The Fed’s Lending a Hand

Published March 29, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

We’re just past the two-week point in the latest episode of bank woes, and the markets continue to grapple with the aftereffects. What started out as more of a U.S.-centric regional bank concern has now moved across the Atlantic to infect some well-known bank names in Europe.

If you’re looking for any silver lining in the current situation, global central banks, led by the U.S. Federal Reserve, have acted quickly to try and stem potential systemic damage. The debate will certainly continue as to how it could have gotten to this point, but this blog post is going to focus more on the action the Fed has taken and how it is playing out thus far.

Although the Fed did ultimately raise rates by another 25 basis points (bps) at the March FOMC meeting, there was considerable debate about whether the voting members would refrain from any further rate hikes, given some of the dislocations created by the banking woes.

In fact, as of this writing, Fed Funds Futures have removed the possibility for another increase at the May FOMC gathering for just this reason. However, from the Fed’s point of view, an important distinction needs to be made. The U.S. policy makers view tools, such as Fed Funds, from more of a monetary policy perspective, i.e., for economic and/or inflation considerations. Dislocations in markets, specifically for funding purposes, can be addressed by using other tools and facilities, such as the recently announced Bank Term Funding Program (BTFP), which itself represents an enormous amount of potential lending availability for banks/depository institutions.

Fed Balance Sheet: Dollar Change in Lending Facilities

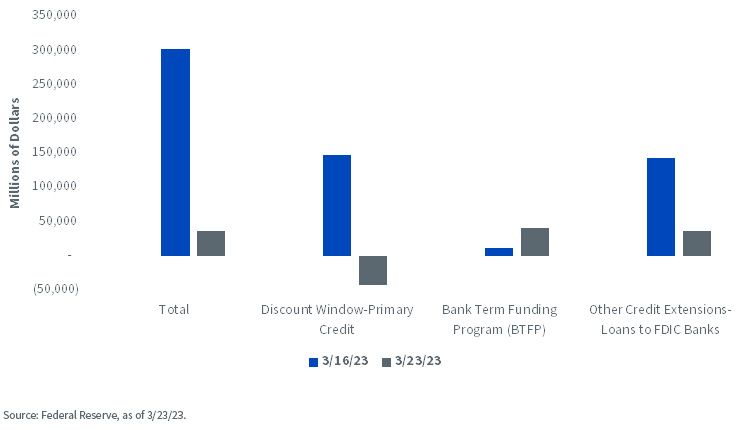

So, let’s take a look at how things are panning out from this perspective. The Fed releases their balance sheet every Thursday at 4:30 p.m. ET, and this is where investors can find insights into how these types of lending facilities are being utilized. There are three key items on the Fed’s balance sheet where this information can be found: the discount window for primary credit, BTFP and other credit extensions for loans to FDIC banks.

There is no doubt that in the immediate aftermath of the Silicon Valley Bank (SVB) failure, banks and depository institutions took advantage of what the Fed was offering. The total amount of these three areas of bank lending surged by $303 billion in the week of March 16. To provide perspective, in the pre-SVB world (March 9), this total amount was only $219 million. All three aforementioned line items rose as well, but the more notable increases came from the discount window ($148.3 billion) and the other credit extension component ($142.8 billion). Use of the ‘new’ BTFP facility was much lower at $11.9 billion.

For the just completed week of March 23, there was noticeably less usage of these facilities. The total increase dropped to $36.1 billion, as gains of $41.7 billion for BTFP and $37.0 billion in other credit extensions was partially offset by an outright decline in borrowing at the discount window of -$42.6 billion.

Conclusion

If you are looking for a silver lining at this stage of the game, the drop-off in usage of the Fed’s lending facilities falls into that category. Without a doubt, it’s still early in the process, and I’m well aware of how things can change quickly and not necessarily for the good. However, the Fed’s tools on this front are working like they are supposed to, and that is good news.

Categories

Related articles

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

Nowhere to Hide…Except Maybe Treasury Floating Rate Notes

How to Mitigate Software Exposure in Bonds

Fed Watch: Between a Rock and a Hard Place

One Week Later

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.