DXJ

Japan Hedged Equity Fund

Published May 2, 2024

Global Head of Research

Who was predicting that, during the first quarter of 2024, we would see record highs in:

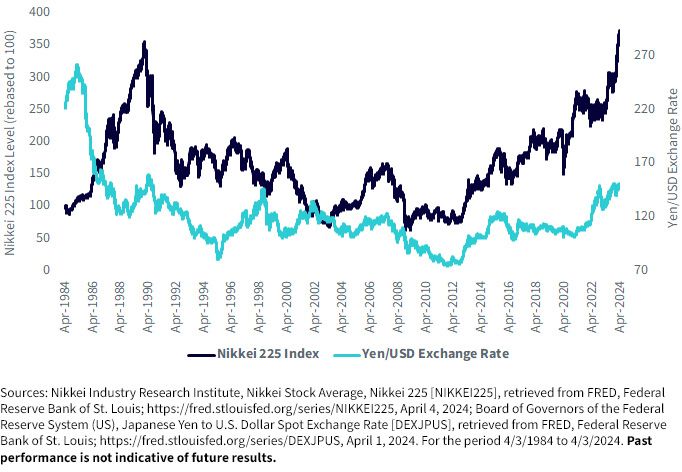

Out of those, I have to admit I was most excited about Japan’s equity market, as this new record high took from 1989 (roughly 35 years) to surpass. At WisdomTree, we were heavily focused on Japan when Prime Minister Shinzo Abe was first elected in 20124, but it was not viewed as remotely reasonable to even consider that a surge in the equity market could take us back to 1989 levels at that point.

Figure 1 looks at the last 40 years:

Bottom line: To us, it is not an accident that Japan’s equity market is breaking out to new highs after a period of significant yen weakness against the U.S. dollar.

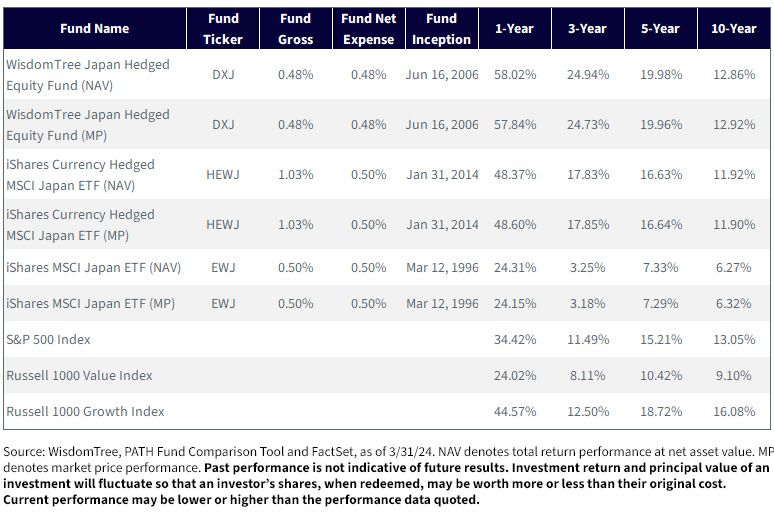

A beautiful thing about the proliferation of ETFs is that we can use more and more strategies to illustrate different stories playing out across asset classes in markets. Here, we can look at some of the most widely followed strategies that provide exposure to Japanese equities:5

We can then use indexes to benchmark the performance back to the U.S. equity experience. We do this because our readers are based in the U.S. and tend to think of Japanese equities at least in part for how they compare to the attributes, including performance, of U.S. equities.

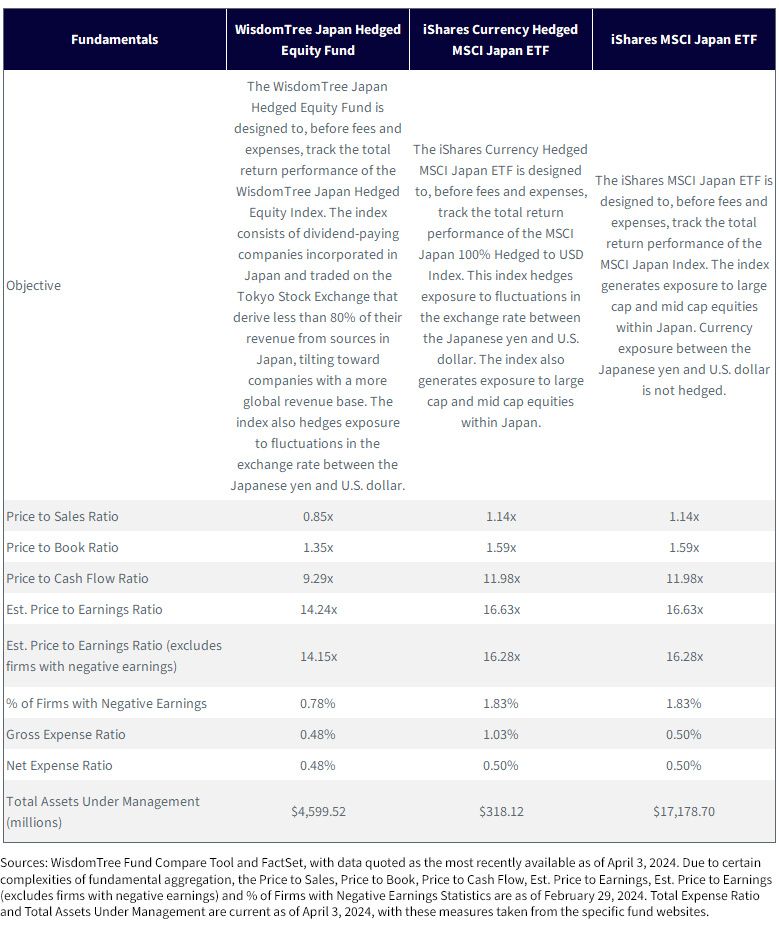

For each Fund’s full standardized and most recent month-end performance, please click the respective ticker: DXJ, HEWJ, EWJ.

For definitions of terms in the table above, please visit the glossary.

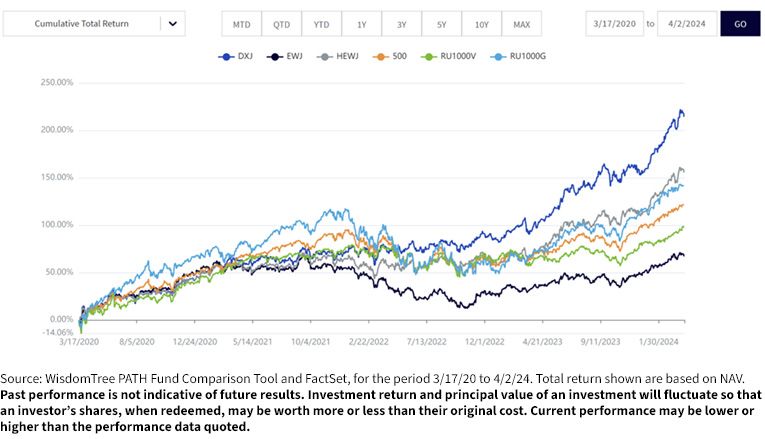

Over the period of 10 years visible in figure 2b, its clear that:

For each Fund’s full standardized and most recent month-end performance, please click the respective ticker: DXJ, HEWJ, EWJ.

For each Fund’s full standardized and most recent month-end performance, please click the respective ticker: DXJ, HEWJ, EWJ.

We hear a lot of investors concerned about U.S. equity valuations. Companies like Nvidia have delivered incredible recent returns. Many are looking for something else to lead markets from here beyond just the largest, predominantly tech-oriented firms.

One answer—investors can stay in the U.S. and try to look towards value and away from growth. That worked in 2022, and it worked during March 2024—but history has shown that being in the U.S. and not looking to large growth, at least in recent years, has lagged more than it has outperformed.

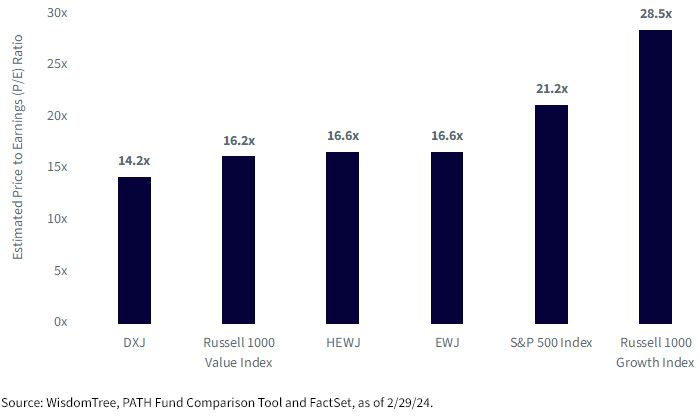

Another answer—and a possible surprise—is that even though Japan has rallied and the Nikkei 225 Index has achieved a recent record, the estimated P/E ratio (shown in figure 4) is about 14 points lower than that of the Russell 1000 Growth Index. We don’t know with certainty whether or not Japan’s rally continues, but we would simply note that if the focus is on Japan’s equities, hedging—taking away the risk of movements in the yen/U.S. dollar exchange rate—is the way to make the investment solely about equities. DXJ is tracking the returns of an underlying index focused on exposure to companies with global earnings—companies with earnings outside of Japan do, in fact, get a boost if the yen is weakening versus other global currencies, like the U.S. dollar.

For definitions of terms in the table above, please visit the glossary.

If you are a financial professional and interested in diving more into the comparison of these Funds, please check out our Fund Comparison Tool.

1 Source: Coinbase, Coinbase Bitcoin [CBBTCUSD], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CBBTCUSD, 4/4/24.

2 Source: https://goldprice.org/gold-price-history.html

3 Source: Nikkei Industry Research Institute, Nikkei Stock Average, Nikkei 225 [NIKKEI225], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/NIKKEI225, 4/4/24.

4 Source: Mireya Solis, “Shinzo Abe’s Surprising Victory,” Brookings, 9/28/12.

5 EWJ is the largest, most longstanding ETF option for U.S. investors focused on passive exposure to Japanese equities. HEWJ represents the currency-hedged version of this strategy. As of April 22, 2024, within the US ETF Japan Stock category, EWJ was the largest ETF on the basis of assets under management (AUM). HEWJ represents the currency-hedged version of the same strategy.

6 Source: Russell 1000 Growth Index factsheet, as of 3/31/24.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DXJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, derivative investments which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

Japan Hedged Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.