U.S. Fixed Income: Looking Back and Looking Ahead

Published January 3, 2024

Kevin Flanagan

Head of Investment and Fixed Income Strategy

In what can be described as a big understatement, calendar year 2023 proved to be an incredible roller-coaster for U.S. fixed income. From interest rates to spread movements, volatility continued to be underscored in a rather noteworthy fashion. However, with all of this back and forth, an interesting result occurred…the major fixed income asset classes all wound up registering positive returns.

So, let’s first take a look at 2023 and then turn our attention to what investors could consider in the bond market during the new year.

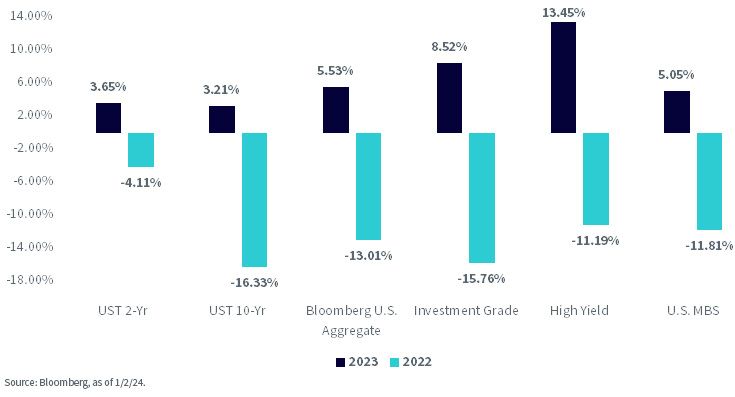

Fixed Income Total Returns

2023

The bar chart neatly displays how last year’s performances stood in stark contrast to 2022, arguably one of the worst years for fixed income on record. As you can see, positive returns were enjoyed by all the major asset classes from rate sensitive, Treasuries (UST) and mortgage-backed securities (MBS), to credit sensitive, investment grade (IG) and high-yield corporates (HY), and including the benchmark Bloomberg U.S. Aggregate Bond Index, the Agg.

Going back to the point I was making in the intro, it wasn’t all roses for U.S. fixed income last year, just the opposite in fact. As recently as late October, it was sure looking like 2023 was going to be another year of negative performance for bonds, which would have made it three in a row for the broader fixed income arena, the Agg.

But once the calendar turned to November, everything changed. Sentiment in the money and bond markets shifted dramatically and yield levels plummeted across the board, while MBS and corporate bond spreads narrowed considerably. Here are some notable stats for: Year-End 2022, Oct/Nov Highs,Year-End 2023:

- UST 2-Year yield: 4.43%; 5.22%; 4.25%

- UST 10-Year yield: 3.87%; 4.99%; 3.88%

- US MBS spread: +51 bps; +82 bps; +47 bps

- US IG Corp: +130 bps; +130 bps; +99 bps

- US HY Spread: +469 bps; +438 bps; +323 bps

Did you happen to notice that the UST 2-Year and 10-Year yields and MBS spreads ended up being little changed from year-end 2022? Meanwhile IG and HY corporate spreads narrowed considerably just over the last two months.

2024

What does the new year have in store for the fixed income investors? Our primary theme for 2024 is to focus on the new rate regime, and now there appears to be a new twist. I’ve discussed often how bond yields have risen to levels a generation of investors haven’t seen before. However, 2024 also looks like it could be the year for the Fed to begin cutting rates, not hiking them.

Here are some key themes for 2024:

- While it appears rate cuts are coming, a notable deterioration in economic data and continued disinflation may be required to validate UST market expectations for significant policy easing in 2024

- Short duration fixed income is our preference to “play the rate cut trade”

- We continue to add duration in a deliberate manner, moving closer to neutral stances relative to benchmarks

- However, given the inverted nature of the yield curve and our expectation for ongoing interest rate volatility, we remain allocated to Treasury floating rate notes

- We remain constructive on quality-screened credit and have selectively rotated into MBS

Conclusion

As we’ve seen the last couple of years, market sentiment can shift rather quickly, and arguably at times, unexpectedly. So, stay tuned!

Categories

Related articles

Closing the Curtain on Rate Cuts

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.