Carry Opportunities Abound with Current Coupon…but Let’s Not Get Carried Away.

Published December 11, 2023

Behnood Noei, CFA

Director, Fixed Income

Andrew Okrongly, CFA

Director, Model Portfolios

Executive Summary

- Even after the recent rally in interest rates, agency mortgage-backed securities (agency MBS) still appear attractive from both a fundamental and technical basis and offer a compelling level of yield/income compared to other fixed income asset classes

- A segment of this market that has recently garnered attention is newly issued MBS, or current coupon mortgages

- While current coupon mortgages can offer a higher level of income than other cohorts of the market, investors should be aware of the inherent risks with these bonds, namely prepayment and liquidity risks

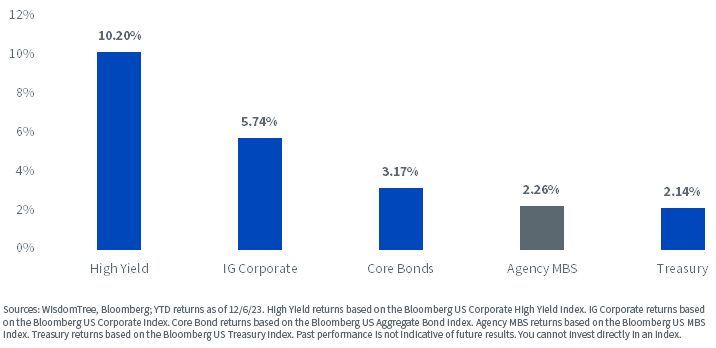

As discussed in previous posts, agency mortgage-backed securities (agency MBS) have lagged other fixed income asset classes in performance this year. This underperformance has been driven by several factors, including rising interest rates, elevated interest rate volatility and concerns around supply/demand imbalances.

YTD Returns across Fixed Income Sectors as of 12/6/23

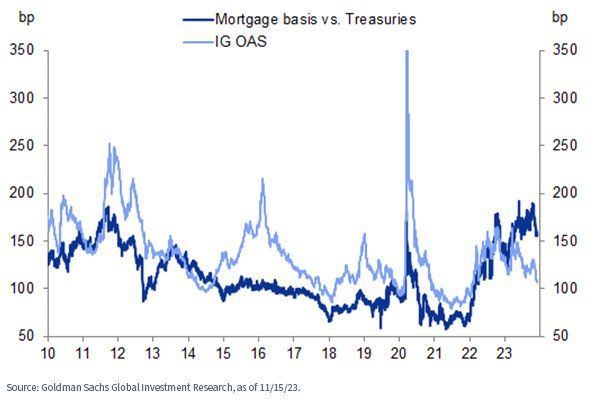

Even after the recent decline in interest rates, the spread of agency MBS relative to Treasury bonds remains at multi-year highs. With attractive valuations and a potentially improving fundamental and technical environment, we believe that long-term investors can benefit by allocating to the asset class.

Mortgage Basis (Current Coupon Mortgage Rate – 5-/10-Year Treasury Rate) and IG OAS

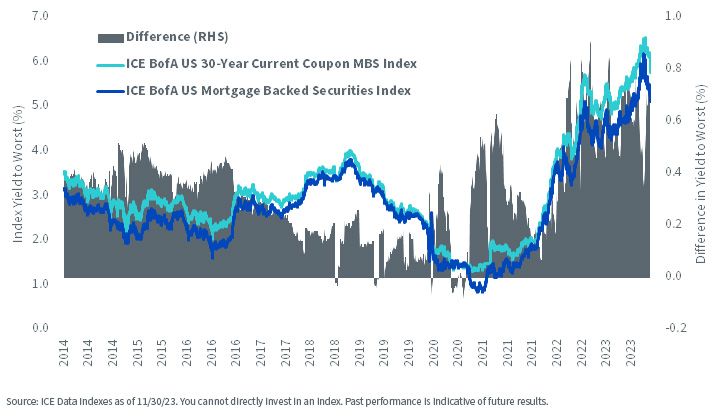

A segment of this market that has garnered attention this year is recently issued MBS, or current coupon mortgages. Simply defined, a current coupon bond is one selling at a price at or close to its par value. These bonds usually tend to be the ones recently issued.

Broad agency MBS indexes consist of mortgages with varying coupons and vintages, or the year each MBS was issued. Current coupon mortgages tend to offer a higher yield versus the broader index. As a matter of fact, in the past 10 years, there have only been a few days when the yield on current coupon mortgages has been lower than the broader index.

Difference in Yield to Worst: Current Coupon MBS and Broad MBS Index

For definitions of indexes in the graph above, please visit the glossary.

As can be seen from the chart above, ever since the Fed embarked on its historical quantitative tightening process in 2022, the yield gap between the current coupon and broader index has widened significantly. Investors have noticed, as they can now get a higher level of yield/income from a product with the same credit risk as the broader index.

However, most savvy market participants know that no good opportunity comes without risks. Hence, it is prudent for investors to understand the inherent risks in current coupon mortgages, namely elevated prepayment and liquidity risks.

Prepayment Risk

Like most mortgages, current coupon mortgages come with prepayment risk. From an investor’s standpoint, this is the risk that you receive your principal back earlier than planned and may need to reinvest that principal at lower prevailing interest rates.

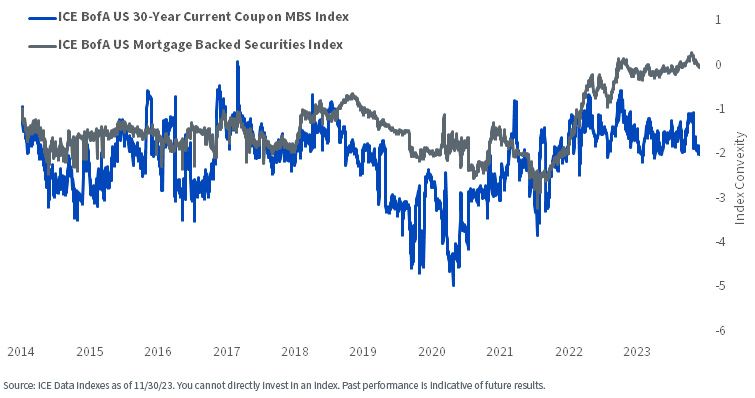

The level of prepayment risk can be quantified by a fixed income risk metric called convexity. Convexity is the curvature in the relationship between bond prices and interest rates. It reflects the rate at which the duration of a bond changes as interest rates change. In mathematical terms, convexity is the second derivative of changes in a bond price compared to changes in the interest rate.

Agency MBS tend to have negative convexity at most times. This is because mortgage borrowers have the option to prepay their outstanding balance when rates fall (refinance their mortgage at a lower rate). As a result, when rates fall, MBS investors won’t enjoy the same price appreciation that investors in a similar-duration Treasury bond would.

However, as can be seen from the chart below, the broader MBS index currently has slightly positive convexity, something that hasn’t happened in years.

Difference in Index Convexity: Current Coupon MBS and Broad MBS Index

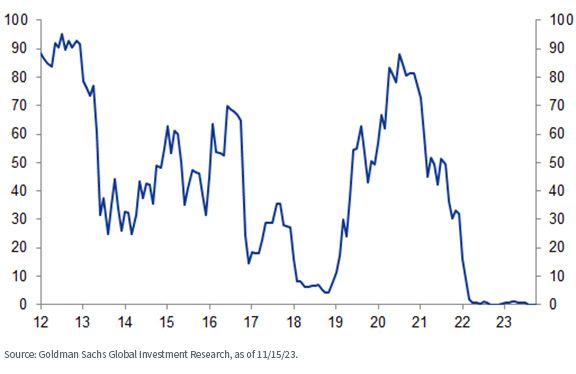

This positive convexity for the broader agency MBS index is driven by mortgage borrowers having little to no incentive to refinance their mortgages. Putting it in more technical terms, the prepayment option sold to borrowers by investors is out-of-money. As can be seen from the chart below, the share of borrowers with a 50+ basis points (bps) rate incentive to refinance their mortgages is near zero.

Percentage of Borrowers with a 50+ bps Refinance Incentive (%)

On the other hand, this can’t be said for borrowers who have recently taken out mortgages at today’s high interest rates, which are the mortgages predominantly backing current coupon MBS.

This segment of the agency MBS market is still negatively convex. As a result, if interest rates were to decline in the near future, current coupon investors would be more likely to suffer the prepayment/reinvestment risk associated with negative convexity and might end up underperforming the broader agency MBS index as a result.

Liquidity Risk

The other important risk to consider with current coupon mortgages is the liquidity of these bonds if interest rates decline and borrowers refinance their debt at a lower rate.

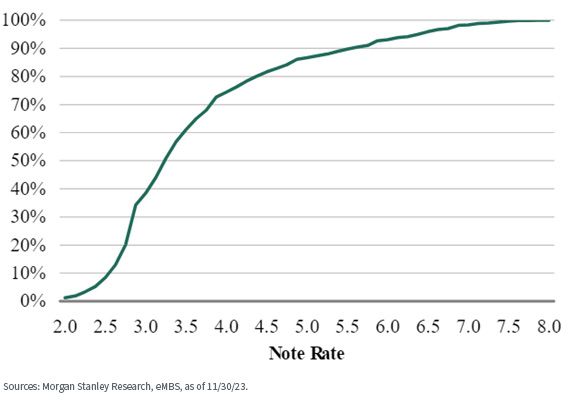

More than 98% of the conventional fixed-rate agency MBS universe has a mortgage rate below 7%. In other words, current coupon mortgages make up only around 2% of the universe. And, as explained above, these mortgages are most susceptible to prepayment risk. Falling interest rates could, therefore, leave an even smaller number of these current coupon mortgages outstanding, potentially creating liquidity challenges that could further impact market pricing.

Percentage of Conventional Borrowers below a Given Rate

Conclusion

Current coupon agency MBS offers an attractive level of yield compared to other segments of the MBS market and even compared to other highly rated AAA corporates. However, they also could experience elevated prepayment and liquidity risks in a falling interest rate environment.

Prudent investors need to be aware of these risks before getting carried away by the allure of higher yields offered by this segment of the market.

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributors

Behnood Noei, CFA

Director, Fixed Income

Behnood Noei serves as Director of Fixed Income at WisdomTree Asset Management, where he develops the firm’s suite of fixed income and currency exchange-traded funds and enhances existing investment processes. Behnood has 11 years investment experience in portfolio management and quantitative research. Prior to joining WisdomTree in 2022, Behnood was a portfolio manager and developer of some of the fixed income ETFs at J.P.Morgan Asset Management, where he was directly responsible for managing more than 7 Fixed Income ETFs and multiple SMAs with more than $13Billion in assets. He graduated from The Ohio State University with Master of Science degree in Finance and is a CFA charter holder.

Andrew Okrongly, CFA

Director, Model Portfolios

Andrew Okrongly joined WisdomTree in 2022 as a Director on the Model Portfolios Team. He is responsible for the design and ongoing management of model portfolios and custom solutions for portfolio managers and advisors. Andrew is also a member of the Model Portfolio Investment Committee. Prior to joining WisdomTree, Andrew was a Director on the Outsourced Chief Investment Officer (OCIO) team at Commonfund, where he was responsible for macro-economic analysis and advising institutional clients on strategic and tactical asset allocation. Andrew began his career at BlackRock where he held a variety of fixed income and multi-asset investment roles. Andrew received a BBA degree from the University of Michigan and is a holder of the Chartered Financial Analyst designation.