‘Big Tech’ Won the First Half of 2023…What about the Second?

Published August 1, 2023

Global Head of Research

A small subset of mega-cap companies—many of them associated with generative artificial intelligence (AI)—have driven most of the U.S. equity market’s positive returns in 2023.

So what?

Now, investors are trying to decide if the growth setback in 2022 is indicative of a longer-term shift toward value investing over the coming years—or even decade—or was just a temporary speed bump for the large tech giants.

One interesting signal that we have seen is a large variation in returns between the Nasdaq 100 Index and the S&P 500 Index. The Nasdaq conforms largely to what people think of as ‘tech,’ and it still includes companies like Amazon.com, Tesla, Alphabet and Meta—companies that technically now find themselves in the Consumer Discretionary and Communication Services sectors.

Tech, Growth or Quality Growth?

Frequently, investors don’t simply stop after looking at the S&P 500 and Nasdaq 100 indexes—they might also consider growth indexes, like the Russell 1000 or S&P 500 Growth. Intuitively, before looking under the hood, many assume that the results should be similar to those of the Nasdaq 100.

At WisdomTree, we denote a special approach that we term ‘Quality Growth,’ where many tech companies do in fact gain inclusion if they are able to demonstrate significant return on equity and return on asset statistics. For WisdomTree—it’s not about ‘tech’ or ‘not tech’ or ‘growth’ or ‘value’—it is a simple question of whether or not the companies prove they are the highest quality through their fundamentals. As we see in figure 1, where we start the analysis roughly at the release of ChatGPT in November 2022:

- The WisdomTree U.S. Quality Growth Index was strong over the period, delivering returns very similar to those of the Nasdaq 100 Index.

- The Russell 1000 Growth Index was significantly behind both the WisdomTree U.S. Quality Growth Index and the Nasdaq 100.

- It was also clear that there was a huge difference between choosing the Russell variety of growth and the S&P variety of growth, shown through the significant lag in cumulative returns for the S&P 500 Growth Index relative to those of the Russell 1000 Growth Index.

Figure 1: H1 2023 was all about quality growth companies, yet returns were quite different

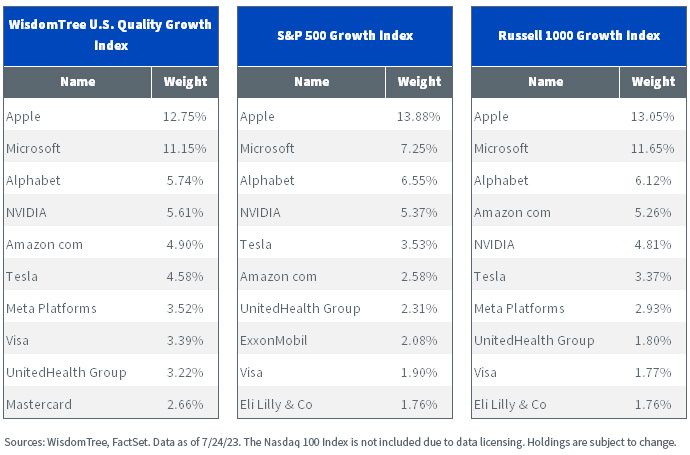

Who Are the Quality Growth Companies?

In figure 2, we wanted to make crystal clear what we mean by the quintessential quality growth companies by looking at the WisdomTree U.S. Quality Growth Index’s top 10 exposures. You learn a lot by looking at this compared to those of the other benchmarks.

- Having Apple and Microsoft in the top two positions was not unusual, and we see that is the case across all three indexes. However, the S&P 500 Growth Index was the outlier with a figure closer to 7% allocated to Microsoft, whereas the allocations of both the WisdomTree U.S. Quality Growth Index and Russell 1000 Growth were closer to the 11% range. Out of the gate, less weight to Microsoft for the first half of 2023 was not the route to the strongest possible performance, but we know that this can ebb and flow over time.

- Within the S&P 500 Growth, we see the Exxon Mobil position. A big energy company, at least historically, tends to be more of a value type of position rather than a growth position, but after a strong 2022, Exxon Mobil exhibited strong share price momentum and ended up being included in the S&P 500 Growth. The position stands out, not because we know how Exxon Mobil will perform, but because it’s clearly not in the top 10 for the other two indexes.

- Meta Platforms was a strong performer during the first half of 2022. It was not in the top 10 of the S&P 500 Growth, as it had lower momentum from 2022. It was included in both the WisdomTree U.S. Quality Growth Index and the Russell 1000 Growth. Intuitively, people do think of Meta as more a ‘growth’ type of company, even if, like Exxon Mobil, you can never know ahead of time when Meta will be poised for outperformance.

Figure 2: Top 10 positions in select benchmark indexes

Conclusion: Will AI Continue to Fuel this Big Company Rally?

As we go through the final days of July and coming into early August 2023, Microsoft pre-empted this so-called earnings week by making a big announcement in the prior week, letting the world know that they would be pricing their generative AI Copilot software at $30 per month, per user, for commercial customers.1 This was an important announcement, because while we know that generative AI is important and that it was central to the rally in equities in the first half of 2023, we don’t know for sure if or how it will allow companies to drive revenues and ultimately generate earnings. Of all the largest firms, at least so far, Microsoft is doing the best job of tying generative AI’s narrative and potential to concrete, revenue-driving initiatives. Later in the reporting cycle, it will be notable to see if Nvidia can make good on or possibly even beat the $11 billion expected figure that they put on the board back in May 2023.

After all of the Big Tech companies report their quarterly results, we believe we might get a sense as to whether the strong share price performance of these companies is more or less likely to continue.

For those seeking exposure to the growth companies that have proven they belong at the top of the quality spectrum, we believe the WisdomTree U.S. Quality Growth Fund (QGRW) is well positioned to keep the focus directly on these firms.

1 Source: Richard Waters, “Microsoft to Charge $30 per Month for Generative AI Features,” Financial Times 7/18/23.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified and, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.