A Surprising Rebalance Season for S&P Style Indexes

Published January 5, 2023

Global Chief Investment Officer

The S&P family of growth and value style indexes conducted its annual rebalance in December, and there were some surprising twists and perhaps unexpected turnover this cycle.

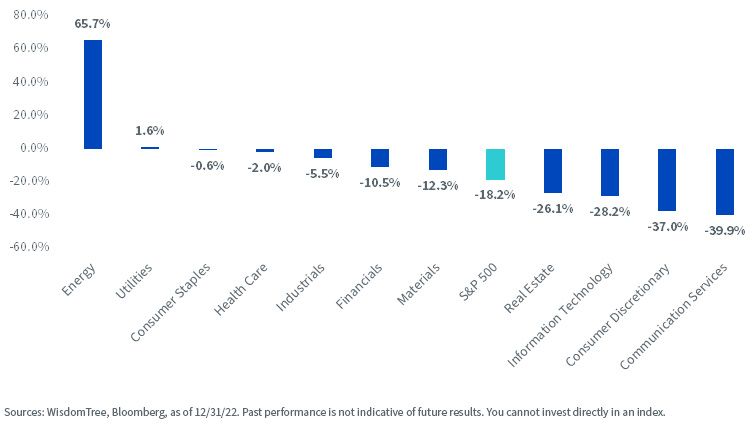

Notably, value indexes outperformed growth indexes across the board in 2022, as fears about elevated valuations in technology stocks dominated markets.

Energy stocks were the lone, large, bright spot, but defensive sectors like Utilities, Consumer Staples and Health Care also outperformed the broader S&P 500.

2022 S&P 500 Sector Total Returns

Despite Energy stocks remaining among the lowest sector valuations, the S&P value indexes dramatically reduced their weight while the growth indexes added more Energy exposure.

Below we will review Index composition changes across the large-cap (S&P 500), mid-cap (S&P MidCap 400) and small-cap (S&P SmallCap 600) benchmarks in the S&P family and explain what aspects of their style methodology caused these surprising shifts.

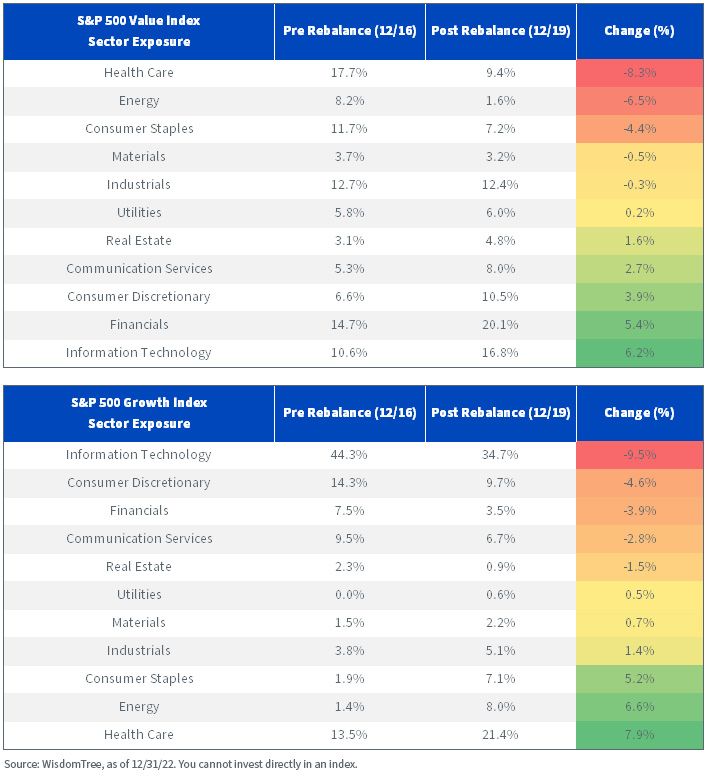

Within large-cap and the S&P 500 style benchmarks:

- In the S&P 500 Value Index, the greatest reductions in weight occurred in Health Care (-8.3%), Energy (-6.5%) and Consumer Staples (-4.4%). Those were three of the top four performing sectors in 2022.

- Meanwhile, three of the four sectors with the worst performance in 2022 (Information, Technology, Communication Services and Consumer Discretionary) received the largest increases in exposure.

- These same shifts were mirrored in the S&P 500 Growth Index, as the biggest increases in exposure included Health Care, Energy and Consumer Staples, while Technology sectors saw the greatest reduction in weight.

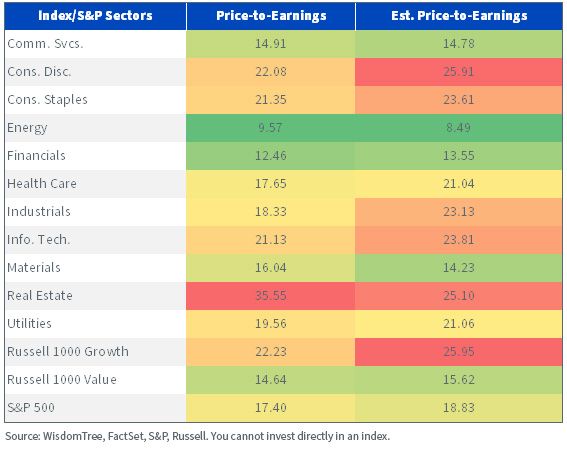

Notably, these shifts in Technology becoming more heavily weighted in value benchmarks, and Energy becoming more dominant in growth was not based on actual valuations.

Energy, despite being the cheapest sector in the market by price-to-earnings (P/E) multiple, became the lowest-weighted sector in the S&P 500 Value Index.

The Technology, Consumer Discretionary and Communications Services sectors had the highest P/E ratios despite receiving the largest increase in weight in the value benchmark.

Fundamentals - as of 12/31/22

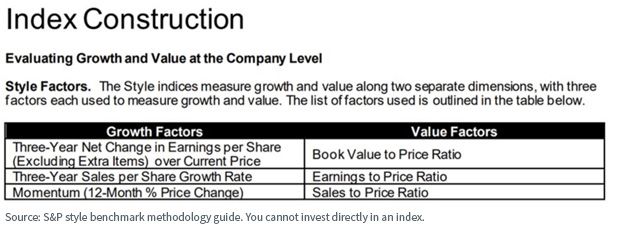

What explains the shifting sector weights, then? The below grid lists the factors in the S&P style family. Price momentum is one of the key growth factors utilized; clearly, that factor was an outlier in driving turnover.

The intersection of the S&P growth and value factor scores caused the Energy stocks to become weighted more heavily in growth, overcoming their low valuations.

Technology, although priced at high multiples, had such negative momentum that its growth scores plummeted enough to become more value-heavy in S&P’s scoring system.

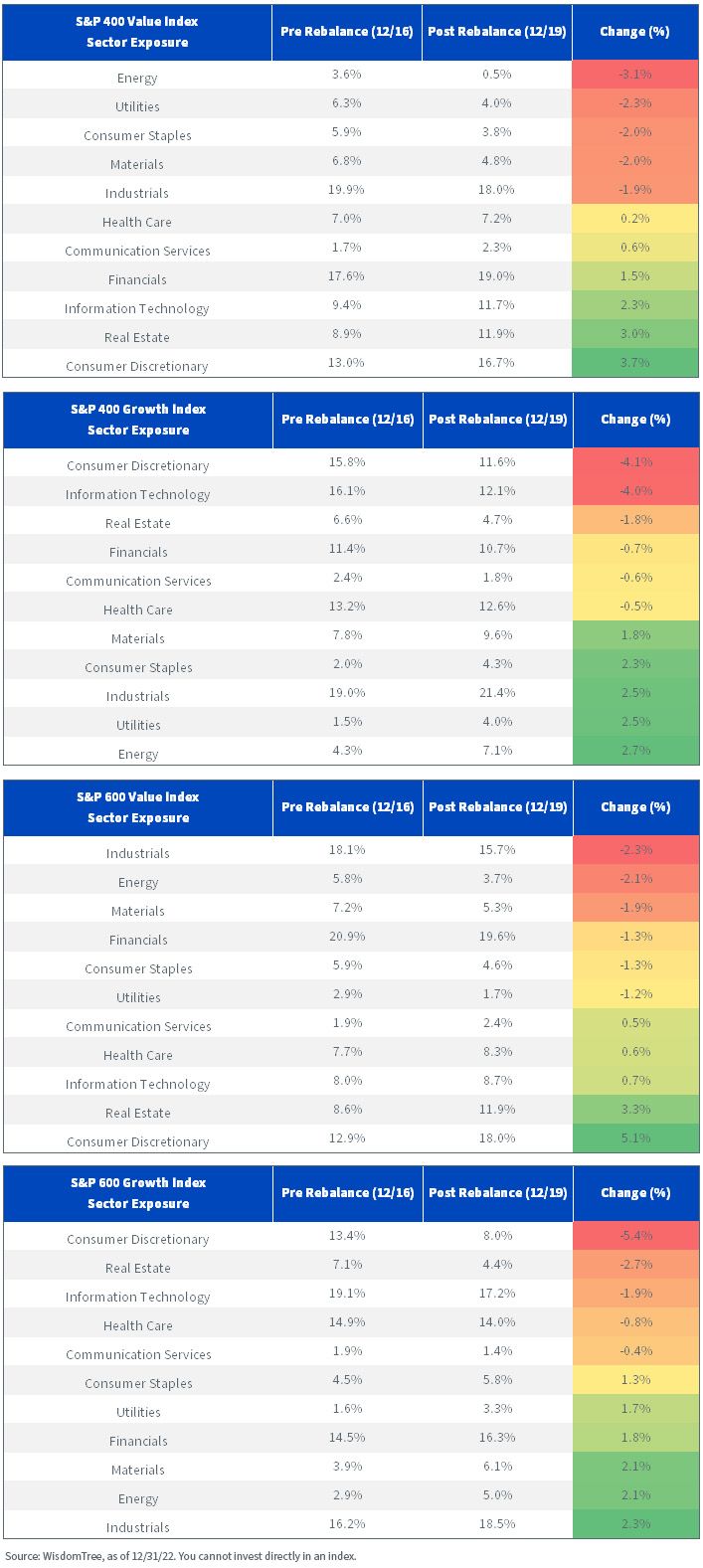

These changes were not limited to large caps. The tables below show similar shifts occurring in the mid- and small caps.

We see surprising shifts, like Utilities becoming more heavily weighted in the growth benchmarks. Energy and Consumer Staples moving from value to growth also occurred here in mid- and small caps.

WisdomTree also rebalanced its equity Index family in December, and we can share more specifics on each rebalance.

If you would like an updated look at valuations, we have a daily market dashboard that shows the P/E ratios of our ETFs against major benchmarks here.

Because of the turnover discussed above, the S&P 500 Value Index only has a single P/E point lower valuation than the S&P 500 (16.4x vs. 17.4x).

The WisdomTree U.S. High Dividend Fund (DHS) has a P/E ratio of 10.8x, more than six points lower than the S&P 500.

The WisdomTree U.S. LargeCap Dividend Fund (DLN) has a P/E ratio about two points lower than the S&P 500 Value Index (14.5 vs. 16.4) and three points lower than the S&P 500.

Again, these same features are mirrored in mid- and small caps, which we believe have attractive valuations overall.

This was quite the interesting rebalance season. It serves as a useful reminder that methodologies matter, and looking under the hood to understand portfolio composition is important since portfolios are not stagnant.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.