The New Rate Regime: Income without the Volatility

Published January 17, 2024

Kevin Flanagan

Head of Investment and Fixed Income Strategy

The money and bond markets appear to be doubling down on their optimistic expectations for Fed rate cuts this year despite the release of key economic data (jobs and CPI reports) that would normally be viewed as somewhat challenging to this narrative. That brings us back to a theme I’ve discussed quite a bit over the last few months: fixed income investors will more than likely continue to face elevated volatility, especially in the U.S. Treasury (UST) arena, without the income typically associated with it.

During the first half of January, UST yields, such as for the 2- and 10-Year notes, have witnessed increases of roughly 15–20 basis points (bps), only to come crashing back down again. In fact, in the case of the UST 2-Year note, its yield on Friday dropped to its lowest reading since May of last year.

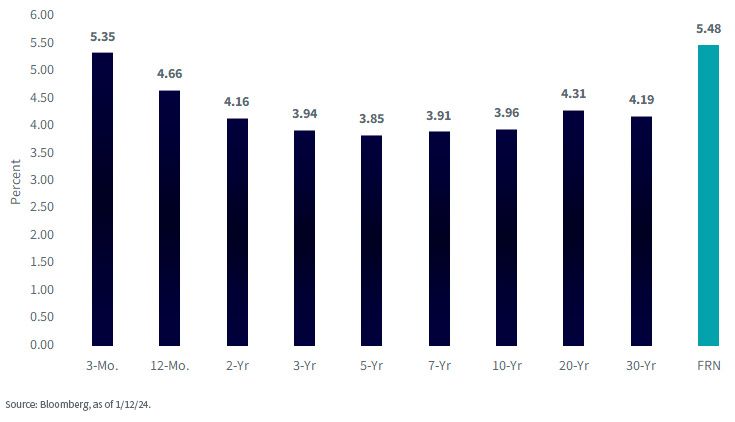

U.S. Treasury Yields

Since I last blogged about this topic about two months ago, there has been a noteworthy development I wanted to bring readers up to date with: UST yields have fallen even further. To provide some perspective, in mid to late November, the UST 2-Year yield was just under 4.90%, or more than 70 bps above its current level, as of this writing. The widely followed UST 5- and 10-Year yields have declined roughly 50–60 bps during this same timeframe. In fact, the entire 3–10-Year sector of the Treasury yield curve last week was at yield levels below the 4% threshold. As recently as late October, these maturities were trading right around the 5% vicinity.

The main catalyst for these downward movements is continued optimism the Fed will cut rates aggressively this year. Implied probabilities for Fed Funds Futures are pricing in six to seven rate cuts for 2024, worth a total of at least 160 bps. This scenario would put the Fed Funds target range between 3.50% and 3.75%. Arguably, one can make the case that the UST market has already priced in a lot of good news, and as we’ve seen many times in the past (2023 included), the track record for the implied probability measure is not very good. In other words, there is definitely room for disappointment on this front.

So, what is one way investors can position themselves in this rate setting?

Playing Defense (Income without the Volatility): WisdomTree Floating Rate Treasury Fund (USFR)

- USFR is tied to the UST 3-month t-bill auction yield, which is directly tied to the actual Fed Funds Rate, not an expectation, such as what is being discounted by the fixed coupon sector.

- Why is that important? Because the Fed hasn’t cut rates. The 3-month t-bill yield is essentially unchanged vs. the declines in the 2-, 5- and 10-Year yields I mentioned earlier.

- We believe Fed rate cuts are coming, but what if the market is wrong in its aggressive pricing on this front? Volatility.

- And don’t forget the yield curve is still inverted, hence UST floating rate notes (FRNs) are the highest-yield Treasury security by a wide margin in many cases (see above).

- Even if the Fed cuts rates by 100 bps in 2024, UST FRN yields would more than likely still be well above the current fixed coupon Treasury yields.

Conclusion

This is the first in a series of blog posts on The New Rate Regime…so stay tuned!

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.