Have You Rate Hedged Yet?

Thus far in 2021, the overarching theme in my blog posts and podcasts has been the ‘Reflation Trade’ and how investors should be considering rate-hedged strategies within their fixed income portfolios. Last week’s spike in the U.S. Treasury (UST) 10-Year yield was a not-so-subtle reminder that rate hedging remains an active consideration for the bond market investment landscape.

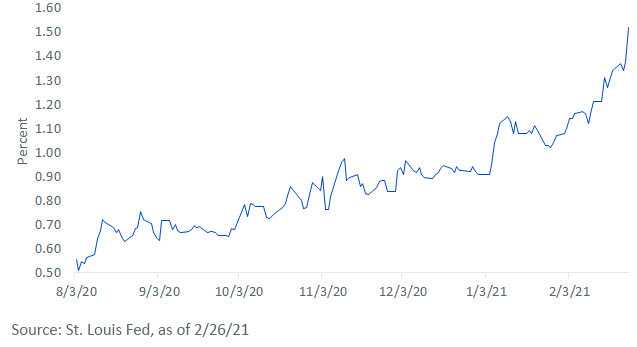

The graph below takes a little bit of a longer look back, rather than just focusing on 2021 developments. As you can see, the rise in the UST 10-Year yield actually began in early August when the all-time low watermark of 0.51% was registered on August 4. As I write, the rate increase since that date has been an eye-opening 101 basis points (bps). However, the development that is getting the lion’s share of attention is what has transpired thus far this year, when the rise has been pegged at a little more than 60 bps.

U.S. Treasury 10-Year Yield

In fact, that’s exactly the issue—60% of the increase in the UST 10-Year yield occurred in less than two months’ time. So, what are the culprits? Here’s a list of the top five:

- The aforementioned Reflation Trade—inflation expectations have increased due to unprecedented monetary and fiscal stimulus, with an additional huge amount of the latter seemingly on the way

- The Federal Reserve’s (Fed) increasingly dovish policy stance, which was highlighted by Chair Powell at last week’s Semiannual Monetary Policy Report testimonies—is the Fed in danger of falling behind the inflation curve?

- Better-than-expected Q1 economic data, especially for consumer spending, which has led forecasts such as the Atlanta Fed’s GDPNOW estimate to pin growth at just under +9% for this quarter

- Budget deficits, maybe—up until very recently, it didn’t look like they mattered, but the $62 billion UST 7-Year note auction last week was abysmal, perhaps suggesting that investors are demanding higher yields to underwrite such enormous auction amounts

- Technicals—various Fibonacci retracement levels have been ‘blown through’, with higher targets seemingly coming into play every week of late, if not every day

Solutions to Consider

Based on the fundamental and technical outlook, it appears as if a further rise in the UST 10-Year yield is still a distinct possibility. A retracement back to the pre-pandemic trading range of 1.75%–2.00% could be on the horizon.

Here are three rate-hedge solutions to consider:

- UST-based: WisdomTree Floating Rate Treasury Fund (USFR) vs. TIPS. 10-Year TIPS, or real, yields are not immune and have risen 50 bps this year.

- Investment-grade: WisdomTree Interest Rate Hedged US Aggregate Bond Fund (AGZD) vs. corporate floating-rate vehicles. Higher yield, with more diversification (representative of the AGG) and less concentration in the financial sector.

- Core plus: WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD) vs. bank loans. A quality screen that tilts for income and targets zero duration.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new and the amount of supply will be limited. The value of an investment in USFR may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. AGZD and HYZD seek to mitigate interest rate risk by taking short positions in U.S. Treasuries (or futures providing exposure to U.S. Treasuries), but there is no guarantee this will be achieved. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions.

Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. AGZD and HYZD may engage in “short sale” transactions where losses may be exaggerated, potentially losing more money than the actual cost of the investment and the third party to the short sale may fail to honor its contract terms, causing a loss to the Funds. While the Funds attempt to limit credit and counterparty exposure, the value of an investment in the Funds may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Funds’ portfolio investments. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated or defaulted on. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links