The WisdomTree Portfolio Review, Part Three: Collaboration Models

This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

We are now on the third and final part of our “mini-series” of blog posts reviewing the Q1 2023 performances of our Model Portfolios. Part one focused on our strategic models, part two focused on our outcome-focused models and in this final entry into the series, we focus on our collaboration models.

First, let’s define terms. We use the term “collaboration” as it is defined—“the action of working with someone to produce or create something.” We recognize that other people and firms have smart ideas and/or good products, and we actively seek to find partners willing to collaborate with us to deliver outstanding solutions.

An active part of our models business is to collaborate with RIAs, wirehouses, IBDs and other platforms to construct and manage customized models that fit those firms’ specific investment mandates. As they are customized and sometimes proprietary, we cannot show those models on our Model Adoption Center, but they represent at least 50% of the total AUM in models that we manage, and we welcome that business.

A growing part of that is our Portfolio and Growth Solutions platform. On this platform, we not only help build models with advisors, but we also then take on the implementation, trading and ongoing rebalancing (including tax management, if desired) of those portfolios on the advisor’s behalf, freeing them up to spend more time on revenue-generating activities.

But we do have three publicly available collaboration models we can discuss—the Select models that we manage in collaboration with PIMCO, the U.S. Growth series, which we developed in coordination with a large RIA and, of course, our flagship collaboration with Professor Jeremy Siegel in the Siegel-WisdomTree Global Equity and Longevity models.

Let’s take a look.

Siegel-WisdomTree Models

We have written extensively about these models, most recently in early March when we reviewed our overall 2022 performances. So here we just provide a quick reminder of what these models are all about and why we collaborate so closely with Professor Siegel on them.

The investment thesis was to challenge the ability of the traditional 60/40 portfolio to deliver on what we believe are the four primary objectives of most investors:

- Maintain or enhance current lifestyle by optimizing current income.

- Minimize “longevity risk,” or the risk of outliving your portfolio.

- Maximize the potential for leaving a legacy; and

- Minimize fees and taxes along the way.

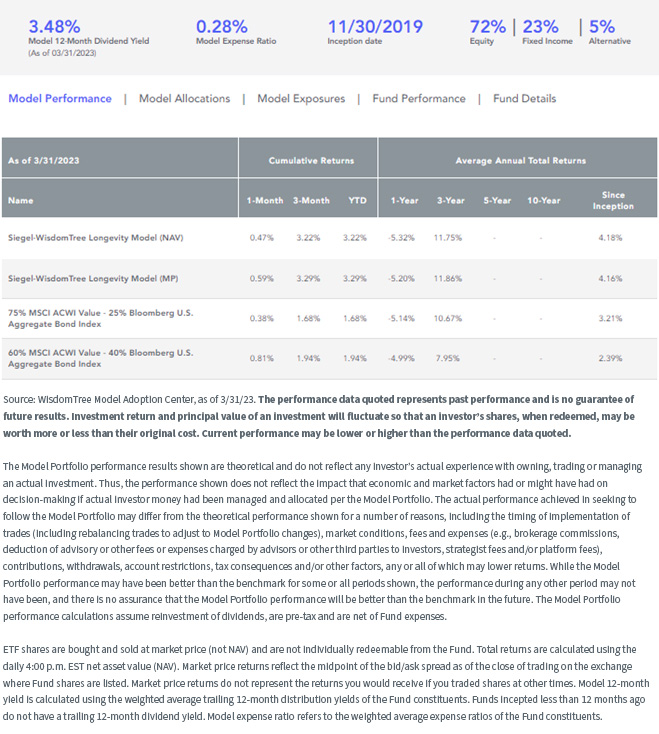

The Siegel-WisdomTree Longevity model attempts to solve for exactly these issues. Its strategic allocations are 75% stocks and 25% bonds (though we currently have ~5% allocated to managed futures for diversification purposes, with the equity allocation focused on value-oriented and dividend-paying strategies.

The result is a portfolio that, in comparison to a traditional 60/40: (1) generates enhanced current income; (2) has an improved longevity profile because of the heavier allocation to stocks; and (3) has only a slightly higher standard deviation (i.e., short-term volatility profile) than the traditional 60/40. Because of its “tilts” toward value and dividend stocks, it tends to have a lower beta profile, so the standard deviation is close to the 60/40 portfolio despite its heavier allocation to equities.

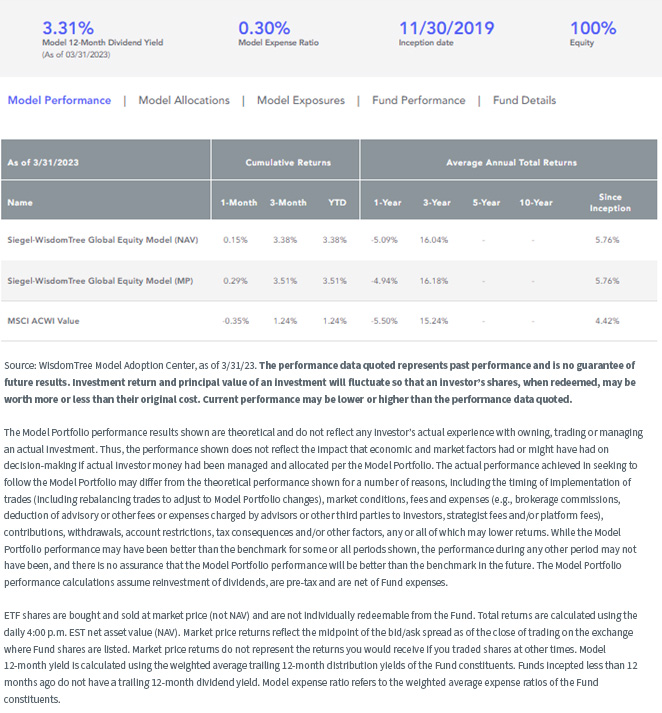

The Siegel-WisdomTree Global Equity portfolio is constructed in a similar fashion but allows advisors to manage their own fixed income allocations if they so desire.

Q1 saw these models outperform their benchmarks, where we use the MSCI ACWI Value Index as the equity benchmark and the Bloomberg U.S. Aggregate Index for fixed income. While value dramatically underperformed growth in Q1 (a distinct headwind for our inherent tilts), our relative performances were carried by strong results in our large-cap EAFE and managed futures allocations.

We also overlay a distinct quality filter within these portfolios, and this provided additional marginal relative performance. All that said, we don’t believe the “re-rotation” back toward growth stocks in Q1 is a long-term trend, and we remain comfortable with our overall positioning for the medium and long term.

Considering heightened uncertainty regarding the economy, corporate earnings and the banking system, however, we did take moves at our April Model Portfolio Investment Committee meeting to reduce our active bets versus our benchmarks and to lower our exposure to financials and banks.

Since inception more than three years ago, these portfolios have comfortably outperformed their benchmarks. In the case of the longevity model, this includes both a 75/25 benchmark and the more traditional 60/40 benchmark.

Siegel-WisdomTree Longevity Model

For the most recent month-end performance and current 30-Day Sec Standardized Yield, please click here.

Siegel-WisdomTree Global Equity Model

For the most recent month-end performance and current 30-Day Sec Standardized Yield, please click here.

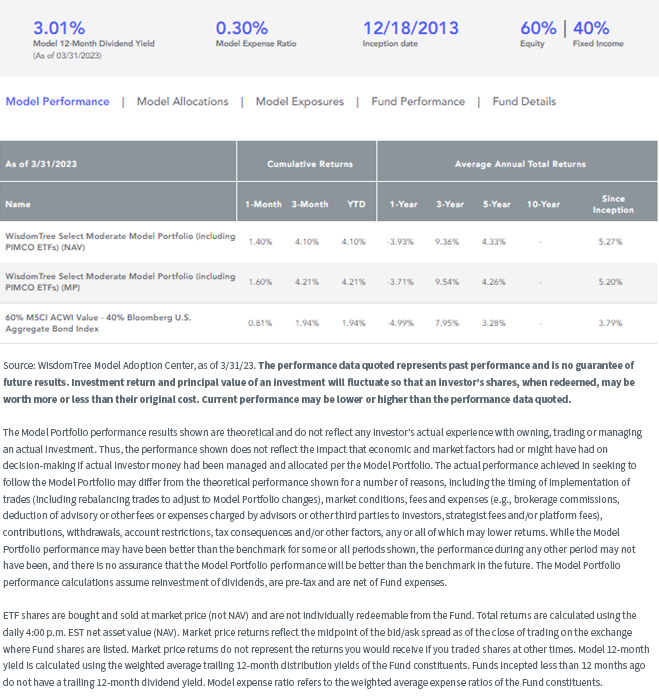

Select Models (with PIMCO)

These are multi-asset portfolios that we manage in coordination with PIMCO. All the equity allocations are WisdomTree products, while all the fixed income products are from PIMCO, a market leader in fixed income asset management.

WisdomTree is the “lead” portfolio manager, but our CIO of Fixed Income works closely with PIMCO to ensure that our outlooks and allocations remain aligned.

Q1 2023 saw these portfolios deliver a mixed bag of relative performances, with our conservative and moderate portfolios outperforming but our aggressive portfolio underperforming due primarily to its higher allocations to bank-ravaged mid-cap and multifactor equity exposures. Since inception in December 2013, however, all three models have outperformed their benchmarks. Here we use the “moderate” (60/40) model as an example.

WisdomTree Select Moderate Model Portfolio (including PIMCO ETFs)

For the most recent month-end performance and current 30-Day Sec Standardized Yield, please click here.

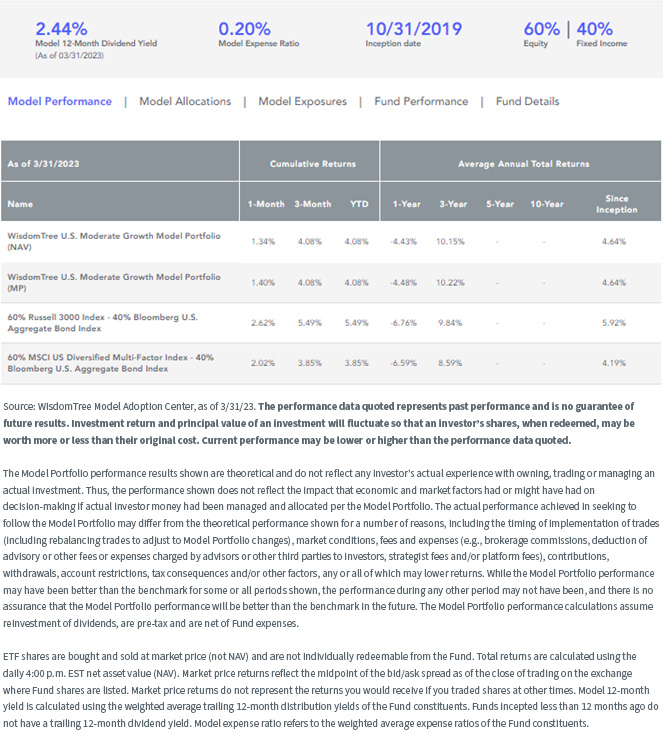

U.S. Growth Model

These models were developed in coordination with a large RIA that liked our approach to asset allocation and risk factor diversification but wanted a U.S.-only model to deploy with their client base. We were happy to help.

Although this is a customized model, it is available to other advisors on different platforms, so we are able to show performance and portfolio specifics.

The thesis behind these models, on the equity side, is similar to that of our U.S. multifactor model, which is then combined with a variation of our fixed income model and offered at different risk bands (conservative, moderate, aggressive, etc.).

Using the “moderate” (60/40) model as an example, we see underperformance in Q1 versus its primary benchmark (a combination of 60% Russell 3000 Equity Index and 40% Bloomberg U.S. Aggregate Bond Index. We saw similar underperformance levels in the other risk bands, driven by our value and SMID cap exposures within these portfolios.

If, however, we use the MSCI US Diversified Multi-Factor Index as a second equity index (an index more aligned with how we constructed and manage this portfolio), we see outperformance.

We see similar since-inception relative performances across all risk profiles.

WisdomTree U.S. Moderate Growth Model Portfolio

For the most recent month-end performance and current 30-Day Sec Standardized Yield, please click here.

Conclusion

As we saw in our strategic and outcome-focused models, there were things that worked and things that didn’t work as well for us in Q1. Our allocations to developed international (EAFE) and large-cap quality helped us. Our shorter duration profile in fixed income, in a quarter when rates fell, did not help us, nor did our allocations to value, dividend and SMID stocks.

This, of course, is exactly why we diversify at both the asset class and risk factor levels—our primary objective is to deliver more consistent performance over full market regimes. Our collective since-inception performances provide support for the “wisdom” (pun intended) of this approach.

Contact Us

Important Risks Related to this Article

For Financial Advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy.

For Retail Investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

Share & Comment

Popular Posts

Categories

Related Links