India: An Unsung Hero in EM?

For many investors, emerging markets (EM) have become synonymous with China, and it’s easy to understand why. China has been the only global economy to navigate the COVID-19 pandemic relatively unscathed, despite hawkish rhetoric from Washington, tariff threats and deteriorating geopolitical relationships.

As a result, the region’s darling economy has ballooned to constitute 39% of the MSCI Emerging Markets Index and remains paramount for EM returns.

But despite China’s outsized influence, there is another player worthy of attention in emerging markets. India may only account for 9% of the MSCI EM Index, but we are watching a few key catalysts that may propel it in 2021:

- Cyclical Recovery: After a year of halted economic activity, even a modest resumption in growth, encouraged by COVID-19 vaccine distribution, may bode well for sectors that struggled in 2020. Cyclical stalwarts such as Financials, Industrials and Materials may enjoy a long overdue rally.

- Earnings Revival: A corollary to the cyclical recovery, earnings growth may finally resume in 2021 alongside economic activity. With profitability restored, equity prices could benefit from markets’ renewed enthusiasm and confidence.

- Perfect Storm of Policy: While the pandemic introduced unprecedented challenges in 2020, it also provoked unprecedented responses from central banks and fiscal authorities. We expect the global environment of accommodative monetary policy, coupled with fiscal stimulus, to continue well into 2021 and beyond. The Reserve Bank of India (RBI), India’s central bank, intends to follow suit, as many economists are expecting another 50-basis-point interest rate cut to support the recovery.

- Emerging Markets in Vogue: A byproduct of the low-rate environment is renewed interest in foreign markets. Low rates, coupled with weakness in the U.S. dollar, or “USD” (and the possibility of further USD depreciation in 2021), are traditionally a tailwind for risk-on assets, and EM in particular.

India has already begun to benefit from the recent optimism. Its BSE SENSEX Index eclipsed the 50,000 level in January, nearly doubling since its recent low in March 2020. Likewise, it has been an attractive destination for fund flows since the onset of the pandemic. After significant outflows in March of last year, India saw positive flows in every subsequent month, except for modest outflows in April and September.1

There’s More Than Meets the Eye in India

WisdomTree has a potential solution poised to capitalize on India’s potential. The WisdomTree India Earnings Fund (EPI) targets Indian equities with an emphasis on profitability. Constituents are weighted based on their earnings per share over the past year, resulting in three features that would complement the trends above:

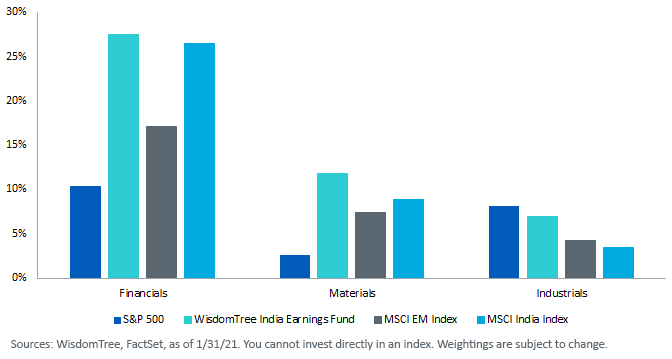

1) Sectors Positioned for a Cyclical Recovery. The Financials, Materials and Industrials sectors make up more than 46% of the Fund, levering it to the level of global economic activity, which may perform well if growth resumes. Likewise, these positions result in a 7% over-weight to the market capitalization-weighted MSCI India Index. For comparison, these three sectors only account for 21% of the S&P 500 Index and 29% of the broader MSCI EM Index.

Cyclical Sector Comparison

2) Diversification Benefits. EPI is the second-largest Fund by total assets in the U.S. Fund – India Equity category, classified by Morningstar. It is also by far the most diversified, with more than 340 constituents in the Fund compared to the category average of 92. The Fund is also less concentrated than its competitors. As of January 21, the top 10 holdings constitute about 40% of the Fund, compared to the 48% category average, with many others in the 50%–70% range.

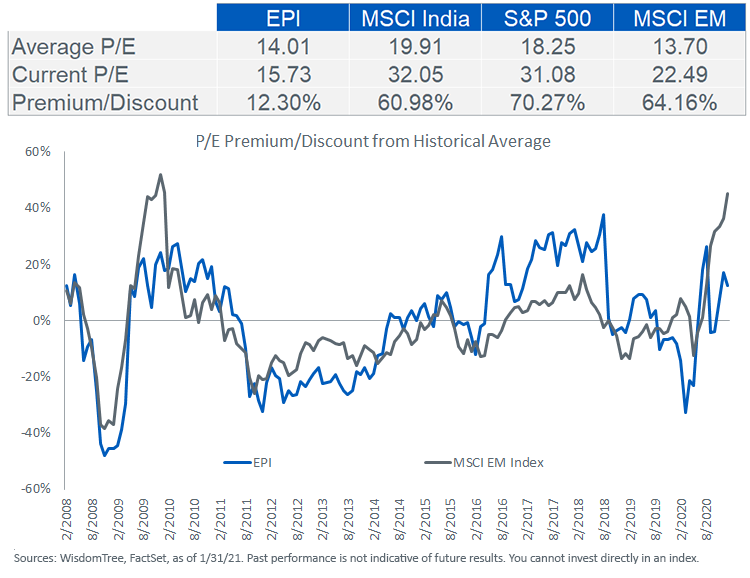

3) Earnings Are the Common Denominator. Companies are weighted by Earnings Streams, which helps to mitigate valuations during periods of elevated market pricing. EPI has an inherent focus on controlling valuations, since an earnings-focused methodology tends to over-weight in the lower P/E ratio companies while under-weighting in the higher P/E ones, or those most at risk if valuations recede. EPI is currently trading at a 12% premium to its average P/E since inception (2/22/08). Meanwhile, market cap-weighted India, the S&P 500 and broader EM are all trading at premiums of 60%–70%. Moreover, while MSCI India is trading at a 48% premium to broad emerging markets, EPI is actually trading at a 30% discount to the broader region.

Since the pandemic introduced unprecedented challenges in 2020, investors are hungry for new opportunities, and we believe an earnings-weighted methodology in India is a compelling one now more than ever. At a net expense ratio of only 0.84%, we have a strong conviction that the WisdomTree India Earnings Fund may provide the means to benefit from potential catalysts in the region.

Unless otherwise stated, all data is sourced from WisdomTree, FactSet or Morningstar, as of 1/31/21.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. As this Fund has a high concentration in some sectors, the Fund can be adversely affected by changes in those sectors. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.Share & Comment

Popular Posts

Categories

Related Links

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.