HEDJ

Europe Hedged Equity Fund

Published May 2, 2024

Global Head of Research

U.S. market leadership has been well established for much of the last 15 years, but it might surprise a number of readers to learn some European ETFs outperformed the U.S. over the last three years—so long as those ETFs employed a currency-hedged approach.

The dollar has been strong, and we think it offers a nice diversifier to portfolios. But if there is a place where it matters the most, it likely is Europe, which we see as having long-term structural issues with its economy.

But low growth can lead to opportunities for low valuations in companies that participate in revenue growth around the world, not just in Europe.

U.S. equity markets are richly priced. While valuation by itself has rarely caused a market correction, there are wide concerns that U.S. equities could be ripe for a downturn.

European equities are perceived to be among the global laggards in performance. From the top down:

Many tend to assume that the U.S. must be crushing Europe on an equity market performance basis.

To give a better sense of how different types of equities are performing, we can delve into the broad ETF toolkit including3:

In recent years, investors have become so used to U.S. equities outperforming European equities that the question of which region is winning in a given period has almost faded away. Few, if any, assume that European equities would be outperforming those in the U.S.

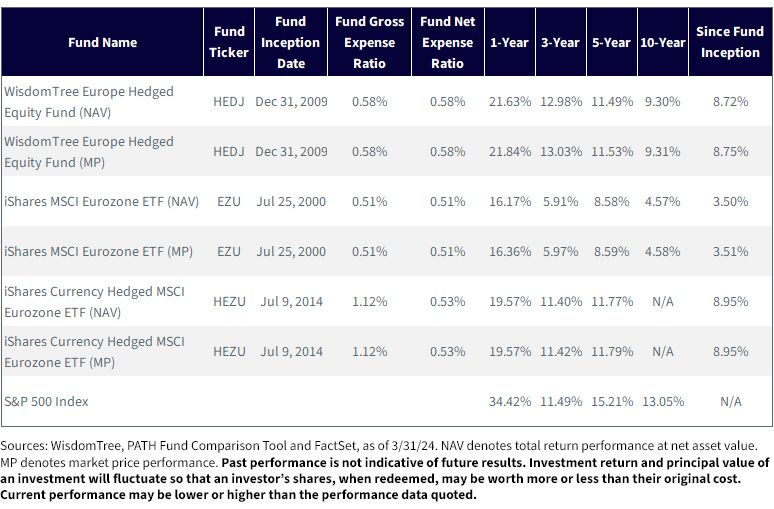

Performance data for the most recent month-end for HEDJ is available here.

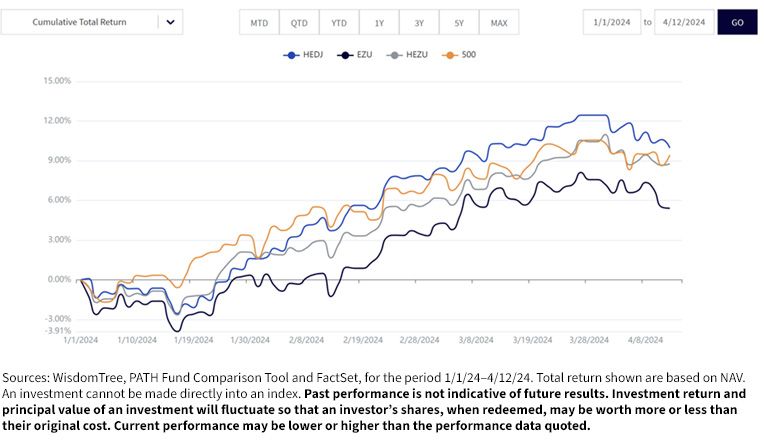

In Figure 1b, we see:

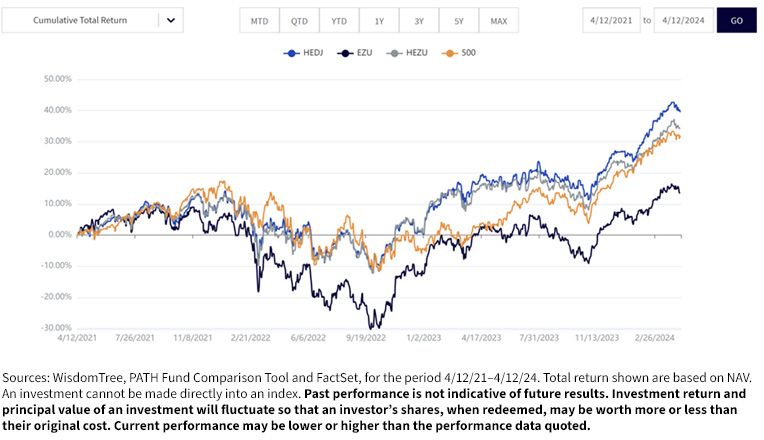

If we think of the past three years (figure 2), we can see a mix of big equity market events in our mind’s eye:

In this environment of growth over value and with Europe having a reputation for being so anti-growth, we can see a case for why we might expect U.S. stocks to beat European stocks over the past three years…and yet, HEDJ outperformed.

The evolution of the U.S. equity market has led to big platform companies attaining primacy. The Magnificent 7 in 2023—Apple, Alphabet, Meta Platforms, Amazon.com, Microsoft, Tesla and Nvidia—share a common thread of a massive base of users that subscribe to certain services.

Looking to Europe, one big group of companies is the auto makers. These firms are very capable and longstanding, but at the core are viewed as car companies, whereas Tesla is able at times to be perceived as more of an AI or software company.

Another big company is ASML. Nvidia’s most advanced chips are being fabricated by Taiwan Semiconductor Manufacturing Co. (TSMC) on machines developed and maintained by ASML.

Then, there is the luxury market, represented by LVMH, which has some of the best brand recognition in the world, but is still making physical products.

The bottom line: there are great companies in Europe but not the same number of clear cases of firms that can break a trillion or trillions of U.S.-dollar market capitalization in the near term. Notably, many of the Magnificent 7 firms do in fact garner significant revenues from Europe.

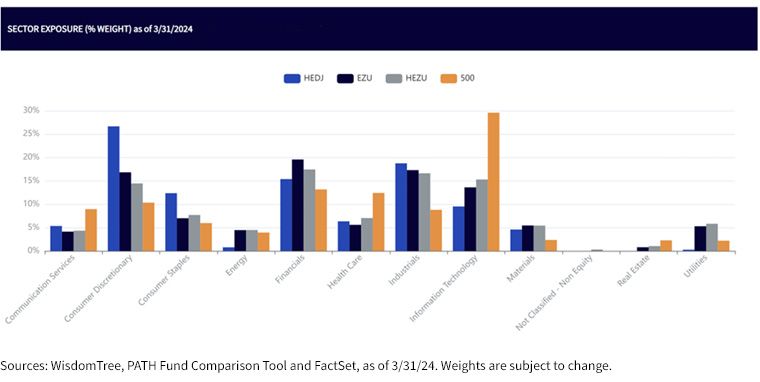

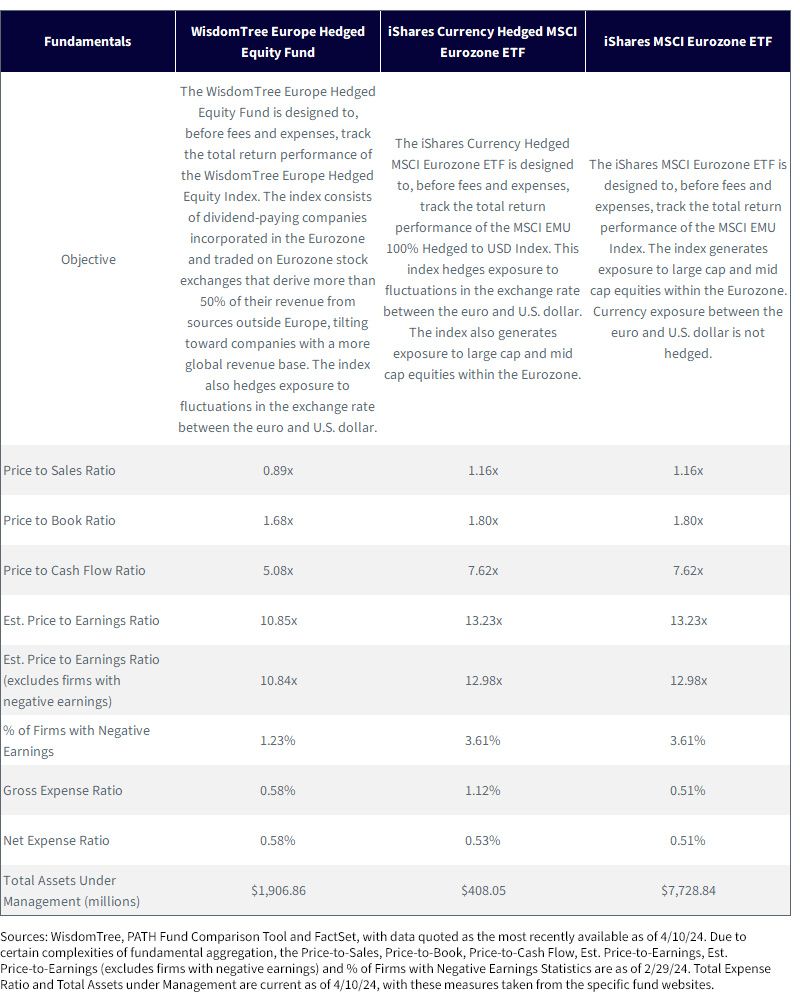

In figure 3, we see that the S&P 500 Index has roughly 30% exposure to what we think of as ‘tech’ and HEDJ places much more weight into Consumer Discretionary. A big reason an export-oriented strategy has so much discretionary exposure is in fact the auto makers.

We frequently come back to valuations here in 2024.

The U.S. equity market has been driven forward by large-cap growth and it is at the more expensive end of its range. While an expensive valuation is rarely the reason why an equity market will drop, it does create a greater susceptibility to risk if earnings ever disappoint.

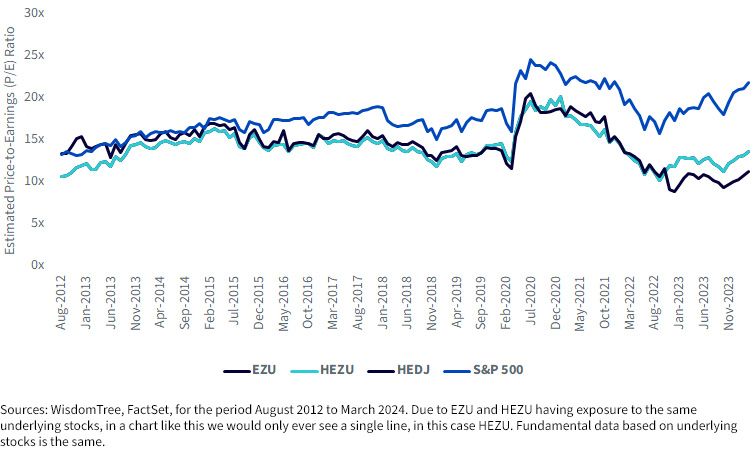

When we look at the performance of European exporters, there are periods when they have outperformed the U.S. and they have certainly not lagged as much as many might think. With that said, on a forward price-to-earnings ratio (P/E) basis, the S&P 500 Index is above 20x, whereas HEDJ is at approximately a 50% discount and closer to 10x.

We’d note that in figure 4, since HEZU and EZU have the same underlying stock exposures, the forward P/E ratio data is the same for each of the relevant historical time series.

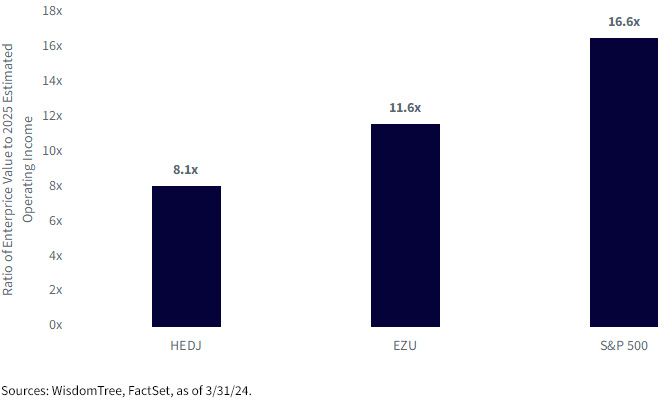

We think a lot about the nexus between how an equity market is currently priced relative to its future growth expectations. We also try to get beyond the current year and think a bit ahead. Figure 5 takes a measure of 2025 operating income and compares that to the current enterprise value of the different ETFs. Since EZU and HEZU contain the same underlying stocks, we only show one of them here.

Our conclusion: HEDJ, EZU, HEZU and the S&P 500 Index have very different risk profiles. If one wants exposure to U.S. large-cap growth—there is not substitute for a U.S. exposure. However, many investors we speak to look at the U.S. market and have seen very good performance of late.

They are concerned about valuation. Figure 5 shows that HEDJ is currently trading at about half the ratio of the S&P 500 Index if one is comparing EV/2025 operating income.4

In our opinion, this discount could allow investors to feel more comfortable with the increased risk of investing outside the U.S.

If you are a financial professional and interested in diving further into the comparison of these Funds, please check out our Fund Comparison Tool.

1 Source: AI Act, European Commission, https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai

2 Source: Nestor Maslej, Loredana Fattorini, Erik Brynjolfsson, John Etchemendy, Katrina Ligett, Terah Lyons, James Manyika, Helen Ngo, Juan Carlos Niebles, Vanessa Parli, Yoav Shoham, Russell Wald, Jack Clark, and Raymond Perrault, “The AI Index 2023 Annual Report,” AI Index Steering Committee, Institute for Human-Centered AI, Stanford University, April 2023.

3 EZU is the largest ETF within the U.S. ETF Europe Stock category for Morningstar, measured on the basis of assets under management (AUM), that has only eurozone equity exposure, i.e., no exposure to the UK, Switzerland, Norway, Sweden or any other country that does not use the euro currency. Calculations were run as of 4/22/24. HEZU is the currency-hedged version of the same strategy.

4 Refers to a measure of current enterprise value over 2025 operating income, meaning that company estimates of 2025 operating income are aggregated for each strategy. The source is FactSet, which aggregates all analyst estimates.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Europe Hedged Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.