EM Small-Caps: Attractive Valuations and Dividends

Published September 26, 2023

Associate Director, Research Content

U.S. Head of Research

In the pursuit of returns, investors are constantly asking what they potentially missed. Narrow market leadership in U.S. large caps all but guaranteed outperformance relative to small caps. In the EAFE (Europe, Australasia and the Far East) region, a similar story emerges, but with slightly less concentration. Curiously, in emerging markets the exact opposite is true. Despite wide-spread concern about the underlying fundamentals of emerging markets and China, small-cap companies are handily outperforming large caps.

In this piece, we highlight drivers of relative performance. For investors focused on valuations, emerging markets small-cap dividend payers appear worthy of a second look.

The WisdomTree Emerging Markets SmallCap Dividend Fund (DGS), which seeks to track the price and yield performance, before fees and expenses, of the WisdomTree Emerging Markets SmallCap Dividend Index (WTEMSC), was launched in 2007 and provides exposure to small-cap dividend-paying companies in emerging markets.

DGS is value-oriented and differs from traditional market cap-weighted indexes, as outlined below:

- Screen to only include profitable dividend-paying companies from the eligible universe

- Remove companies most at risk of cutting dividends based on quantitative risk screens

- Take a dividend-weighted approach based on each company’s Dividend Stream®

Differentiated exposure

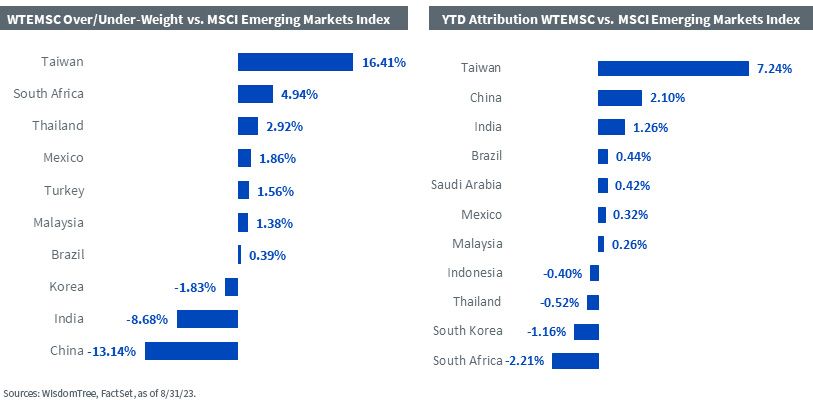

In recent years, investing in emerging markets meant taking a substantial allocation in Chinese companies. Even though the proportion of the MSCI Emerging Markets Index allocated to China has fallen from its peak of 43% in October 2020, it still constitutes close to a third of the index.

DGS has significantly lower exposure to China than traditional large caps—which have a lot of tech companies that are low dividend payers.

As of August 31, 2023, the underlying WisdomTree Index had 17% allocated to China and over 31% to Taiwan. The over-weight exposure to Taiwan contributed over 7% to performance while an under-weight exposure to China and India added 2.10% and 1.26%, for a total outperformance of 7.76% relative to the MSCI Emerging Markets Index.

Higher allocation to ex-state-owned enterprises and lower allocation to state-owned enterprises also contributed to year-to-date performance.

Valuations

Current valuations make a compelling case for investing in emerging markets, especially relative to the U.S. market, which had high multiple expansion over the past few years.

DGS currently offers single-digit price-to-earnings ratios on trailing as well as forward basis. In contrast, valuations for the S&P 500 Index are currently over 20 and above the long-term average.

Price-to-Earnings

Estimated Price-to-Earnings

Quality Tilt

One of the requirements for inclusion in the WisdomTree Emerging Markets SmallCap Dividend Index is profitability, which introduces a quality bias. Less than 3% of the Index is currently invested in unprofitable companies, compared to 5% for the MSCI Emerging Markets Index and close to 11% for the MSCI Emerging Markets SmallCap Index.

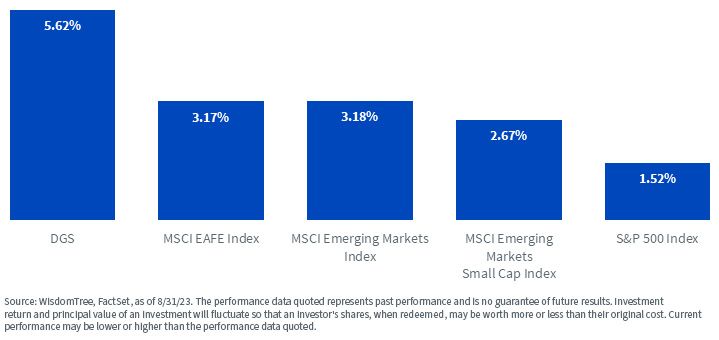

In addition to attractive valuations and quality tilt, emerging markets small-cap dividend payers have historically offered considerably higher income than core U.S. and broad international developed equities.

Dividend Yields

For the 30 Day SEC Yield, SEC Standardized Return, and the most recent month-end performance click here.

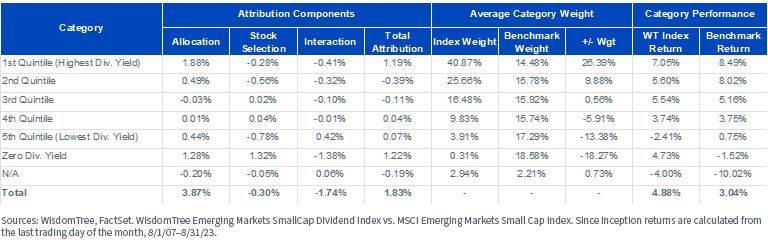

Investors may be surprised to learn how important of a factor dividend payments were for the small-cap segment in emerging markets. First, unlike the U.S., where less than 50% of the Russell 2000 paid a dividend, among emerging markets small caps, more than 87% distributed dividends. Moreover, our attribution tool shows how important a driver this factor was for emerging markets.

Since Inception Dividend Yield Attribution

Companies that don’t pay dividends had returns of -1.52%, more than 4.56% behind the MSCI Emerging Markets Small Cap Index generally.

While the highest dividend yield segment in the WisdomTree Index returned 7.05%, more than 4.01% higher than the MSCI Emerging Markets Small Cap Index.

Since inception, the underlying index for DGS outperformed the MSCI Emerging Markets Small Cap Index by 1.83%. A higher allocation to the top dividend-yielding segment added 1.19%, while a reduced allocation to non-dividend-paying stocks contributed an additional 1.22% to the overall performance.

Focusing on dividend-paying companies was a key value add to the small-cap strategy in generating excess returns since inception. Paying dividends served not only as a valuation factor but also as a quality measure since companies needed profitability, earnings and financial strength to maintain and distribute dividends.

Conclusion

For investors who believe in the long-run potential of emerging markets, focusing on dividend-paying small caps could be a source of positive total returns as well as income.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing on a single sector and/or smaller companies generally experience greater price volatility. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributors

Associate Director, Research Content

Lonnie S. Jacobs joined WisdomTree in August 2006 as Senior Index Analyst overseeing creation, maintenance and reconstitution of the firm’s passive indexes and actively managed ETFs. In her current role as Associate Director, Research Content, she is focused on supporting the research pipeline and analyzing the impact of global markets on WisdomTree strategies. Lonnie has B.A. in Economics and M.S. in Information Systems.

U.S. Head of Research

Bradley Krom joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.