“One Small Step for Managers, One Giant Leap for Bitcoin” - On the Edge of a Paradigm Shift

Mainstream adoption of technology occurs when a system is robust, and its value is recognized by the public. To quantify these measures, let’s talk about utility value and speculative value.

Utility value refers to the benefits that the technology provides, reflected by its demands.

Speculative value is when investors believe the technology is worth a value based on future expectations.

Both factors are essential in advancing a system’s expansion—utility value is unsubstantiated if speculative value doesn’t grow, and conversely, speculative value is artificial if utility value doesn’t follow.

Bitcoin’s recent growth is fueled by both aspects. Its ecosystem has matured, leading to more applications in real life. In anticipation of its wider adoption, financial institutions started delving into the crypto space, resulting in a strong inflow of capital.

Unlike its 2017 retail frenzy, bitcoin’s recent upsurge is partly driven by financial institutions’ interests.

In our first blog post of the series, we introduced corporations’ purchases of bitcoin as part of their balance sheet assets. Here, we will discuss the second source of institutional demand—the investment management industry’s participation.

A Shift in Narrative and Perception

Financial institutions’ views of bitcoin have been evolving.

In the beginning, bitcoin was mainly regarded as electronic cash, and many saw it as a means to facilitate illicit activities. As time passed, analysis by blockchain analytics companies like Chainalysis have helped debunk the idea that bitcoin is mostly used for illicit activities—the estimated amount of laundered money accounts for 2%–5% of global GDP ($800B–$2T), while total illicit value including money laundering related to cryptocurrency accounts for 0.34% ($10B) of its transaction volume.1

The narrative also shifted to acknowledge bitcoin as a financial asset for the potential store of value, largely per virtue of its limited supply, as well as a candidate for consideration in portfolio diversification.

The current inflationary and low-yield environment aids the financial asset narrative, as fiat money and bonds become less attractive vehicles to store value. Furthermore, companies’ plans to accept bitcoin and blockchain technology’s applications demonstrate one aspect of bitcoin’s utility value. Bitcoin’s growing influence has boosted end clients’ interests to capture the potential upside of this new technology. Their interests have in turn encouraged asset managers to incorporate it into portfolios.

The Bitcoin Ecosystem Evolution

Structurally, the underlying bitcoin network has matured since its birth. The fact that bitcoin has been in place for more than a decade is a testimony of its operational validity.

Not only are the mining machines used today much more advanced, but miners and users also expanded significantly: There are now more than 76K mining nodes and 1.2M active bitcoin addresses.2

The evolution of bitcoin can also be seen through the development of its trading infrastructure. Trading volumes on the eight major exchanges have passed $11B, reaching an all-time high.3 Compared to the early days when bitcoin first started trading, the current infrastructure offers better custody solutions, more efficient pricing, higher liquidity and easier access.

- Better Custody – When someone “owns” bitcoins, what they really own are the private keys associated with their bitcoin wallets. In the past, investors either self-custodied or stored their keys in exchanges’ hot wallets. These methods led to regrettable password losses and high-profile hacks. Firms have stepped in with custody solutions to provide safer and more convenient options to protect bitcoin ownership. They generally achieve this by storing private keys (or key fragments) offline—commonly referred to as cold storage. Other technologies, such as multi-party computation (MPC), have also enabled secure key storage.

- More Efficient Pricing and Higher Liquidity – Market makers such as DRW’s Cumberland, Jane Street, Jump Trading and Flow Traders entered the crypto space as early as 2014. They provide liquidity, minimize slippage and reconcile prices across platforms by arbitraging the difference away. Their involvement creates a more efficient market to execute trades.

- Easier Access – Institutional investors now have more tools to obtain bitcoin exposure. Bitcoin futures have grown significantly over the years. We are also witnessing the expansion of Europe’s bitcoin ETP market, as well as the birth of North America’s bitcoin ETF market. Moreover, exchanges such as Coinbase and Gemini are building trading systems that resemble equity systems to bring the traditional securities experience to the crypto world.

Bitcoin’s network expansion has eased institutional investors’ concerns about legitimacy. The development in bitcoin’s trading infrastructure has paved the way for the entrance of institutional investors.

How Can Investors Get Access to Bitcoin?

Investment managers, either directly or through their affiliates, are taking steps to provide bitcoin exposure to end clients. Some of the measures include establishing crypto trading operations, offering custody services, financing transactions and allocating to bitcoin in their investment funds.

- Direct physical holding of bitcoins, often through custodians.

- Investment through bitcoin exchange-traded products (ETPs/ETFs), which eliminates the burden of managing keys and custody for the investor while providing physical exposure.

- Synthetic exposure through regulated futures like the CME instrument, offering the usual advantages that come with any other commodity futures contract (settlement, ease of shorting, leverage, etc.).

- Indirect investment through equities, such as cryptocurrency mining companies or companies that hold bitcoin in their corporate treasury.

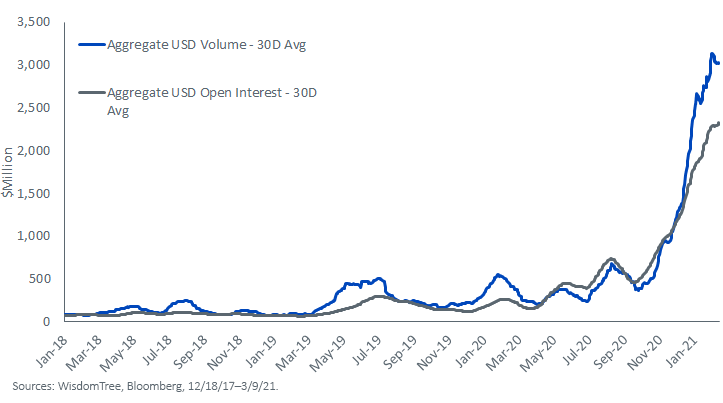

Institutional Money Entering the Futures Market

Regulated bitcoin futures debuted in December 2017 on the Chicago Mercantile Exchange (CME). Since then, a lot of new buyers have been entering the market via futures. They include family offices, asset managers and hedge funds.

Because most participants from this channel adhere to strict compliance rules and are prohibited from trading unregulated futures on retail platforms, bitcoin futures’ open interests and volume on regulated exchanges are important indicators for institutional activities.

Recently, we have witnessed a strong pickup in institutional demand, reflected by significant rises in open interest (over $2B) and trading volume (close to $2.8B) on the CME Bitcoin futures.

Figure 1: Bitcoin Futures on CME

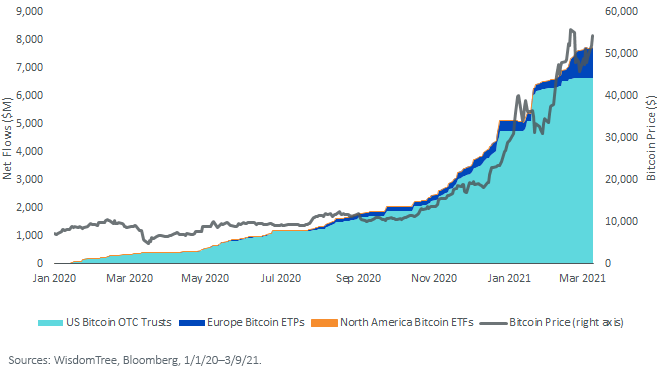

Bitcoin Trusts and ETPs Bringing Strong Inflows

Bitcoin trusts, private funds and ETPs have also taken in significant money in recent months. Since January 2020, bitcoin ETPs took in nearly $900M in inflows.

The flow has been dominated by European products, and the North American funds are on the rise with the recent launch of Canadian ETFs. OTC-traded trusts, which are currently trading in the U.S. and have existed for a longer period of time, have taken in an even greater sum of money.

Figure 2: Cumulative Net Flows into Global Bitcoin Funds

In February 2021, bitcoin ETFs gained regulatory approval in Canada and began trading on the Toronto Stock Exchange. In just one month, the combined AUMs of such ETFs rose to more than $580M USD. Other jurisdictions, including the U.S., may follow by allowing bitcoin-focused ETFs and/or allocating greater exposure to bitcoin futures in U.S.-registered ETFs.

As we’ve discussed in other blog posts, we believe ETPs and ETFs can provide effective access to bitcoin for investors. The flows into these vehicles indicate continued retail and institutional interest in the asset class.

Conclusion

It is important to recognize that bitcoin’s ecosystem is not yet fully developed, but it is equally important to acknowledge that its landscape is changing rapidly.

As bitcoin grows organically and realizes its utility value, we believe its speculative value will be gradually substantiated. At this moment, we are witnessing the beginning of a new paradigm, shifting away from a quasi-exclusive retail asset to a more widely accepted financial instrument.

1Chainalysis 2021 Crypto Crime Report, https://www.unodc.org/unodc/en/money-laundering/overview.html

2Colin Harper, “Are You Running a Bitcoin Node?” Coindesk.com, 1/29/21. https://www.coindesk.com/are-you-running-a-bitcoin-node

3The eight exchanges refer to Bitfinex, Coinbase, Kraken, Bitstamp, bitFlyer, Gemini, itBit and Poloniex. https://www.coindesk.com/bitcoin-active-addresses-trading-volumes-all-time-highs

Important Risks Related to this Article

Please note WisdomTree Asset Management, Inc., does not offer any bitcoin products.

Bitcoin operates as a decentralized, peer-to-peer financial exchange and value storage that is used like money. Bitcoin operates without central authority or banks and is not backed by any government. Bitcoin generally experiences very high volatility. Bitcoin is also not legal tender. Federal, state or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in the U.S. is still developing. Bitcoin exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers or malware.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Unless expressly stated otherwise, the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

There are risks associated with investing, including the possible loss of principal. Crypto assets, such as bitcoin and ether, are complex, generally exhibit extreme price volatility and unpredictability and should be viewed as highly speculative assets. Crypto assets are frequently referred to as crypto “currencies,” but they typically operate without central authority or banks, are not backed by any government or issuing entity (i.e., no right of recourse), have no government or insurance protections, are not legal tender and have limited or no usability as compared to fiat currencies. Federal, state or foreign governments may restrict the use, transfer, exchange and value of crypto assets, and regulation in the U.S. and worldwide is still developing. Crypto asset exchanges and/or settlement facilities may stop operating, permanently shut down or experience issues due to security breaches, fraud, insolvency, market manipulation, market surveillance, KYC/AML (know your customer/anti-money laundering) procedures, noncompliance with applicable rules and regulations, technical glitches, hackers, malware or other reasons, which could negatively impact the price of any cryptocurrency traded on such exchanges or reliant on a settlement facility or otherwise may prevent access or use of the crypto asset. Crypto assets can experience unique events, such as forks or airdrops, which can impact the value and functionality of the crypto asset. Crypto asset transactions are generally irreversible, which means that a crypto asset may be unrecoverable in instances where: (i) it is sent to an incorrect address, (ii) the incorrect amount is sent or (iii) transactions are made fraudulently from an account. A crypto asset may decline in popularity, acceptance or use, thereby impairing its price, and the price of a crypto asset may also be impacted by the transactions of a small number of holders of such crypto asset. Crypto assets may be difficult to value, and valuations, even for the same crypto asset, may differ significantly by pricing source or otherwise be suspect due to market fragmentation, illiquidity, volatility and the potential for manipulation. Crypto assets generally rely on blockchain technology, and blockchain technology is a relatively new and untested technology that operates as a distributed ledger. Blockchain systems could be subject to internet connectivity disruptions, consensus failures or cybersecurity attacks, and the date or time that you initiate a transaction may be different than when it is recorded on the blockchain. Access to a given blockchain requires an individualized key, which, if compromised, could result in loss due to theft, destruction or inaccessibility. In addition, different crypto assets exhibit different characteristics, use cases and risk profiles. Information provided by WisdomTree regarding digital assets, crypto assets or blockchain networks should not be considered or relied upon as investment or other advice, as a recommendation from WisdomTree, including regarding the use or suitability of any particular digital asset, crypto asset, blockchain network or strategy. WisdomTree is not acting and has not agreed to act in an investment advisory, fiduciary or quasi-fiduciary capacity to any advisor, end client or investor, and has no responsibility in connection therewith, with respect to any digital assets, crypto assets or blockchain networks.

Share & Comment

Popular Posts

Categories

Related Links

Jianing Wu joined WisdomTree as a Research Analyst in October 2018. She is responsible for analyzing market trends and helping support WisdomTree’s research efforts. Previously, Jianing completed internships and projects at Geode Capital, Starwint Capital, and Invesco Great Wall Fund Management with a focus in quantitative research. Jianing received her M.S in Finance from the Massachusetts Institute of Technology. She graduated with honors from Boston College with degrees in Mathematics and Philosophy.