Fixed Income: A Return to Normalcy

Published December 7, 2022

Kevin Flanagan

Head of Investment and Fixed Income Strategy

While 2022 was arguably one of the worst, if not actually the worst, years for the U.S. bond market in modern history, a silver lining has emerged. Indeed, with yield levels surging across the asset class spectrum, one could conclude that a semblance of ‘normalcy’ has returned to the fixed income arena.

Up until this year, the one major question I was always asked was: Where can I find yield in the bond market? To be sure, with U.S. rates being dragged down by zero interest rate (ZIRP) central bank policies, negative sovereign debt yields abroad and a lack of inflation, to name a few key factors, investors had been left with historically low yield levels, a new normal for the bond market.

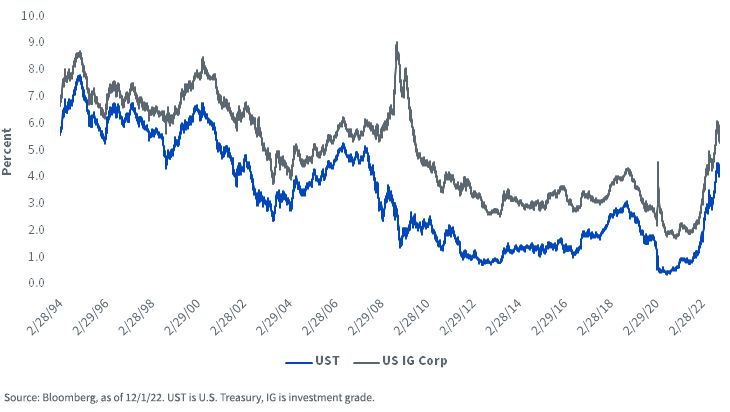

UST & U.S. IG Corporate: Yield to Worst

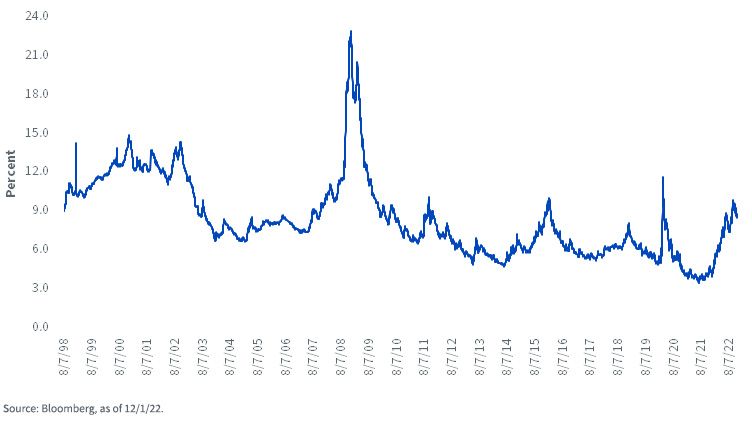

U.S. High Yield: Yield to Worst

As we are about to embark on a new calendar year, the fixed income landscape has changed dramatically. As I mentioned in a prior blog post, I would argue that the historically low yield levels of the last 10 to 15 years were “abby normal,” to quote the movie Young Frankenstein, and that investors are now witnessing what normal looks like when central banks are no longer pursuing ZIRP and are actually tightening monetary policy because of inflation.

This new rate regimen has brought Treasuries (UST), investment-grade (IG) corporates and high-yield (HY) corporates all back to familiar pre-global financial crisis territory, arguably the genesis of the abnormal yield structure for the last decade or so (see graphs). For Treasuries, that means a yield to worst reading at or around 4%, and for U.S. IG corps, levels over the 5% threshold. Perhaps one of the more intriguing developments has been the rise in HY into the 8%–9% range. Compare these readings to where they were just a year ago: UST 1.12%, U.S. IG corps 2.29% and HY 4.74%.

Conclusion

From an investment backdrop, investors now have some definitive options within the fixed income arena. In fact, even though Fed Chairman Powell has signaled the potential for some slowing in the pace of rate hikes, perhaps as soon as next week’s FOMC meeting, he also emphasized that rates could be heading higher for longer, with no apparent appetite to reverse course anytime soon. So, if I was asked the aforementioned question about where to find yield in the bond market now, my answer has now become a much easier one.

Indexes:

- Treasuries: Bloomberg U.S. AGG Treasury Yield to Worst

- IG Corps: Bloomberg U.S. AGG Corporate Yield to Worst

- High Yield: Bloomberg U.S. Corporate High Yield Yield to Worst

For more insights, please visit our Fixed Income Strategy page.

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.