Is AI Excitement Creating a Stock Market Bubble?

Published June 29, 2023

Christopher Gannatti, CFA

Global Head of Research

History shapes our views, and we are always seeking analogues to current events. Even if we know past performance is not indicative of future performance we are still comforted when we draw parallels to the past. Many are now drawing parallels between the current tech enthusiasm and the dawn of the internet.

We also recently spoke with Professor Jeremy Siegel, who has written extensively on the historical performance of equities. He pointed out that what we are seeing in 2023 is not similar to what we saw in 2000 when the tech bubble burst, especially in terms of fundamentals and valuation. We wanted to explore this idea further with this piece.

The quintessential bubble developed in the late 1990s. Some hallmarks of that time:

- When companies put the suffix “.com” in their name, their share prices soared. Any company could do so, regardless of real business prospects or potential.

- In the absence of profits or even sales, new metrics were created to make the case for progress in business, like webpage visits or clicks.

- Many leading internet companies did not have positive earnings, but even in the more established S&P 500, which requires profitability for inclusion, price levels approached 100x earnings for many large-cap names. Hundreds of billions of dollars of market capitalization was supported by dreams of wild future profits.

And what has been happening in the first half of 2023:

- There are some companies putting “AI” in their names, but it is not yet a huge number and they have real business reasons for doing so. Additionally, at least so far, not many private companies have tapped the public markets.

- Naturally, investors will look to track measures like the intensity with which firms are using AI or engaging with data. Because people remember the tech bubble period, we doubt that people will again say that ‘earnings don’t matter’ or ‘revenues don’t matter’—or at least that could still be some time away.

- When we look at how the big indexes, like the Nasdaq 100 Index and the S&P 500 Index, are being driven higher by the largest companies, we see that all those large companies are ‘real businesses.’ They have revenues, cash flows and earnings. It’s absolutely true that investors might look at Nvidia, as an example, and think its multiple is too high for the growth they expect to see—but it’s not a case of Nvidia selling the dream of making a chip one day. Nvidia chips exist, they are sold, and Nvidia is the clear leader in providing the graphics processing units (GPUs) that allow AI to run.

Our conclusion—even if the market could very well be ripe for a near-term correction after a nearly six-month run, and even if that run has been accompanied by a hype cycle in AI, we are not seeing signals that broad technology focused stocks are in bubble territory.

Let’s Look at Some Numbers…

During the tech bubble investors decided to not look at the classic statistics. We will not make that mistake here. Looking at figure 1:

- We create a view of an ‘Expanded Tech’ sector. Companies like Meta Platforms and Alphabet are in the Communication Services sector. Amazon.com (even accounting for that .com suffix) is in Consumer Discretionary. Information Technology includes Microsoft and Apple. If we use this Expanded Tech designation, we capture a broader cross section of technology.

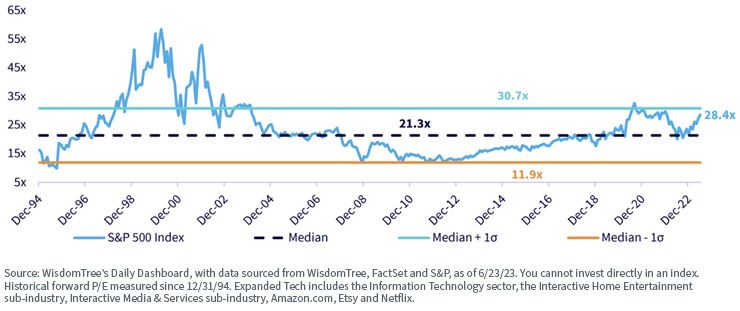

- In 1998–2000, roughly speaking, the S&P 500 was hitting a forward P/E ratio of more than 55x. The initial run up was based on prices and euphoria—the second spike into the 50x range would have been from the quick drop in forward earnings expectations when the popping of the bubble was clear.

- If we then ask—what is this same index trading at in terms of forward P/E at present—it is still below 30x. As 28.4x is not ‘cheap,’ we are not seeking to indicate tech is currently cheap in any way.

- Back in 2000, real interest rates were higher. However, we note that this multiple expansion has occurred alongside a higher interest rate environment—not always an easy feat for stocks to achieve. In 2000 when the tech sector was over 55x forward earnings, real interest rates (measured by TIPS bonds) were double where they are currently.

Figure 1: S&P 500 Expanded Tech Forward P/E Ratio over Time

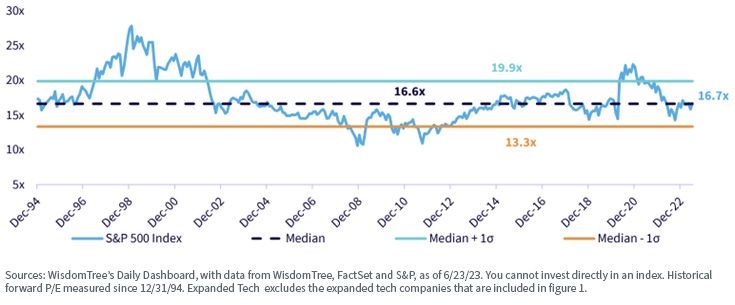

Then, in figure 2:

- We can see how the ‘other stocks’ that are not tech have been doing by way of valuation. These other stocks never broke a 30x forward P/E ratio during the tech bubble.

- The current valuation of the expanded tech part of S&P 500 is at 16.7x and is very close to the average over the full period. This is not cheap, but nor is it getting into the more expensive territory.

Figure 2: S&P 500 Expanded Tech Forward P/E Ratio over Time

Our bottom line: A bubble is not just ‘a bit expensive’ or ‘kinda expensive,’ but rather represents a situation where prices have clearly gone far beyond fundamentals. Forcing ourselves back to a classic figure, forward P/E ratio, we don’t see evidence of that being the case.

Dealing with the AI Hype Cycle

Still, we recognize that performance in thematic equities can come in waves. One way to deal with these waves is to allocate to certain themes and then recognize that over a cycle—something closer to 10 years than 5—there are going to be periods of strongly positive and strongly negative returns.

In many cases, knowing whether the themes are working or not is something completely different from looking at the share price performance. What we know today is that, in the current quarter, Nvidia is expecting revenues in the range of $11 billion. It will be critical to watch that trajectory, which then indicates a 12-month run rate above $40 billion. Do we actually see that materialize? Similarly, companies like Microsoft and Alphabet will continue to talk about the topic and launch new options for their customers. These are the kinds of things that we can honestly see and monitor.

Signals of a greater degree of froth could entail seeing a much more robust IPO market in specific AI companies, which may happen in the future but is not yet here. We are not saying that one day there cannot ultimately be a bubble—we are all still human, and human behaviors create bubbles—but what we are not yet seeing one.

For those interested in hearing more about AI and the potential bubble, we recently hosted a webinar with Professor Jeremy Siegel and myself, which dives further into this topic: AI and the Markets.

Categories

Related articles

When Space Leaves the Blueprint and Enters the Economy

The Other Direction: How AI Could Become the Operating System for Quantum Computing

Battlefield-Proven: How the Drone Revolution Maps onto WisdomTree's Physical AI, Humanoids & Drones Strategy

The Drone Dominance Map: China's Lead, America's Response, and the Supply Chain That Will Determine the Outcome

The Nexus of Quantum Computing and the AI Trade

Real Estate Has Been Quietly Redefined. Most Portfolios Haven’t Caught Up.

Quantum Computing Goes Mainstream: What Two Executive Orders Mean for Investors

The Platforms: Why the Tech Giants Are Always in the Room

The First Mass-Market Robots May Not Walk. They May Fly.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.