China and India Energy: Two Countries for the Same Tale?

Chinese equities, particularly offshore equities, suffered relentlessly in the headlines for their negative performance. India was the other way around: people likely remembered India’s heartbreaking pictures of its COVID surge, but not its top-performing equity market.

Figure 1: YTD Performance and Sector

For definitions of indexes in the chart, please visit the glossary.

But when it comes to energy—particularly coal-generated electricity—the two countries are remarkably similar.

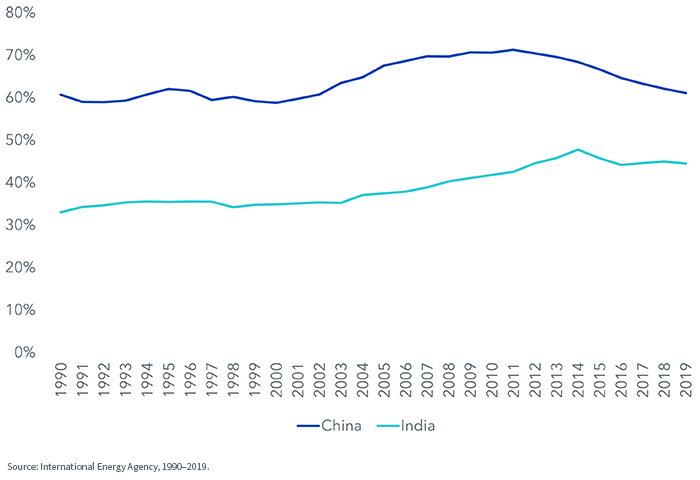

About 70% of both China and India’s electricity are generated from coal. It’s the single largest energy source, for electricity and other uses, in both countries. As shown in the chart below China has a higher percentage of coal as energy source, which expands past electricity, than India.

Figure 2: China and India: % Energy Sources from Coal

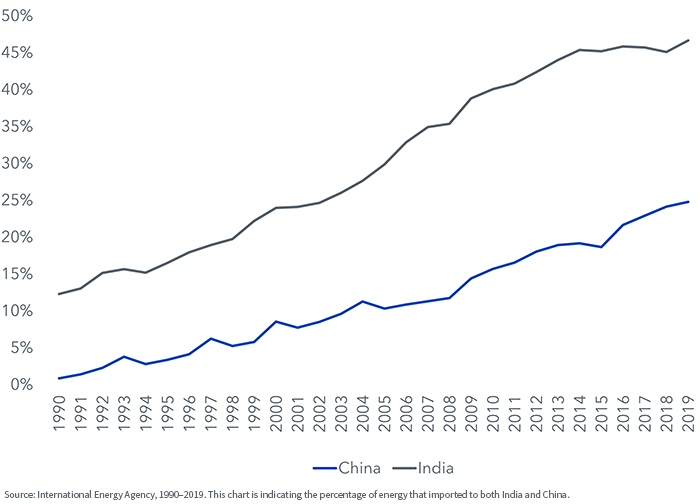

And both India and China have been increasingly reliant on imported energy, which includes coal, oil and others.

Figure 3: India and China Energy Supply: % Imports

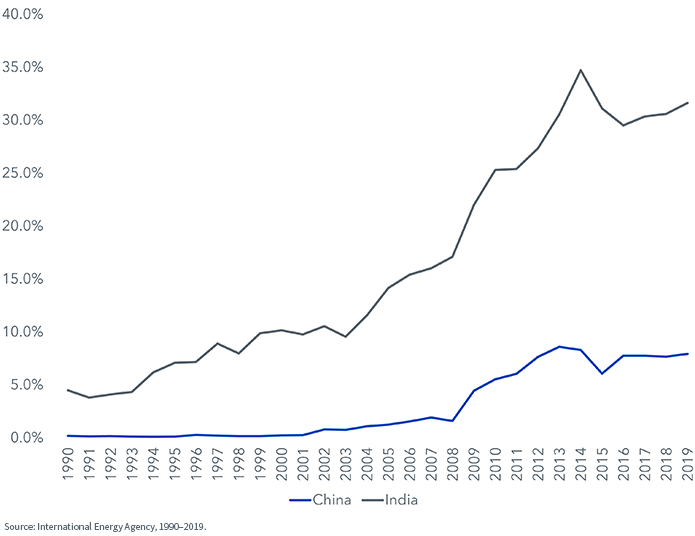

But in China, less than 10% of coal is imported. Because most top coal producers are state-owned, the government also has some power in influencing the coal price.

Figure 4: India and China Coal: % Imported

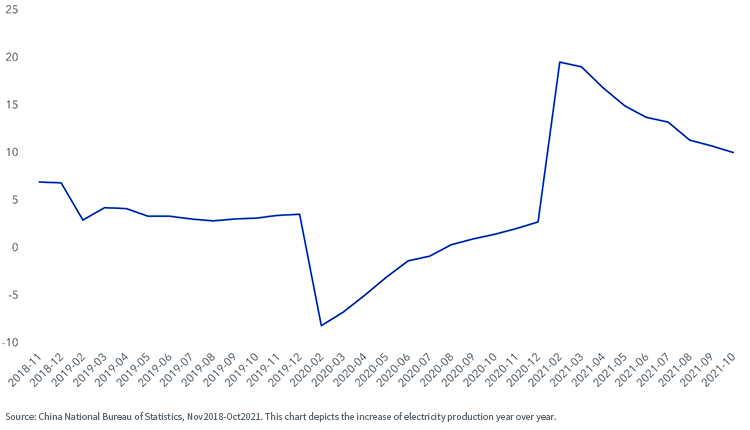

This was the energy and coal landscape in September when China was facing an electricity shortage. It was forced to ration electricity until early November, except for those companies considered highly energy inefficient, such as aluminum production.

Because China has relied on exports for its growth, which tend to come more from manufacturing than services, electricity demand has gone up significantly. Coal prices were very low in 2020 due to the pandemic, depressing coal output, and then reversed rapidly. Electricity prices are regulated, which created a perfect storm as many electricity generating companies were reluctant to generate electricity at a loss.

The following chart illustrates how dramatic electricity demand has increased after initial COVID-related economic slowdown in 2020.

Figure 5: China Electricity: YTD Cumulative Electricity Production (%y/y)

In the last two months, China’s National Development and Reform Commission (NDRC) has asked state-owned coal producers to increase output and prioritize coal transportation, increased coal imports, relaxed the price band for electricity trading and allowed electricity prices to increase 50% for high-energy-use industries.

The Zhengzhou futures exchange also put limits on who, and how many, domestic coal futures contracts could be traded, reducing financial speculation. Coal prices, though still elevated, have come down significantly.

The energy crunch thus far has been alleviated, before it made real, negative economic impact, with the manufacturing official Purchasing Manager Index (PMI) dipping into contraction in October.

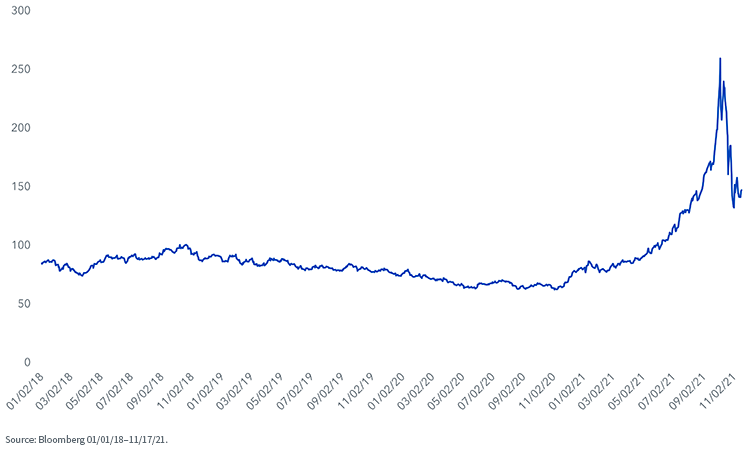

Figure 6: New Castles Coal Futures Price

In the short term, the current Chinese energy crunch is close to being over. But in the long run, energy will continue to be the constraining factor for Indian and Chinese growth.

The more volatile the weather and global demand, the more India and China will rely on coal for energy.

As we discussed with Chase Taylor of Pinecone Macro in the China of Tomorrow podcast, electricity and energy demand, in our opinion, will not be peaking soon. It is no wonder that while China and India promised carbon neutrality in 2060 and 2070 respectively, both countries want watered down language on coal usage in their commitments and are muted on any concrete targets in the next 5–10 years.

You can listen to the full episode below:

Share & Comment

Popular Posts

Categories

Related Links

Liqian Ren, Ph.D., joined WisdomTree as Director of Modern Alpha in 2018. She leads WisdomTree’s quantitative investment capabilities and serves as a thought leader for WisdomTree’s Modern Alpha® approach. Liqian was previously at Vanguard, where she worked for 12 years, most recently as a portfolio manager in the Quantitative Equity Group managing Vanguard’s active funds and conducting research on factor strategies. Prior to joining Vanguard, she was an associate economist at the Federal Reserve Bank of Chicago. Liqian received her bachelor’s degree in Computer Science from Peking University in Beijing, her master’s in Economics from Indiana University—Purdue University Indianapolis, and her MBA and Ph.D. in Economics from the University of Chicago Booth School of Business. Liqian co-hosts a podcast on China and Asian markets with Jeremy Schwartz, WisdomTree’s Global Head of Research, and she is a co-host on the Wharton Business Radio program Behind the Markets on SiriusXM 132.