WTAI

Artificial Intelligence and Innovation Fund

Published April 30, 2024

Global Head of Research

The Stanford AI Index for 2024 has grown to more than 500 pages! If you have an interest in AI, this is an incredible resource. But as a form of AI for you on this report, we highlight key takeaways for you.

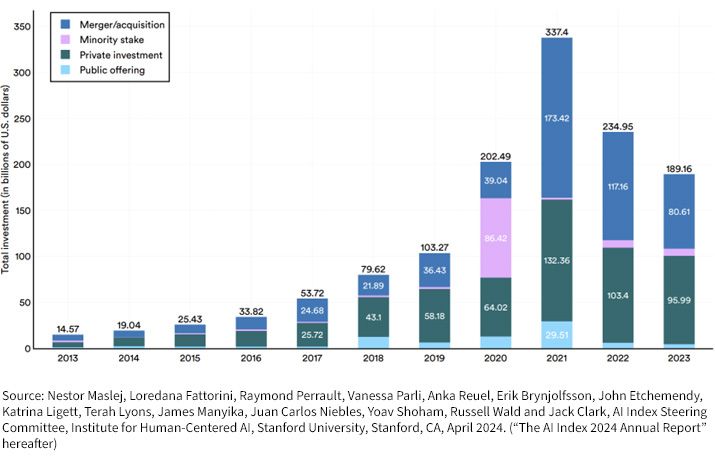

Figure 1 plots global corporate investment in AI back to 2013.

Now, we would be remiss to leave the discussion there, as the headlines that we are seeing on a daily basis would not naturally lead us to predict that AI investment has been going down.

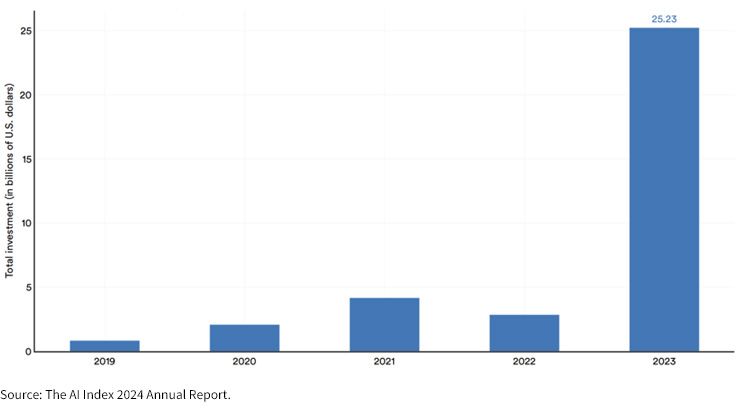

The report evolves each year to best capture new learnings and new details. Generative AI is clearly one of these details, as ChatGPT catapulted this technology into the mainstream. 2023 was the first full year from which we can pull data about different investment activities related to Generative AI. Figure 2:

We believe this trend in generative AI investment is the primary driver behind the headlines we have been seeing for the better part of the last 16 months.

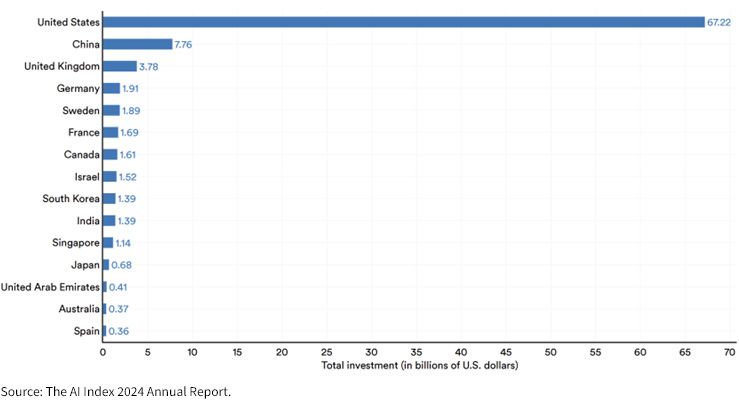

One geopolitical rivalry, time and again, is ever-present in the AI headlines: the U.S. versus China. These two countries have the most prolific spending on AI. China is more influential at the government investment level, whereas the U.S. is more focused on the private side—even if we are seeing things like the CHIPS Act encouraging the semiconductor supply chains to shift more toward the U.S.

Figure 3 shows that no country, at least on a private investment basis, is spending anything close to what the U.S. is spending, which likely means it will be difficult to challenge U.S. leadership in this area.

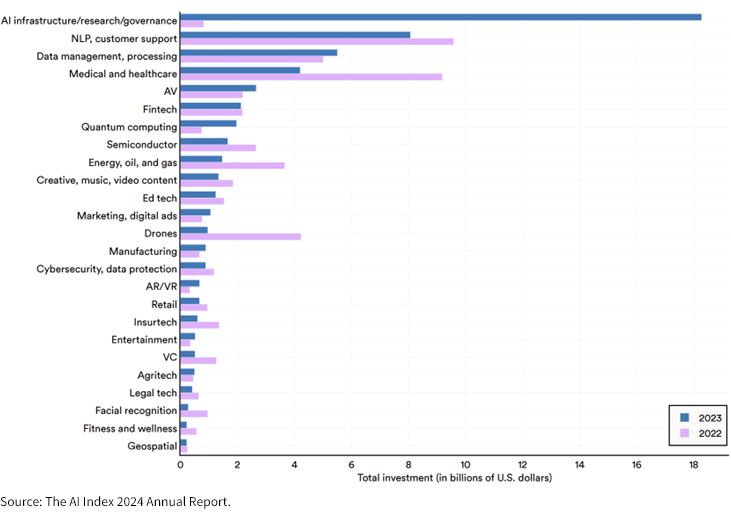

Looking at figure 4, it’s clear the focus category of 2023 was “AI infrastructure/research/governance,” and then there was everything else. This category took $18.3B of private investment, whereas the next biggest focus area, “NLP, customer support,” took $8.1B. Companies building AI applications, like OpenAI, Anthropic and Inflection AI, are included here.

Quantum computing also had a rather significant increase in investment from 2022 to 2023.

Drones, on the other hand, saw a rather significant decrease.

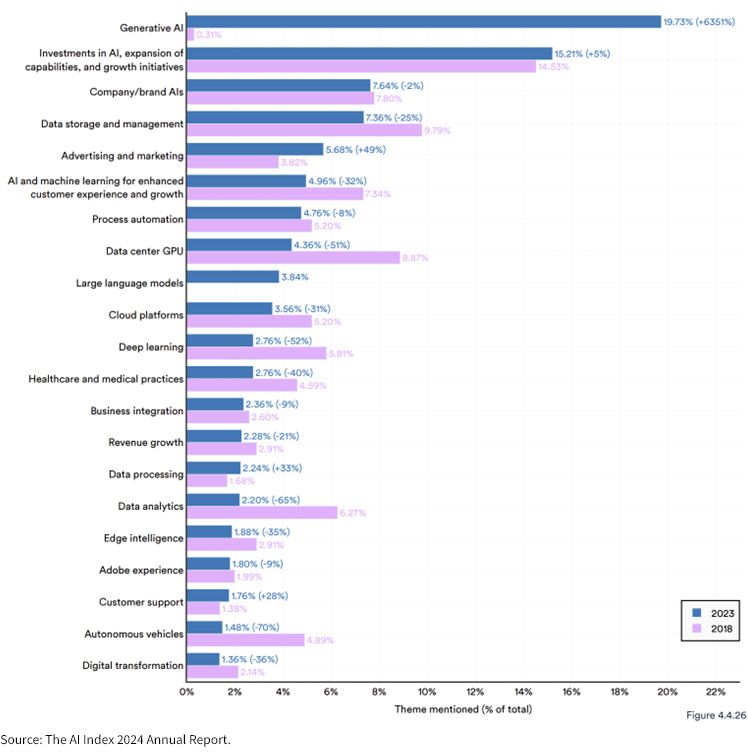

The quarterly earnings calls in which U.S. publicly listed companies engage represent a dance, and the most important takeaway from every call is learning what the C-suite of the specified firm is trying to sell. Figure 5 shows the themes of AI mentions in earnings calls, comparing 2018 to 2023.

This is, in our view, the true impact of ChatGPT. This application made the potential of generative AI so exciting that every public company felt it must pay attention and promote actions. Even if the “Attention is all you need”1 paper defining generative pre-trained transformers as an architecture was published in 2017, prior to ChatGPT, corporate America was not really paying close attention.

The mentions on Fortune 500 earnings calls with generative AI as a theme increased more than 6,300% from 2018 to 2023.

WisdomTree has focused on the AI megatrend in a few different ways:

Both of these Funds can provide exposure to this theme, depending on whether you want more diversified ecosystem exposure and the innovative applications or the mega-caps that are currently benefiting the most.

1 Source: Vaswani et al., “Attention is all you need,” arXiv, 2017.

For current Fund holdings, please click the respective ticker: WTAI, QGRW. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTAI: The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended.

QGRW: Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified; as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.