Some Perspective on Banking Woes: Two Months Later

Published May 17, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

It’s been roughly two months now operating in a post-Silicon Valley Bank (SVB) world, and the markets are still feeling its impact. While the stock and bond markets continue to wrestle with the fallout from both an economic and regional banking concern perspective, there is a very important arena where developments have seemingly flown under the radar of late (which is a good thing): the funding markets.

When banking-related issues “hit the tape,” one of the first locations investors should turn to see if there are any negative effects is the funding markets. Indeed, throughout modern financial history, it is this arena where dislocations can “snowball” and turn a potentially isolated occurrence into a systemic event. Certainly, the 2007–2008 great financial crisis underscored that point, but we’ve also witnessed other episodes where pressures were evident, such as the COVID-19 lockdown.

The Federal Reserve (Fed) is well aware of these scenarios as well. In fact, the Fed acted rather swiftly this time around and implemented the Bank Term Funding Program (BTFP) in response to the first wave of adverse news that came out from Silicon Valley Bank (SVB) and Signature Bank in early March. BTFP was created specifically to offer “funding available to eligible depository institutions.” What can be considered one of the key aspects of this program is that the pledged collateral, such as Treasuries, “will be valued at par,” not only making funding available if needed but also “eliminating an institution’s need to quickly sell those securities in times of stress,” which was one of the major catalysts behind the regional banking turmoil in the U.S.

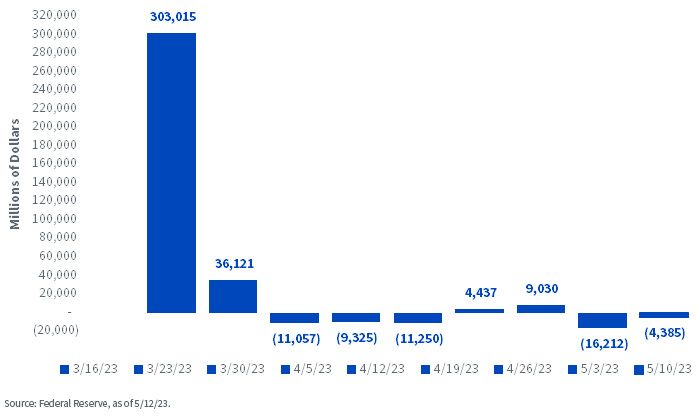

Fed Balance Sheet: The Total Change in Lending Facilities

When looking at the Fed’s key available lending facilities, there are three components to examine: primary credit at the discount window, BTFP and other credit extensions (FDIC-related loans). As you can see, banks utilized these facilities in a visible way in the immediate wake of the turmoil, but since mid-March, total usage has dropped off considerably. To provide some perspective, after hitting a peak increase of $303.0 billion on March 16, the total amount has declined in five out of the last seven weeks, falling by $4.4 billion as of May 10. The bottom-line message is that the Fed’s facilities acted as they were intended and arguably prevented any further calamity up to this point.

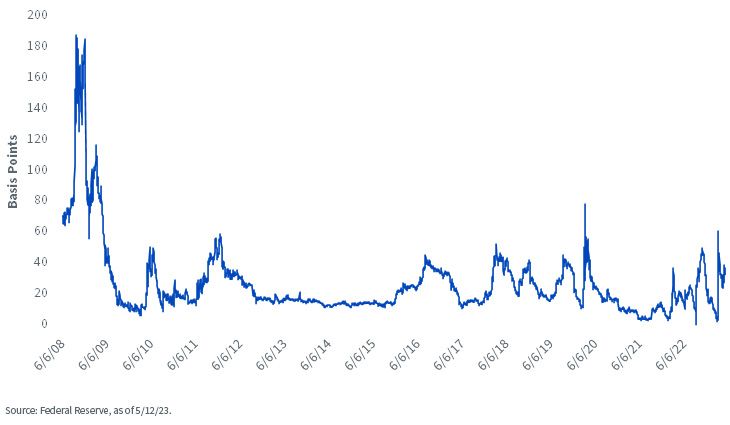

U.S. Interest Rate Swaps

This point has been buttressed by what has also transpired in the aforementioned funding market. The U.S. interest rate swap market (an agreement between counterparties to exchange fixed versus floating cash flows) provides a clear look at developments in this arena. For the record, the wider the spread, as measured in basis points (bps), theoretically, the more pressure, or dislocations, there is for institutions to find funding. As you can see, there was a spike in funding pressures around mid-March, but conditions have steadily improved since then. While the spread has not returned to its pre-SVB reading, it has remained relatively stable (+35 bps) and is well within recent trading ranges and considerably below the high watermarks of the financial crisis (+188 bps) and COVID-19 lockdown (+78 bps).

Conclusion

With regional bank concerns still making headlines, it remains a prudent idea to continue monitoring developments. However, if the funding markets continue to operate as outlined here, the markets, and perhaps more importantly, the Fed, can focus more on the potential economic ramifications that may lie ahead. More on this in a later blog post…

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.