Risk Factors Are Rotating Back into Focus

This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

Regular readers of the WisdomTree blogs know that we write frequently about risk factor diversification. As we approach the halfway point of what has been a very turbulent 2022, it is time to revisit this important topic.

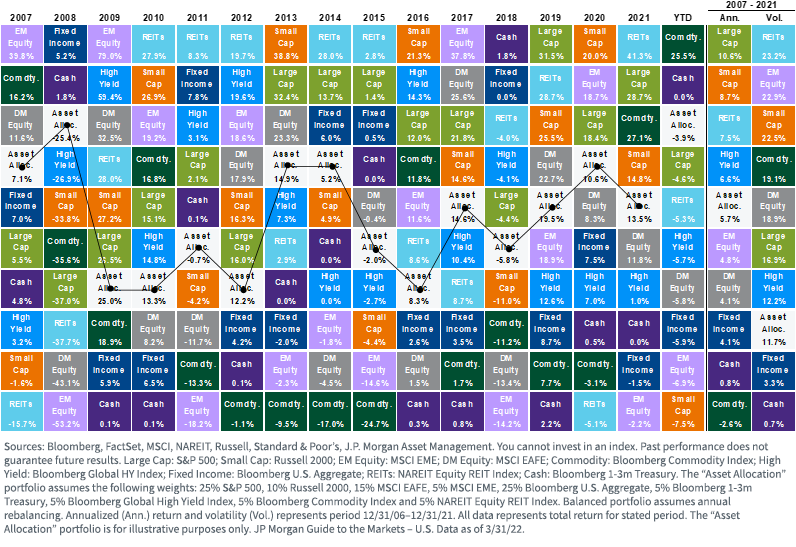

As a reminder, most investors are familiar with the visual of an asset class “performance quilt,” which highlights the importance of asset class diversification.

For definitions of terms in the image above, please visit the glossary.

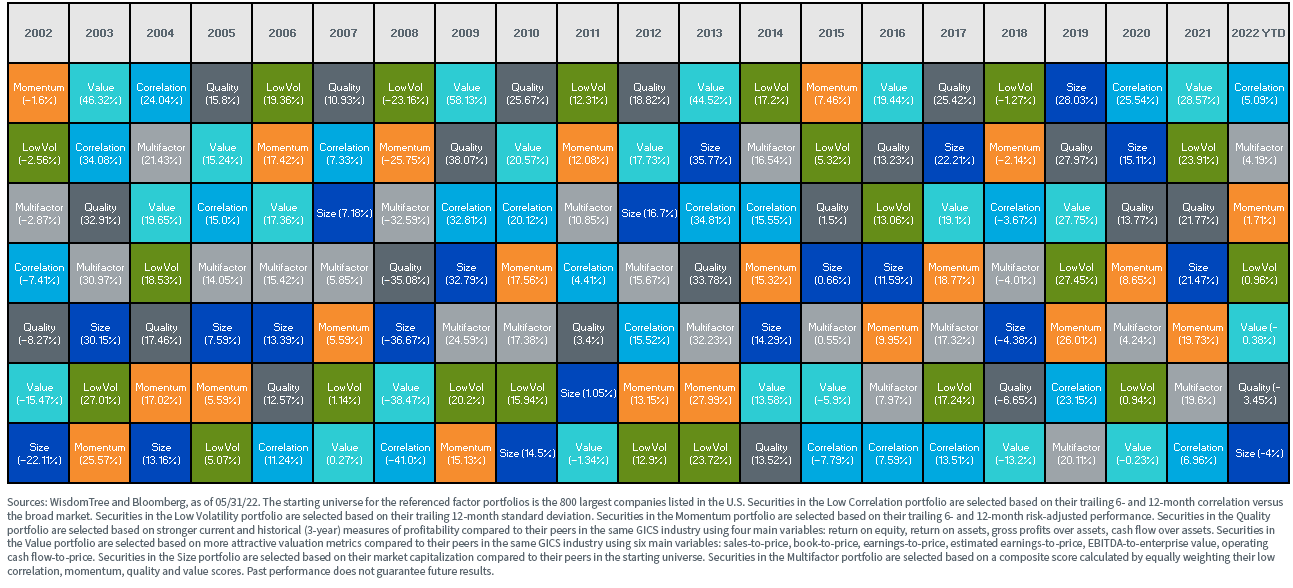

But we believe risk factor diversification is equally as important as asset class diversification. And risk factor performance can be as difficult to forecast as asset class performance.

For definitions of terms in the image above, please visit the glossary.

For definitions of terms in the image above, please visit the glossary.

Year-to-Date Review

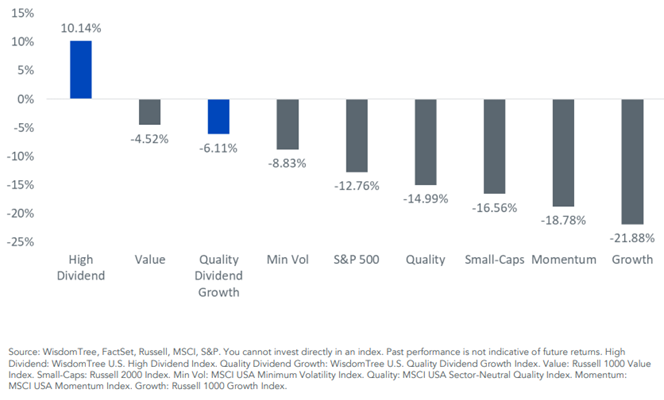

The first half of 2022 was unusual in the sense that bonds did not provide the hedge to equity risk they historically have.

For definitions of terms in the image above, please visit the glossary.

Certain equity risk factors, specifically dividends and value, were more effective hedges to broad market equity risk.

Conversely, the rising interest rate environment over the first half caused havoc with growth stocks (i.e., stocks whose cash flows are expected further out in the future and so whose “discounted cash flow” valuations are therefore more sensitive to rising rates).

U.S. Factor Return YTD, as of 5/31/22

For definitions of terms in the image above, please visit the glossary.

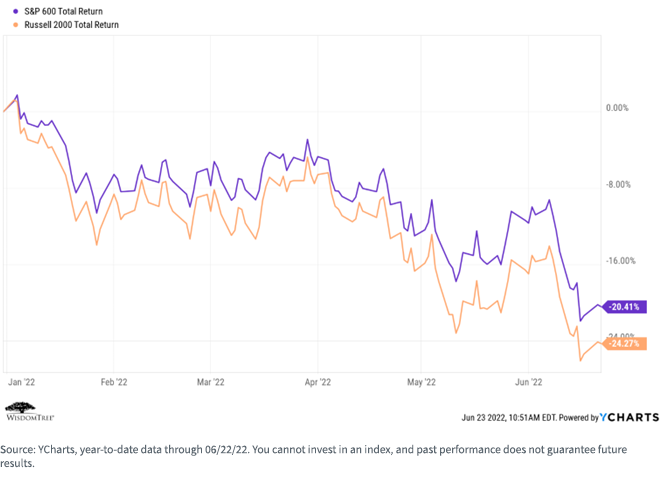

Within small-cap stocks, we also see that quality was an important risk mitigator (using the S&P 600 versus the Russell 2000 indexes as proxies for the quality factor, as the S&P 600 index excludes far more negative earnings companies than the Russell 2000 index).

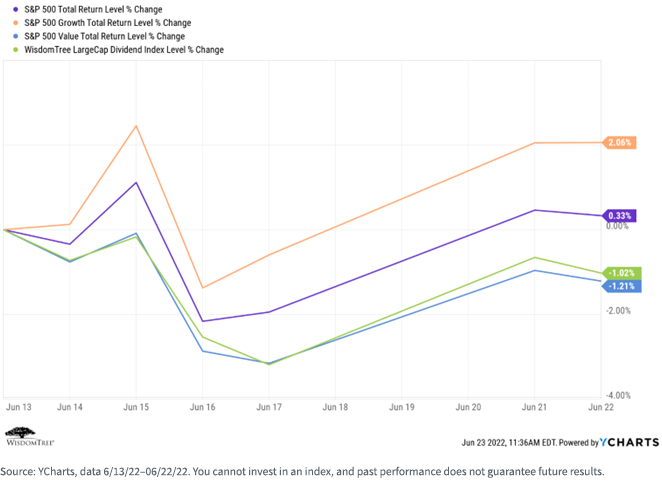

As a final factor to examine, let’s look at size. Within U.S. large-cap stocks, we see year-to-date (YTD) outperformance by the smaller-cap stocks within the index (using the S&P 500 equal-weighted index as a proxy for those smaller-cap stocks).

For definitions of terms in the image above, please visit the glossary.

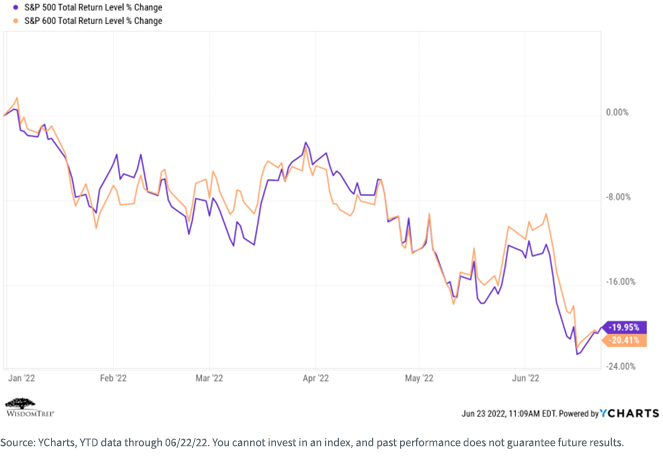

But, at a broader level, U.S. large-cap stocks outperformed U.S. small-cap stocks.

We saw similar (and more dramatic) YTD underperformances with EAFE and EM small-cap stocks in comparison to their respective large-cap indexes, though non-U.S. small-cap stocks have outperformed non-U.S. large-cap stocks over longer time horizons (e.g., 10 years).

Outlook for the Remainder of 2022

As the Fed (and other central banks) engages in more aggressive rate hike regimes, we see the market interpreting that as a signal for impending recession. The result has been a mini rally in growth stocks over the past two weeks as investors have leaned away from value-oriented sectors such as financials, utilities and especially energy.

For definitions of terms in the image above, please visit the glossary.

Despite this, we believe that value and dividends will outperform over the remainder of the year. We further believe that quality will become increasingly important as we head into an uncertain economic environment marked by generally rising interest rates and increased market volatility. We believe that investors will once again refocus on companies that exhibit stronger earnings, cash flows and balance sheets.

For valuation-driven (and therefore longer-term) investors, U.S. small-cap stocks present an interesting potential opportunity—the market has driven small-cap valuations down, seemingly in expectation of a sooner-than-we-expect recession.

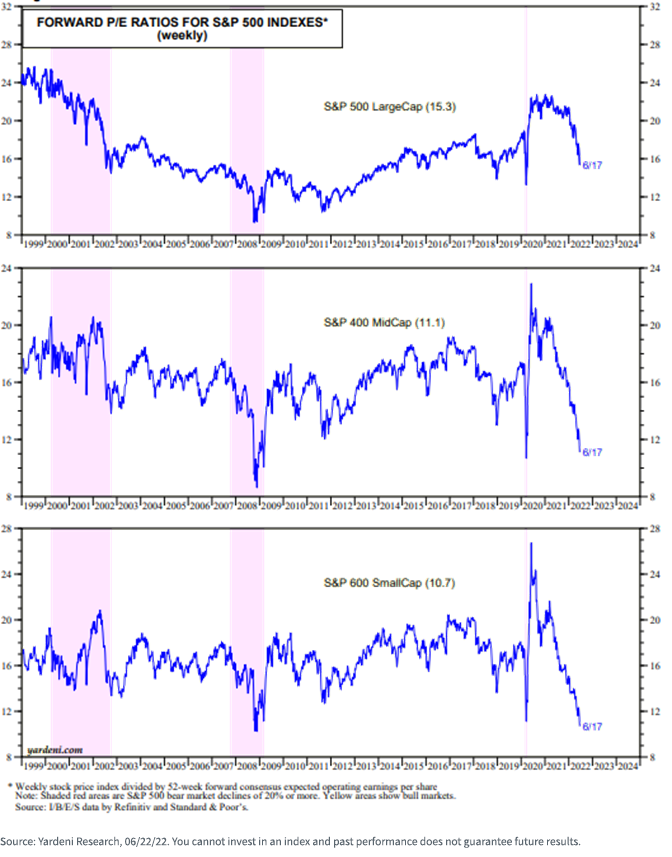

Let’s compare commonly-used valuation metrics of the S&P large cap and small cap indexes (labeled “500” and “600”, respectively, in the chart below) – we see a significant discount in the small cap index numbers versus the large cap index numbers. Since what you can earn on any investment is at least partially a function of how much you pay for it today, longer-term investors may see a relative attraction to small cap stocks, despite the current market environment.

A more historical perspective tells a similar story—despite the downturn so far this year, mid- and small-cap stocks remain more attractively valued than large-cap stocks.

Conclusions

Given the factor tilts inherent in many, if not most WisdomTree strategies (dividends, value, size and quality), we remain comfortable with the positioning and allocations within our Model Portfolios. Most of our strategic models are benefitting from these factor tilts and are beating their respective benchmarks YTD.

Given the difficulty in forecasting asset class and risk factor performances, however, we intentionally diversify our portfolio at both of those levels.

As a reminder, almost all publicly available WisdomTree Model Portfolios have certain common characteristics:

- They are global in nature

- They are diversified at both the asset class and risk factor levels

- They are ETF-focused, to optimize fees and taxes

- We charge no strategist fee

We are an open-architecture shop (that is, all our Models include both WisdomTree and third-party products) for many reasons: (a) it’s the right thing to do, (b) it’s what end clients assume, and advisors expect, and (c) it allows us to build more risk factor-diversified portfolios.

We like the factor tilts currently embedded in our Model Portfolios, as we believe dividends, value and quality will continue to shine as we move through 2022. We also believe size may be positioned for a positive rotation.

Given our strategic investment mandates, however, we also remain diversified at both the asset class and risk factor levels.

Important Risks Related to this Article

Neither diversification nor an asset allocation strategy assures a profit or eliminates the risk of experiencing investment losses.

For retail investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. The performance of your account may differ from the performance shown for a variety of reasons, including but not limited to: your investment advisor, and not WisdomTree, is responsible for implementing trades in the accounts; differences in market conditions; client-imposed investment restrictions; the timing of client investments and withdrawals; fees payable; and/or other factors. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

For financial professionals: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy. In providing WisdomTree Model Portfolio information, WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor or end client, and has no responsibility in connection therewith, and is not providing individualized investment advice to any advisor or end client, including based on or tailored to the circumstance of any advisor or end client. The Model Portfolio information is provided “as is,” without warranty of any kind, express or implied. WisdomTree is not responsible for determining the securities to be purchased, held and/or sold for any advisor or end client accounts, nor is WisdomTree responsible for determining the suitability or appropriateness of a Model Portfolio or any securities included therein for any third party, including end clients.

Advisors are solely responsible for making investment recommendations and/or decisions with respect to an end client and should consider the end client’s individual financial circumstances, investment time frame, risk tolerance level and investment goals in determining the appropriateness of a particular investment or strategy, without input from WisdomTree. WisdomTree does not have investment discretion and does not place trade orders for any end client accounts. Information and other marketing materials provided to you by WisdomTree concerning a Model Portfolio—including allocations, performance and other characteristics—may not be indicative of an end client’s actual experience from investing in one or more of the funds included in a Model Portfolio. Using an asset allocation strategy does not ensure a profit or protect against loss, and diversification does not eliminate the risk of experiencing investment losses. There is no assurance that investing in accordance with a Model Portfolio’s allocations will provide positive performance over any period. Any content or information included in or related to a WisdomTree Model Portfolio, including descriptions, allocations, data, fund details and disclosures, is subject to change and may not be altered by an advisor or other third party in any way.

WisdomTree primarily uses WisdomTree Funds in the Model Portfolios unless there is no WisdomTree Fund that is consistent with the desired asset allocation or Model Portfolio strategy. As a result, WisdomTree Model Portfolios are expected to include a substantial portion of WisdomTree Funds notwithstanding that there may be a similar fund with a higher rating, lower fees and expenses or substantially better performance. Additionally, WisdomTree and its affiliates will indirectly benefit from investments made based on the Model Portfolios through fees paid by the WisdomTree Funds to WisdomTree and its affiliates for advisory, administrative and other services.

Share & Comment

Popular Posts

Categories

Related Links