HEDJ

Europe Hedged Equity Fund

Published April 1, 2024

The buzz around artificial intelligence (AI), in lockstep with the strong earnings announcements, has lent a strong impetus to equity markets, and the eurozone in particular. Eurozone equities are trading at record highs, with the EuroStoxx 600 Index hitting the 496 level.1

Can eurozone equities sustain these gains? The macroeconomic data in the eurozone hasn’t yet convincingly turned around. But many of the leading companies in Europe sell all over the world—from the U.S. to China—and that global backdrop has been supportive.

There is also the potential that the European Central Bank (ECB) pivots before the Federal Reserve (Fed) on monetary policy. Subsequent rate cuts could relieve strain on the eurozone economy, setting the stage for a more constructive equity market backdrop.

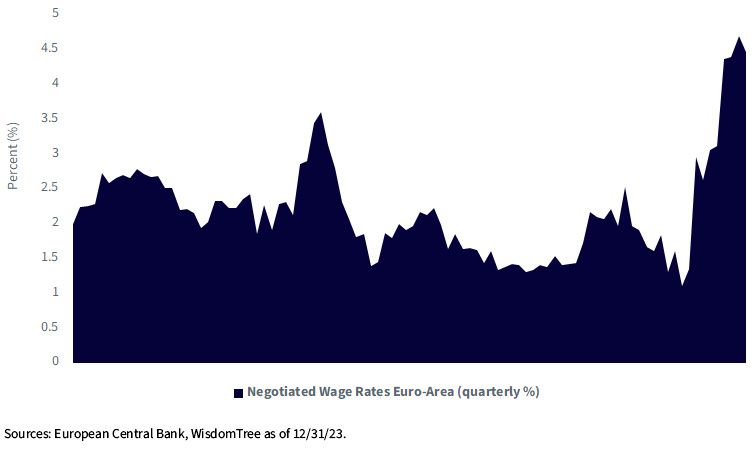

What makes us most convinced about the ECB pivoting sooner than the Fed is the downward pressure from wages. Wage growth remains an important bottleneck to further rate cuts by the ECB. Currently, the eurozone is facing a bigger overshoot in wage growth than the U.S.

While the unemployment rate has been stable at historically low levels over the past year, the job vacancy rate has fallen sharply from a peak of 3.2% in Q2 2022 to 2.7% as of Q4 2023. From this, we can infer that around half of the increase in labor market tightness has already been unwound. With the economy expected to stay range-bound in the near term, the labor market is expected to soften further over the coming months.

The quarterly negotiated wages are one of the few “official” ECB wage statistics that fell from their record high in Q3 2023. For the ECB to wait until wage growth has fully fallen back runs the risk of rates staying higher for longer, risking a recession.

ECB members led by President Christine Lagarde, Isabel Schnabel and Joachim Nagel tried to talk down rate cut expectations at the meeting of European finance ministers and central bank governors in Ghent. The ECB seems to be faltering in its success in talking down expectations, largely because, unlike in the U.S., where economic data does not point to the need for imminent rate cuts, in the eurozone, it does.

There is no denying that the Magnificent 7 effect has clearly transmitted to Europe, with five stocks driving the European equity rally, led by ASML (+39%), Novo Nordisk (+34%), SAP (+16%), LVMH (+16%) and Schneider (+8%), year-to-date (YTD).2

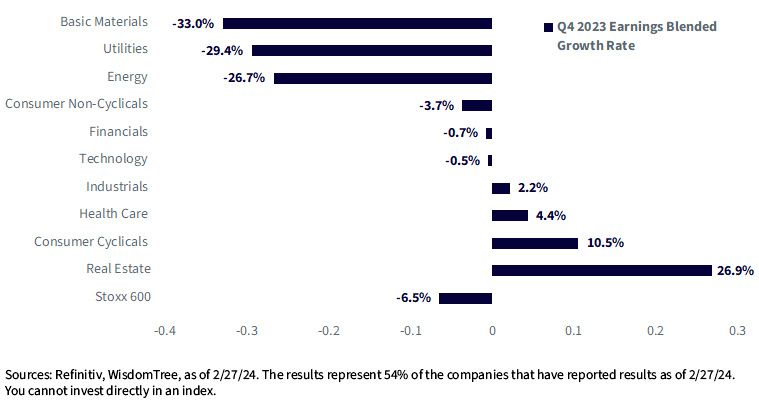

Unlike the U.S., the leading eurozone stocks YTD are diversified across sectors, including Information Technology, Consumer Discretionary and Industrials. A reflection on the Q4 2023 earnings results highlights Consumer Cyclicals, Health Care and Industrials leading the scoreboard with the highest earnings growth rate (among the 54% of the companies that have reported results), while Energy, Utilities and Materials led to the biggest drag on earnings results. Amidst the backdrop of the ECB easing rates and a weaker macroeconomic backdrop, the euro is likely to weaken further against the U.S. dollar, lending a competitive edge to its exporters.

Spain outperformed the Big 4 European countries in 2023 and remains the most constructive case for 2024. In 2023, the impact of higher rates dented investment growth; however, consumption remained strong fundamentally, driven by the resilience of the labor market. The Spanish labor market performed well. The composition of Spain’s labor market has shifted from temporary employment to open-ended contracts. The tilt toward open-ended contracts tends to encourage more consumption, owing to greater job security.

However, the recovery has not been even across sectors—the Construction, Real Estate, Information Technology and Communication Services sectors are lagging. There is a need for the Spanish economy to improve productivity via rebuilding capex, and Spain is well-positioned to do so. Spain suffered the highest repercussions from the tightening of monetary policy, and in lockstep, the rate relief expected by the ECB should be relatively more impactful for Spain’s economy. Spain is also the largest recipient of recovery funds in Europe. It has been effective in implementing the $37 billion in funding.3 In 2024, it is expected to receive more than 2% of GDP in disbursements, most of which will be in support of capital expenditure. Spain is well-positioned to leverage the supportive macro landscape.

The WisdomTree Europe Hedged Equity ETF (HEDJ) provides investors with exposure to dividend-paying eurozone companies that derive at least 50% of their revenues outside of the eurozone while hedging exposure to the euro.

By virtue of including dividend-paying eurozone exporters, HEDJ attributes a higher weighting to sectors that exhibit stronger earnings growth, such as Consumer Discretionary, Industrials, Financials and Information Technology, while it has a lower weighting to sectors with weaker earnings growth, like Energy, Utilities and Materials.

The connection between stronger earnings and performance is evident from HEDJ's performance in 2024. While the EuroStoxx 600 Index is up 3.3% and the MSCI Europe Index is up 4.8%, the WisdomTree Europe Hedged Equity ETF (HEDJ) is up 8.1%.4

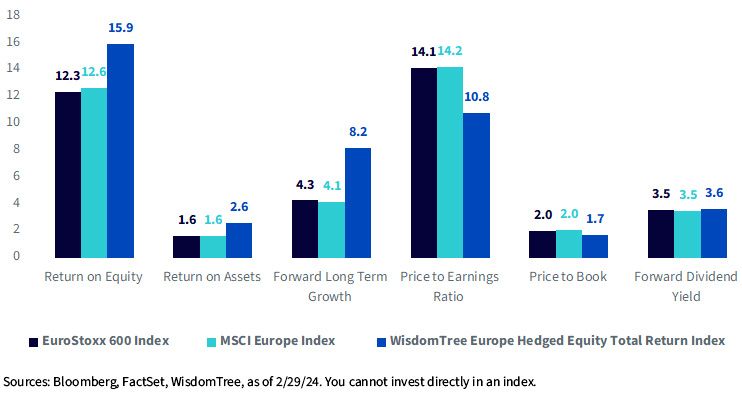

We know that Europe is trading at attractive valuations compared to global equity markets. The WisdomTree Europe Hedged Equity Index compares favorably to the benchmarks when looking at fundamental metrics.

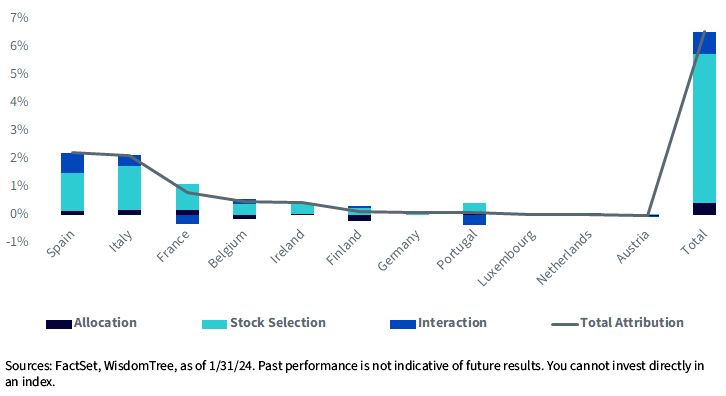

Over the past year, the WisdomTree Europe Hedged Equity Index outperformed the MSCI EMU Local Currency Index by 6.55%. The attribution across geographies highlights the higher allocation to Spain, which resulted in a positive overall contribution of 2.24%, benefitting the overall performance.

1 Bloomberg, as of 2/23/24.

2 Bloomberg, from 12/31/23 to 2/26/24 (in USD terms).

3 European Commission, https://ec.europa.eu/economy_finance/recovery-and-resilience-scoreboard/disbursements.html?lang=en.

4 Bloomberg performance from 12/31/23 to 2/29/24. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the Fund prospectus, click here.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Europe Hedged Equity Fund

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.