Your Move Jay Powell

08/09/2021

One of the key pillars for the Fed to begin a more active exit strategy was “substantial progress” in the labor market. With the July jobs report, it looks like the Fed will need to make some decisions, perhaps sooner rather than later. Here’s a look at the latest numbers:

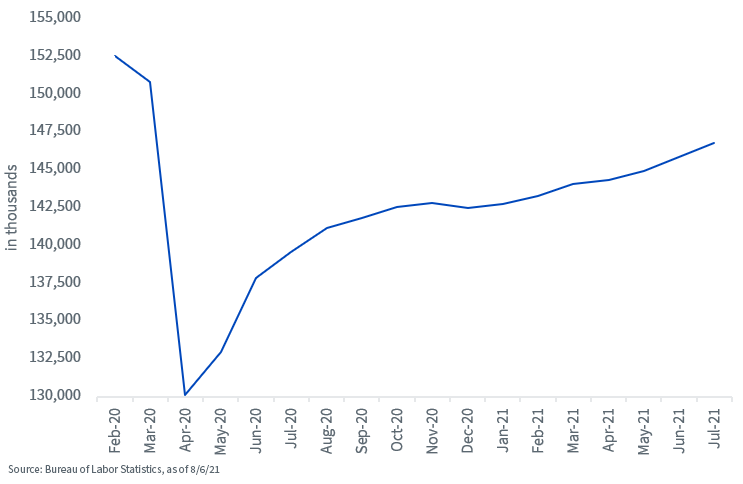

- Total nonfarm payrolls rose by 943,000, beating the consensus estimate of 870,000 handily. In addition, the prior two months’ tallies were revised upward in a noticeable fashion. Thus, the U.S. jobs market has now produced back-to-back gains in excess of 900,000.

- The breadth of job gains was rather wide as well. The usual suspects (leisure & hospitality) continued their comeback from pandemic lows, but both private service-providing and government payrolls (local government) contributed to the better-than-expected performance in July.

- Overall payrolls are still not back to their pre-pandemic levels, but they have now re-couped 75% of the March/April 2020 plunge.

Total Nonfarm Payrolls

- The unemployment rate dropped 0.5 percentage points to 5.4%, once again beating expectations (5.7%) in a noticeable fashion. In fact, within the household survey of the jobs report, civilian employment topped the million mark at 1,043,000.

- Another key development was the solid gain in average hourly earnings, with the year-over-year increase placed at 4.0%. It definitely appears as if the demand for labor coming from the pandemic recovery is putting upward pressure on wages, a development the BLS also noted in the report.

- Chairman Powell’s “inflation is transitory” argument will fall apart if wages join the party.

- There is no Fed meeting until September 22, but it appears as if some FOMC members are getting a little restless. We still have one more jobs report to go before then, but the July jobs report plays into the narrative that the Fed will make a taper announcement at this meeting, with Powell’s expected Jackson Hole appearance later this month potentially being used as a ‘signal’ to the markets as to what’s coming.

Conclusion

The UST 10-Year yield could be poised for round two of higher yields. After testing the Fibonacci 50% retracement level twice in recent weeks, and essentially failing both times, the fundamental and technical setting for the 10-Year suddenly look less friendly. Against this backdrop, I continue to suggest investors deploy rate-hedge strategies for their fixed income portfolios.

Share & Comment

Popular Posts

Categories

Related Links

About the Contributor

Head of Fixed Income Strategy

As part of WisdomTree’s Investment Strategy group, Kevin serves as Head of Fixed Income Strategy. In this role, he contributes to the asset allocation team, writes fixed income-related content and travels with the sales team, conducting client-facing meetings and providing expertise on WisdomTree’s existing and future bond ETFs. In addition, Kevin works closely with the fixed income team. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S in Finance from Fairfield University.

Follow Kevin Flanagan

@KevinFlanaganWT