An “Un-Conditional” Guarantee?

Published January 18, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

The money and bond markets are already knee-deep in Fed policy conjecture only a couple of weeks into the new year. While the latest jobs data revealed a continued solid labor market setting to end 2022, other economic indicators, such as for manufacturing and services, pointed to real activity entering contractionary territory. Throw on top of that another report showing inflation has not only peaked but is continuing to “cool off,” and you get a full-fledged rally in the Treasury (UST) market.

While the dual mantras of “don’t fight the Fed” and “don’t fight the tape” battle it out (and will more than likely continue to do so for the foreseeable future), there is one aspect of monetary policy decision-making that is getting short shrift: financial conditions. Financial conditions have been an integral part of the Fed’s policy decisions, and the December 2022 FOMC minutes reinforced that this remains an important consideration in determining future assessments.

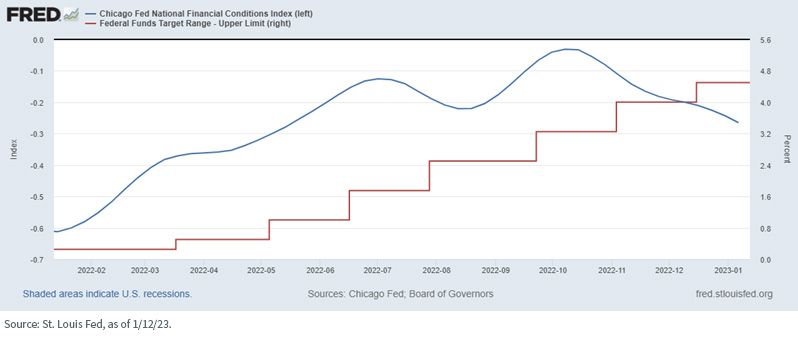

Against this backdrop, I thought it would be useful to provide some insights on the matter. I’m going to go out on a limb here and say that most market participants would probably think that, on the surface, given the “Volcker-esque” pace of rate hikes last year, financial conditions would have visibly tightened. Well, you would be partially correct. As measured by the Chicago Fed’s National Financial Conditions Index, things have tightened up from where they were prior to the Fed’s first rate hike last year, but after peaking in early October, a distinct loosening has since transpired. In fact, financial conditions in early January now stand at the same levels that existed back in May.

That brings us back to the Fed. In my opinion, there is little doubt that Powell & Co. are completely frustrated by this latest turn of events on the financial conditions front. To put it into perspective, even though the Fed raised the Fed Funds target range by an eye-opening 350 basis points (bps) since May, financial conditions are now unchanged from where they were seven months ago.

This frustration was on display in the aforementioned FOMC minutes. The minutes cited that “an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the committee’s reaction function, would complicate the committee’s efforts to restore price stability.”

Conclusion

Presently, the money and bond markets are debating whether the Fed will go with a 25-bp or 50-bp rate hike at the February 1 FOMC meeting but seem to be leaning toward the possibility that this next increase could potentially be the final move, and rate cuts will be forthcoming sooner than the policy makers have been saying. This is where the “real” disconnect lies; i.e., how long will the pause be? Based upon recent “Fed-speak,” Powell & Co. appear to be resolute in their stance that history has shown that “prematurely loosening policy” would be a mistake.

Buckle up—the volatility quotient is going to remain elevated!

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.