Revisiting “Disruptive Growth”

This article is relevant to financial professionals who are considering offering Model Portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

Don’t worry, about a thing

’Cause every little thing, gonna be all right

Singin’, don’t worry, about a thing

’Cause every little thing, gonna be all right

(From “Three Little Birds” by Bob Marley, 1977)

In February, we posted a blog piece about our Disruptive Growth Model Portfolio. Two of our primary investment themes for 2021 and beyond are “disruptive growth” and thematic investing. As a reminder, we believe that, even as the global economy reopens and recovers, the COVID-19 pandemic fundamentally and perhaps permanently altered the way we work and socialize, and take care of and entertain ourselves.

We believe this has led to dramatic growth in certain “thematic” megatrends, and we think these trends will be with us for years to come. This prompted us to launch our disruptive growth model in August of last year. We identified six thematic sectors and ETFs and built a diversified portfolio accordingly. It is intended for growth-focused advisors and end clients who can tolerate highly valued companies and potentially higher volatility in exchange for potentially higher long-term growth rates.

The six sectors we are currently allocate to include cloud computing (via our own WCLD), diversified platform-based companies (via our own PLAT), cybersecurity, financial technology, genomics and biotechnology, and online gaming and e-sports.

How is the portfolio performing?

Like many technology firms and the so-called “FAANGM” stocks—Facebook, Amazon, Apple, Netflix, Google (Alphabet) and Microsoft1—the ETFs in the disruptive growth model hold many highly valued companies that currently do not generate much in the way of current earnings or dividends. That is, investors are paying high valuations today in exchange for the potential of higher earnings in the future.

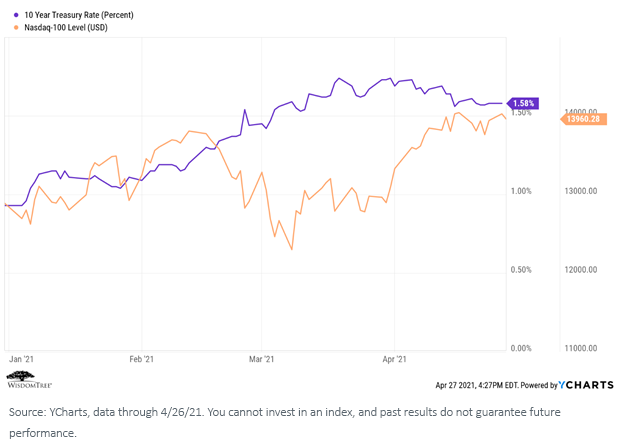

Thus, when interest rates began rising late last year and through roughly mid-March of this year, many of those stocks fell fairly hard. The NASDAQ-100 Index holds many similarly valued companies, and here is a YTD comparison of the rise in the 10-Year Treasury rate and the performance of that Index.

Note (a) the sharp decline in the NASDAQ-100 commensurate with the sharp increase in rates beginning in February, but also (b) the stabilization of the NASDAQ-100 over the past few weeks (it is once again positive for the year) as rates have also stabilized.

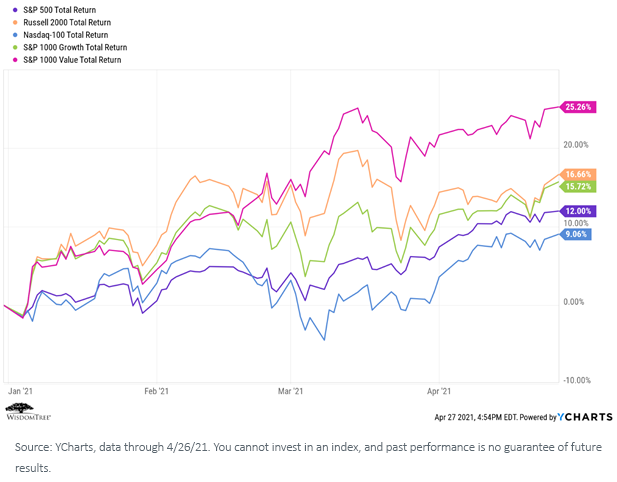

It’s not that growth stocks have performed badly in 2021. They simply have not kept up with the cyclical rotation trades (small cap and value)—a phenomenon advisors and investors have not seen for most of the past 10 years.

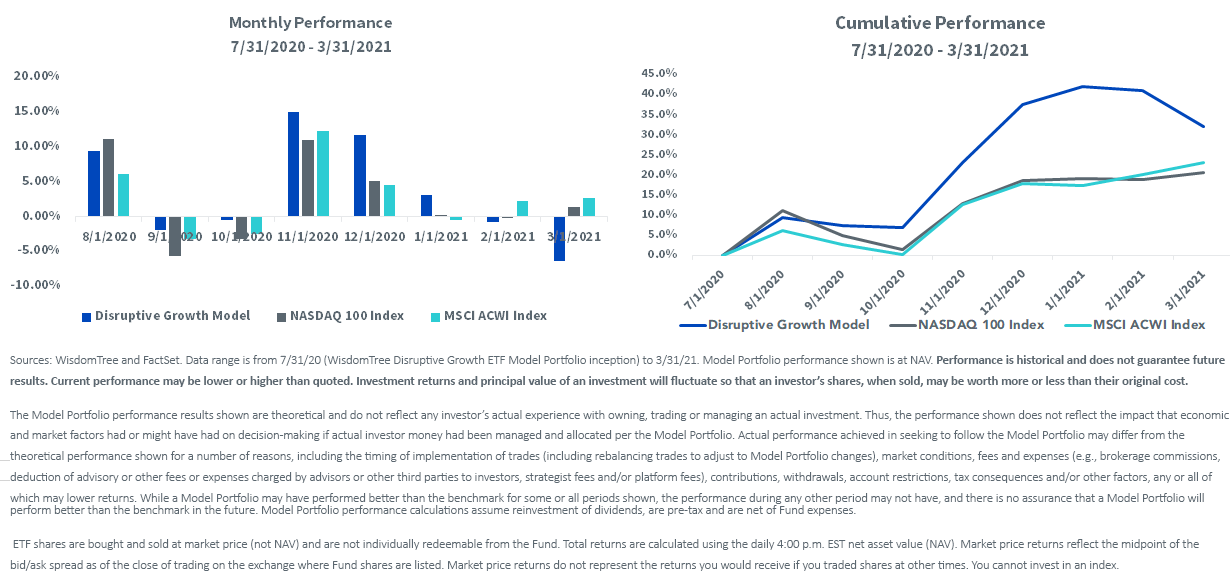

The disruptive growth model shows similar performance characteristics as the NASDAQ-100 Index. It actually holds more highly valued positions and so fell faster when rates rose, but it is recovering and has been outperforming the NASDAQ-100 since inception on July 31, 2020.

Click here for standardized performance.

In addition, although three of our current six ETF allocations have generated slightly negative performance YTD (NAV) over their common investment period dating back to October 2019, each of those individual six strategies has shown high double-digit returns (NAV).2

The portfolio also continues to show a distinct lack of security overlap between the different allocations. As of March 31, 2021, no two of the current six ETF positions have had more than 18% of securities overlap each other, and most had less than 10%. (Holdings and weightings are subject to change.) There likewise is a nice diversification of sector exposures.

This portfolio carries high valuations corresponding to its high growth rates, and its performance will likely continue to be influenced by changing interest rates and may be volatile (and has been YTD), but we believe the level of diversification provided by the current lack of sector and securities overlap will help to generate a more consistent performance while still taking advantage of each individual strategy’s potential future growth.

Conclusion

With COVID-19 vaccinations accelerating and the global economy in what we believe is the early stages of a steady recovery, we anticipate that 2021 generally will be a constructive “risk-on” market environment.

We believe our disruptive growth investment theme will play out well in this environment, as will our corresponding Model Portfolio. It can be allocated to as a stand-alone equity model or as a complementary “sleeve allocation” in broader portfolios where advisors are seeking to improve performance. Financial advisors registered on the WisdomTree website can learn more about this and other WisdomTree models by accessing our newly launched Model Adoption Center (“MAC”).

Despite recent volatility, we continue to like how we are positioned to take advantage of what we believe will be enduring megatrends in global markets. So, for the most part, we are “not worrying about a thing.”

1As of March 31, 2021, the WisdomTree ETF PLAT held positions in Alphabet (9.35%), Microsoft (8.02%), Amazon (7.05%) and Facebook (6.80%), but it did not hold positions in Netflix or Apple. The WisdomTree ETF WCLD does not hold any positions in any of the “FAANGM” stocks.

2Past performance does not guarantee future results.

Important Risks Related to this Article

WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy. In providing WisdomTree Model Portfolio information, WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor or end client, and has no responsibility in connection therewith, and is not providing individualized investment advice to any advisor or end client, including based on or tailored to the circumstance of any advisor or end client. The Model Portfolio information is provided “as is,” without warranty of any kind, express or implied. WisdomTree is not responsible for determining the securities to be purchased, held and/or sold for any advisor or end client accounts, nor is WisdomTree responsible for determining the suitability or appropriateness of a Model Portfolio or any securities included therein for any third party, including end clients. Advisors are solely responsible for making investment recommendations and/or decisions with respect to an end client and should consider the end client’s individual financial circumstances, investment time frame, risk tolerance level and investment goals in determining the appropriateness of a particular investment or strategy, without input from WisdomTree. WisdomTree does not have investment discretion and does not place trade orders for any end client accounts. Information and other marketing materials provided to you by WisdomTree concerning a Model Portfolio—including allocations, performance and other characteristics—may not be indicative of an end client’s actual experience from investing in one or more of the funds included in a Model Portfolio. Using an asset allocation strategy does not ensure a profit or protect against loss, and diversification does not eliminate the risk of experiencing investment losses. There is no assurance that investing in accordance with a Model Portfolio’s allocations will provide positive performance over any period. Any content or information included in or related to a WisdomTree Model Portfolio, including descriptions, allocations, data, fund details and disclosures, are subject to change and may not be altered by an advisor or other third party in any way.

WisdomTree primarily uses WisdomTree Funds in the Model Portfolios unless there is no WisdomTree Fund that is consistent with the desired asset allocation or Model Portfolio strategy. As a result, WisdomTree Model Portfolios are expected to include a substantial portion of WisdomTree Funds notwithstanding that there may be a similar fund with a higher rating, lower fees and expenses or substantially better performance. Additionally, WisdomTree and its affiliates will indirectly benefit from investments made based on the Model Portfolios through fees paid by the WisdomTree Funds to WisdomTree and its affiliates for advisory, administrative and other services.

References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

PLAT: There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty; these risks may be enhanced in emerging, offshore or frontier markets. Technology platform companies have significant exposure to consumers and businesses, and a failure to attract and retain a substantial number of such users to a company’s products, services, content or technology could adversely affect operating results. Technological changes could require substantial expenditures by a technology platform company to modify or adapt its products, services, content or infrastructure. Technology platform companies typically face intense competition, and the development of new products is a complex and uncertain process. Concerns regarding a company’s products or services that may compromise the privacy of users, or other cybersecurity concerns, even if unfounded, could damage a company’s reputation and adversely affect operating results. Many technology platform companies currently operate under less regulatory scrutiny, but there is significant risk that costs associated with regulatory oversight could increase in the future. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WCLD: There are risks associated with investing, including possible loss of principal. The Fund invests in cloud computing companies, which are heavily dependent on the Internet and utilizing a distributed network of servers over the Internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the Internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links