How to Replace FAANGs with Cloud

If you were hoping for yet another contrived acronym to describe a group of stocks, you can stop reading now.

But if you are in the market for fast-growing technology companies that don’t face the same degree of uncertainty from trade wars or antitrust scrutiny, we think cloud-based businesses represent an attractive alternative to mega-cap companies in the Technology sector.

FAANG (Facebook, Amazon, Apple, Netflix, Google)1 stocks have tripled their market capitalization over the last decade and have been the main drivers of the S&P 500 Index’s return. But in the fourth quarter of 2018, they suffered meaningful drawdowns and bouts of volatility. When political tensions ratchet up, some investors could question whether it may be time to seek out a new engine of growth and returns.

In our view, cloud computing could represent one compelling alternative.

Recent Drawdowns

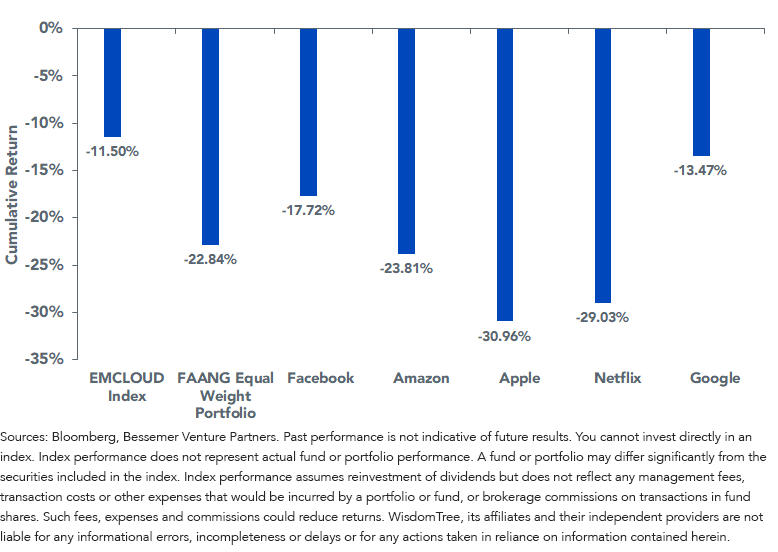

During the fourth-quarter of 2018 market swoon, FAANG stocks declined by 23%, on average. By contrast, cloud computing stocks (as proxied by the BVP Nasdaq Emerging Cloud Index, or EMCLOUD), also experienced volatility but fell by half as much compared with the FAANGs. The parent company of Google, Alphabet, was the most resilient, but it still underperformed EMCLOUD by nearly 200 basis points (bps). This was surprising given that cloud companies tend to have higher volatility on account of their faster growth and smaller market caps, but they have also experienced greater total returns during the rebound as well.

Cloud vs. FAANG Performance (10/2/18 – 12/31/18)

For fund performance click here.

Comparing the performance since the inception of EMCLOUD on October 2, 2018, we observe that while most of the FAANGs had negative returns, the BVP Nasdaq Emerging Cloud Index generated a return of 27.47%.

Cloud vs. FAANG Performance (10/2/18 – 7/31/19)

.png)

The recent downdraft in high-growth stocks on September 9, 2019 has some investors questioning their decision to invest in software companies generally and cloud computing stocks specifically. While we note the rapid shift in sentiment, we still believe in the secular trend in adoption for the industry.

The Growth of Cloud-Based Businesses

Digging deeper, cloud computing’s unique subscription-based business model is one of the reasons we believe these companies could be less prone to market drawdowns compared with the FAANGs.

For cloud services, customers typically pay a recurring subscription fee each month/quarter/year rather than the one-time up-front fee they would pay to purchase a software license. This recurring subscription fee can provide a stable, predictable revenue to sustain a company’s growth amid market volatility. While certain elements of the FAANGs’ businesses may appear similar, we believe these differences can best be shown through a mega-cap tech name that transitioned to the cloud industry.

Company Snapshot

Adobe,2 a cloud computing company that offers digital marketing tools, exemplifies how a subscription-based business model helped a licensed software company achieve explosive growth.

Before 2008, Adobe sold software in physical and boxed discs for customers to install. During 2008 and 2009, Adobe started considering the possibility of transitioning to the cloud for two reasons. First, the difficulty of pushing updates and delivering improved products to customers made Adobe’s tools less attractive to users. Second, the financial crisis in 2008 had a dramatic impact on its cash flow and exposed the limited resiliency of its business.3

Adobe then undertook an expensive and arduous transition to the cloud that concluded in 2013. Since then, Adobe’s revenue has grown at a rate above 25%. Subscription-based revenue also started to account for more of its total revenue, reaching almost 90% in fiscal year 2018.

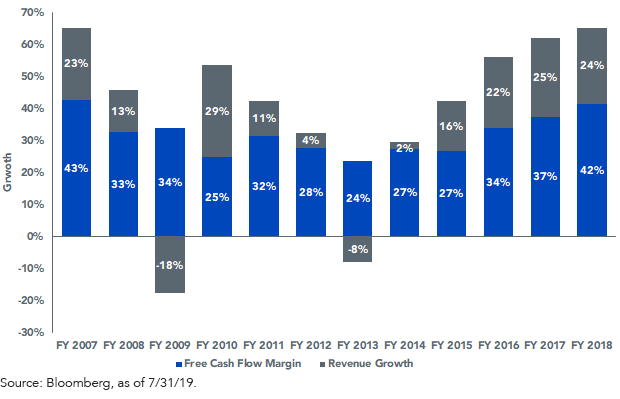

An important rule of thumb for SaaS (software-as-a-service) companies is known as the “40% rule.” This states that if the sum of a company’s free cash flow margin and revenue growth both exceed 40%, the business has a solid balance of growth and profit that enables it to expand efficiently going forward.

From the chart above, we see that before 2013, Adobe’s growth was slowing and its free cash flow margin diminishing. But after 2013, it had a steady growth in revenue and a gradual increase in free cash flow margin. Now, with its established cloud subscription-based business model, Adobe has regained its status as one of the world’s largest technology companies, with a market cap of nearly $140 billion dollars.4

Conclusion

WisdomTree believes cloud computing has disrupted the software sector. While mega-cap tech is facing challenges due to increased government scrutiny, cloud computing could be in the middle innings of its growth curve. For investors seeking better returns but the same growth-oriented, technology-focused exposure in their portfolios, the WisdomTree Cloud Computing Fund (WCLD) could be a compelling alternative.

1WCLD does not hold any FAANG (Facebook, Amazon, Apple, Netflix, Google) stocks

2Adobe Inc. (ticker symbol: ADBE) has a 2.01% weight in the WisdomTree Cloud Computing Fund as of 9/24/19.

3 Sprague, Kara. “Reborn in the Cloud.” McKinsey Digital, 2015

4Source: Bloomberg, as of 9/6/19.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. The Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, on the iInternet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties and the Index may not perform as intended. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

THE INFORMATION SET FORTH IN THE BVP NASDAQ EMERGING CLOUD INDEX IS NOT INTENDED TO BE, AND SHALL NOT BE REGARDED OR CONSTRUED AS, A RECOMMENDATION FOR A TRANSACTION OR INVESTMENT OR FINANCIAL, TAX, INVESTMENT OR OTHER ADVICE OF ANY KIND BY BESSEMER VENTURE PARTNERS. BESSEMER VENTURE PARTNERS DOES NOT PROVIDE INVESTMENT ADVICE TO WISDOM TREE OR THE FUND, IS NOT AN INVESTMENT ADVISER TO THE FUND AND IS NOT RESPONSIBLE FOR THE PERFORMANCE OF THE FUND. THE FUND IS NOT ISSUED, SPONSORED, ENDORSED OR PROMOTED BY BESSEMER VENTURE PARTNERS. BESSEMER VENTURE PARTNERS MAKES NO WARRANTY OR REPRESENTATION REGARDING THE QUALITY, ACCURACY OR COMPLETENESS OF THE BVP NASDAQ EMERGING CLOUD INDEX, INDEX VALUES OR ANY INDEX-RELATED DATA INCLUDED HEREIN, PROVIDED HEREWITH OR DERIVED THEREFROM AND ASSUMES NO LIABILITY IN CONNECTION WITH ITS USE. BESSEMER VENTURE PARTNERS AND/OR POOLED INVESTMENT VEHICLES WHICH IT MANAGES, AND INDIVIDUALS AND ENTITIES AFFILIATED WITH SUCH VEHICLES, MAY PURCHASE, SELL OR HOLD SECURITIES OF ISSUERS THAT ARE CONSTITUENTS OF THE BVP NASDAQ EMERGING CLOUD INDEX FROM TIME TO TIME AND AT ANY TIME, INCLUDING IN ADVANCE OF OR FOLLOWING AN ISSUER BEING ADDED TO OR REMOVED FROM THE BVP NASDAQ EMERGING CLOUD INDEX.

Nasdaq® and the BVP Nasdaq Emerging Cloud Index are registered trademarks and service marks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by WisdomTree. The Fund has not been passed on by the Corporations as to its legality or suitability. The Fund is not issued, endorsed, sold or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE FUND.

Share & Comment

Popular Posts

Categories

Related Links

Jianing Wu joined WisdomTree as a Research Analyst in October 2018. She is responsible for analyzing market trends and helping support WisdomTree’s research efforts. Previously, Jianing completed internships and projects at Geode Capital, Starwint Capital, and Invesco Great Wall Fund Management with a focus in quantitative research. Jianing received her M.S in Finance from the Massachusetts Institute of Technology. She graduated with honors from Boston College with degrees in Mathematics and Philosophy.