The Most Important Charts for 2022

In our view the most important market issue this year, aside from the coronavirus, is inflation.

The market has started pricing in three hikes from the Federal Reserve to combat inflation. We think there is upside risk to these rate hike forecasts.

Our Senior Investment Strategy Advisor, Jeremy Siegel, is the most aggressive with his calls that the Fed needs to get to over 2% for the Fed Funds Rate by year-end. That is nowhere near consensus and could create volatility in the markets if this forecast materializes.

Where should investors focus to protect purchasing power from the high inflation we see?

Bonds and cash are offering disappointing options.

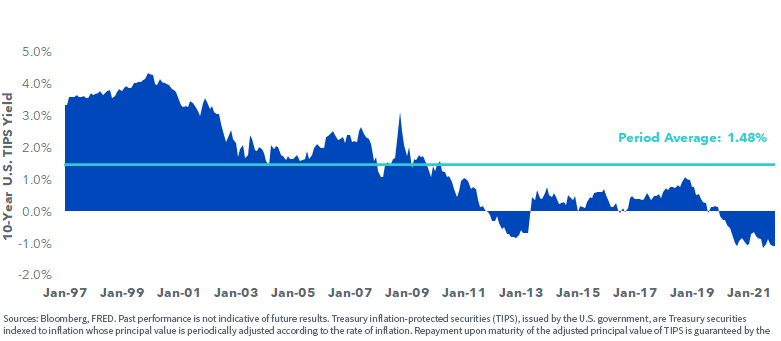

The yield on the Treasury Inflation Adjusted 10-Year Bonds—a very common choice for those who want inflation protection—have negative yields. Going back to its inception in 1997, when the Treasury first issued these securities, the average yield has been 1.5%—we are currently 2.5% below the long-term average TIPs yield.

A -1% TIPS yield implies you are handing the government $100 today and accepting $90 after inflation purchasing power 10 years later.

That seems wild and crazy in our view—but it is the current market dynamic.

10-Year U.S. TIPS Yields (1/31/1997—12/31/2021)

In our view, what you need are real assets that seek to provide positive returns but also hedge inflation. Stocks are such as an asset.

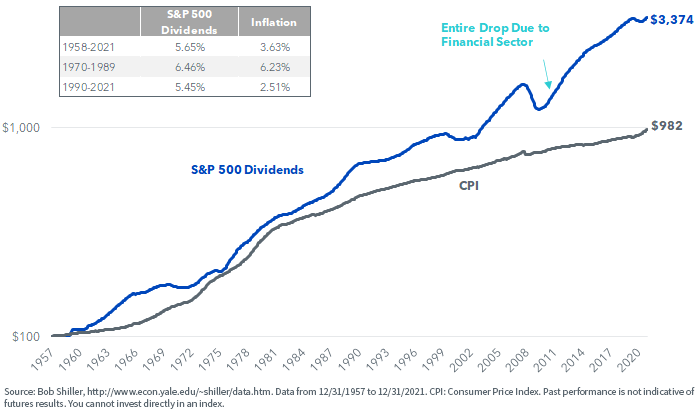

When you look at the long-term cash dividends on the S&P 500 going back to the inception of the index in 1957, inflation has averaged 3.6% but cash dividends have provided real growth on top of inflation.

This 2% real growth is one reason why we call stocks ‘Super TIPS,’ where stocks have provided purchasing power above the rate of inflation over the long term.

Even in high inflation decades of the 1970s and 1980s, dividend growth kept up with over 6% inflation for 20-years—beating inflation over that period.

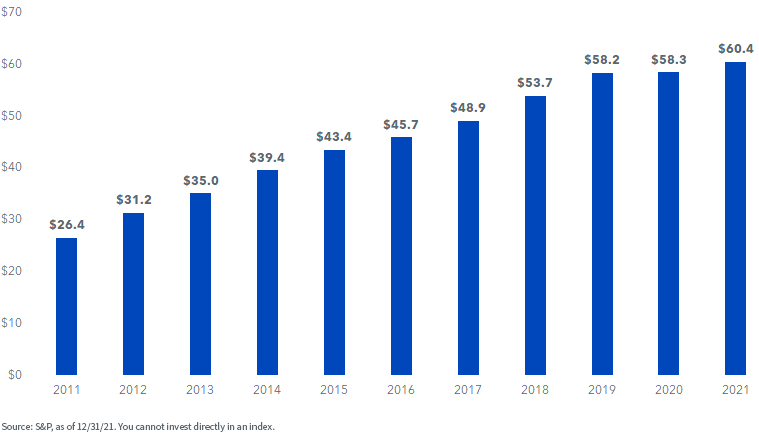

Some of the early behavioral finance work from Bob Shiller looks at the changes in the income stream of stocks—the underlying cash flows to investors—and stock prices and questioned why stock prices moved so much in excess of those fundamentals. That steady march higher in cash flows can be seen with the annual dividends per share on the S&P 500 over the last 11 years.

In 2020, during the pandemic, there were 42 companies in the S&P 500 that suspended dividends, but overall regular cash dividends per share were virtually unchanged.

In 2021, only one company suspended dividends and dividends per share grew 3.5%.

S&P 500 Index Dividends per Share

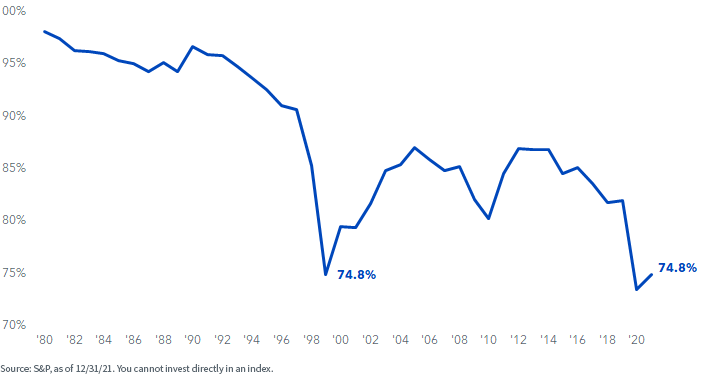

The strong performance in the technology sector has caused the weight on non-dividend paying stocks to rise such that dividend payers have fallen to 75% of the S&P 500 (after approaching 90% in 2013). This is one reason that yields have dropped—in addition to strong price performance ahead of dividend growth.

Weight of Dividend Paying S&P 500 Companies

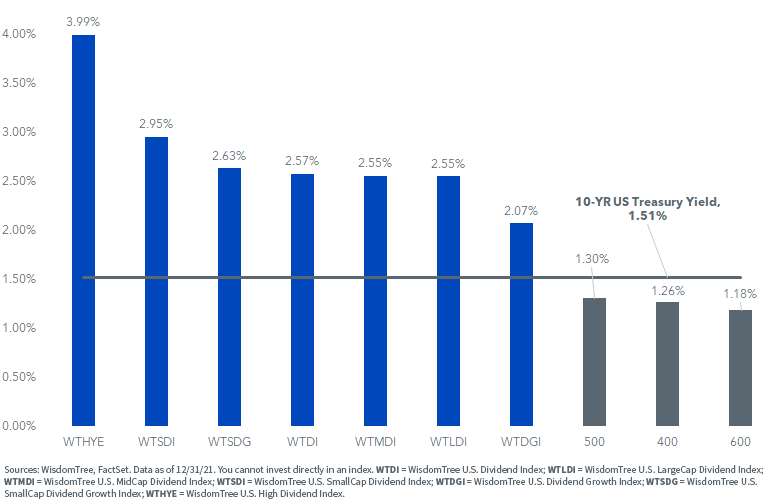

But when you remove non-dividend paying stocks from the universe, you can see index yields move higher.

- An index of 300 large cap dividend paying stocks (WTLDI) has an index yield approximately double that of the S&P 500.

- The mid-cap index and small-cap indexes have more than double the dividend yields of the comparable cap-weighted counterparts and that is because those indexes have even less of their weight in dividend paying stocks.

- Yields can be increased even further if you select based on high dividends.

We have talked about how in today’s macro environment, a stock’s duration (or sensitivity to interest rates) is going to be a prime factor. Stocks with current cash flows are trading as lower duration assets—while the mega-growth stocks have been getting repriced aggressively to start 2022.

Given the historical long-term nature of tech out-performance and the large adjustment we still see in the Fed cycle, this will be a theme we come back to again and again in 2022.

Indicated Dividend Yield

Important Risks Related to this Article

Past performance is not indicative of future results. You cannot invest directly in an index. Index performance does not represent actual fund or portfolio performance. A fund or portfolio may differ significantly from the securities included in the index. Index performance assumes reinvestment of dividends but does not reflect any management fees, transaction costs, brokerage commissions on transactions. Such fees, expense and commissions would reduce returns.

Share & Comment

Popular Posts

Categories

Related Links

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.