Where Will It All End?

Where will it all end? That’s the question on investors’ minds these days when it comes to interest rates. While the focus has been on the Fed Funds Target range in the wake of last week’s FOMC meeting, there is also another component to this query: the Treasury (UST) 10-Year yield.

The Fed certainly made headlines at the just completed September FOMC meeting with their internal projections for the Fed Funds Rate. According to their median estimates, the policy makers are looking for the overnight money target to come in at 4.40% for the end of this year and 4.60% for 2023. Ok, now that we got that covered (insert laugh track here), what about that UST 10-Year yield?

Without a doubt, many factors come in to play when trying to determine the fate of the UST 10-Year. Filed under the obvious would be the state of the U.S. economy, and of course, inflation. Also, flight-to-quality and supply considerations, technical analysis and don’t forget, quantitative tightening (QT) can all potentially play important roles in the process as well.

Nominal vs. Real Yields

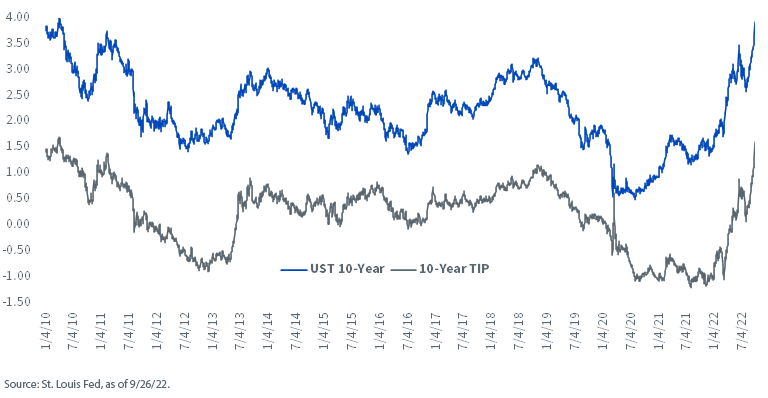

However, there is one aspect to this analysis I have blogged about in the recent past that also warrants attention: developments in real yields, or the TIPS market. In this case, we would be focusing on the Treasury 10-year TIP.

After residing in negative territory for the better part of 2021 and early 2022, real yields have now moved back decisively into the plus column. In addition, this move into positive territory has been swift, and rather noteworthy. To provide perspective, as recently as March 8 of this year, the 10-year TIP yield was as low as -1.07%, but as of this writing, the level has risen to 1.66% on an intra-day basis, an incredible turnaround in a relatively short period. By hitting this new interim peak, the 10-year TIP yield blew though the 2011 high watermark of 1.38%. And guess what other Treasury security has been following in lockstep? The UST 10-Year note.

As the above graph illustrates, this is not just a 2022 phenomenon either, but rather an historical correlation between the two. As the 10-year TIP broke above its high point from both the last rate hike cycle (1.16%) and 2011 (1.38%), the UST 10-Year yield went through the 3.50% threshold to hit 3.99%.

The next interim peak for the 10-year TIP is 1.68%, a reading that was registered in 2010. When the 1.68% real yield was printed in 2010, the UST 10-Year yield came in at 3.99%.

Conclusion

While this blog post focused on a ‘4%’ UST 10-Year yield, don’t forget, the recent selling pressure in the UST market has not been confined to any one maturity, as the spike in yields has been widespread. In fact, the UST 2- & 5-Year yields are trading at levels not seen since 2007.

The natural question to ask is, if the Fed does raise the Fed Funds Target to over 4%, will the UST 10-Year yield follow close behind? Looking at upcoming trends for real yields could offer a useful clue.

Share & Comment

Popular Posts

Categories

Related Links