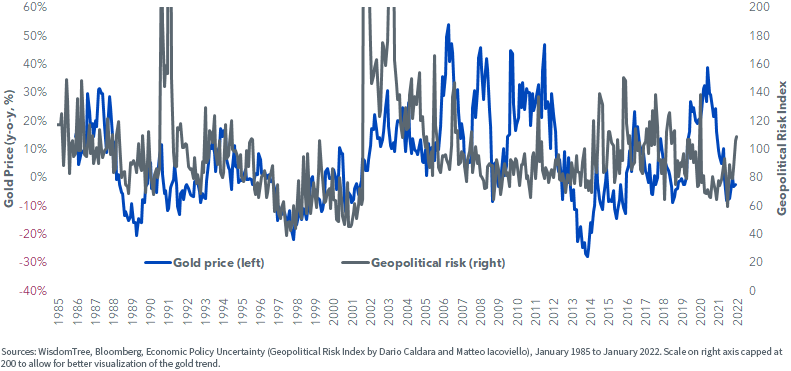

Notwithstanding the difficulty in quantifying geopolitical risk, we use the Geopolitical Risk Index developed by the Federal Reserve Board’s Dario Caldara and Matteo Iacoviello, which is based on automated text-search results of the electronic archives of 10 newspapers. Plotting their series against gold yields some interesting results.

- Immediately before the buildup to the Gulf War (1990), gold prices were quite depressed. It seems the buildup ignited gold prices.

- Immediately before the 9/11 terrorist attacks in the U.S. (2001), gold was depressed. The attacks seem to have ignited gold prices. The Iraqi war soon after (2002) kept gold well supported.

Gold and Geopolitical Risks

We believe most people would agree that gold price behavior in 2021 was disappointing, with the backdrop an elevated level of inflation. Our models indicate that gold should have been trading close to $2,500/oz in January 2022 when inflation in the U.S. was running at 7.5%.1

Could the beginning of a war in Ukraine act as a catalyst for gold in a similar way to the noted events in 1990 and 2001?

1 Other relevant inputs to our model for this January gold price calculation include: dollar basket (DXY) at 96.5, U.S. 10-Year Treasury yields at 1.78%, net speculative positioning on gold futures contracts at 245,782 (source: Bloomberg, 31/01/22)

Important Risks Related to this Article

Nitesh Shah is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree Investments, Inc.

Categories

Related articles

The Strategic Metals Underpinning Our Modern Technologies

Gold Monthly: Rebounding after a Violent Drawdown

Adding, Not Replacing: Gold in the Age of Efficient Capital

Adding, Not Replacing: Broad Commodities in the Age of Efficient Capital

Rebalancing for a Fragmenting World: Why Broad Commodities Still Matter

Shockwaves: How an Energy Crisis Spreads Across Commodities

Inflation Fears Are Rising Again. WTIP Was Ready.

Hard Assets in a Soft World

Gold and Silvers’ Most Volatile Day

About the contributor

Nitesh Shah

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.