Can Powell Hit a Curve Ball?

Here we are in March and the money and bond markets are geared up for the first Federal Funds Rate increase since December 2018. Certainly, Powell & Co. are facing an unusual backdrop to begin this rate hike cycle. Obviously, the latest headlines surrounding Russia’s invasion of Ukraine come to mind as well as the fact we are emerging from a historical global pandemic. In addition, the Fed is confronted with the highest inflation setting in 40 years. This blog post, however, is going to focus on the shape of the yield curve as we approach liftoff, and raises the question of how the Fed will approach this tightening cycle as a result.

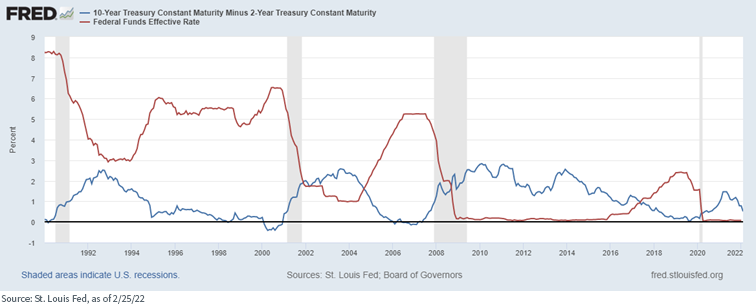

With respect to the yield curve, my focus is on the spread between the U.S. Treasury (UST) 2-Year yield versus the 10-Year yield. The graph below highlights the shape of the aforementioned Treasury yield curve as compared to the level of the effective Federal Funds Rate going back to 1990. As a result, investors get a nice glimpse of what the shape of the yield curve looked like at the time the Fed was beginning to raise the Fed Funds Rate.

Upon closer inspection, it becomes increasingly apparent the yield curve is rarely this flat heading into a prolonged rate hike cycle. In fact, other than the 1999 tightening episode, the yield curve has never been this narrow over the last 30 years or so of tightening. Let’s look at what the UST 2s/10s spread has been at the start of rate hikes over this time span:

- 1994–1995 rate hike cycle: +150 basis points (bps)

- 1999–2000 rate hike cycle: +29 bps

- 2004–2006 rate hike cycle: +197 bps

- 2015–2018 rate hike cycle: +126 bps

- March 2022: +39 bps

With the yield curve being as narrow as it is currently, the question revolves around how fast it could actually become inverted. This is an outcome the Fed would probably like to avoid, especially this early in the game. An inverted curve toward the end of a rate hike cycle is not unusual, but a negative UST 2s/10s spread at the beginning of the process is not ideal, to say the least. If the policy makers were to implement 100 bps worth of rate increases through their July 2022 FOMC meeting, it is reasonable to assume the curve could very well invert.

Can the Fed do anything to combat this result? As we’ve discussed before, this is where their balance sheet could come into play. If the Fed begins to let their Treasury and MBS holdings roll off early in the rate hike process, it could, in theory, help put upward pressure on maturities such as the 10-Year and could serve to somewhat offset the increase in short-term yields. This point was underscored just recently by voting member St. Louis Fed President Bullard on the Behind the Markets podcast.

Conclusion

As investors continue to digest the headlines surrounding liftoff and what the Fed’s policy path may look like in 2022, and next year for that matter, there is no doubt the investment backdrop is clearly different than what we’ve seen in the past.

Share & Comment

Popular Posts

Categories

Related Links