A Reflation Shock: The Catalyst for Small and Mid Cap Value?

It is an understatement to say that 2020 was tough for value investors.

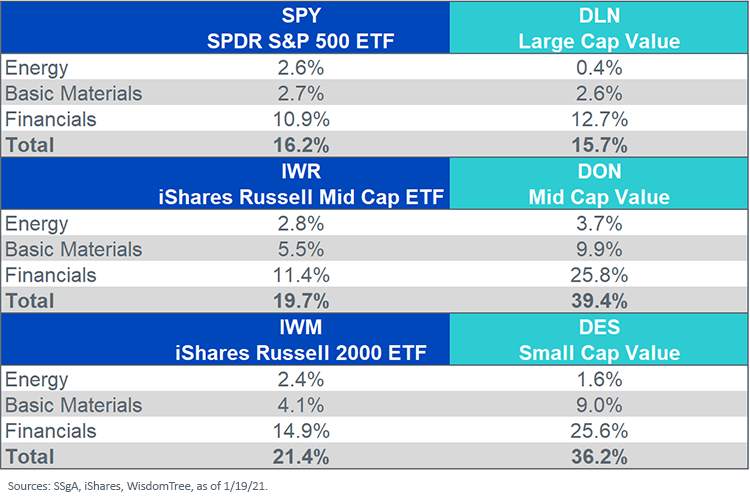

Stocks in the Energy, Materials and yield-sensitive Financials sectors were left wanting last year. That meant pain for reflation-heavy small- and mid-cap stocks, owing to their sizable weights in those groups. Our small and mid cap dividend-oriented value index (in teal in figure 1) are particularly heavy in them

Figure 1: Sector Weights, Reflation Beneficiaries

For definitions of indexes in the chart, please visit our glossary.

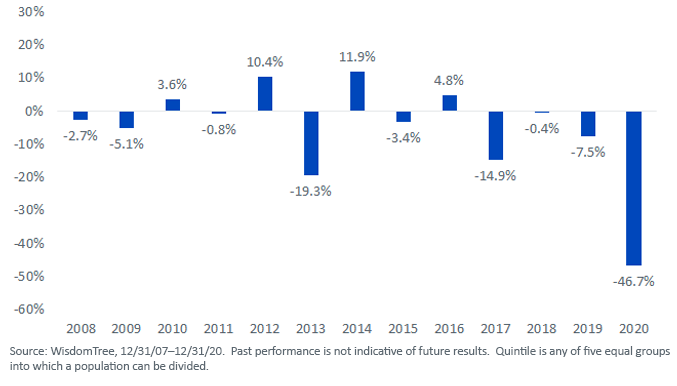

Aside from the post-March bounce back in just about every asset class, disinflationary themes still dominated our Covid-19-focused world.

Figure 2: Return of Top Dividend Yield Quintile Minus Return of Non-Payers, Russell 2000 Index

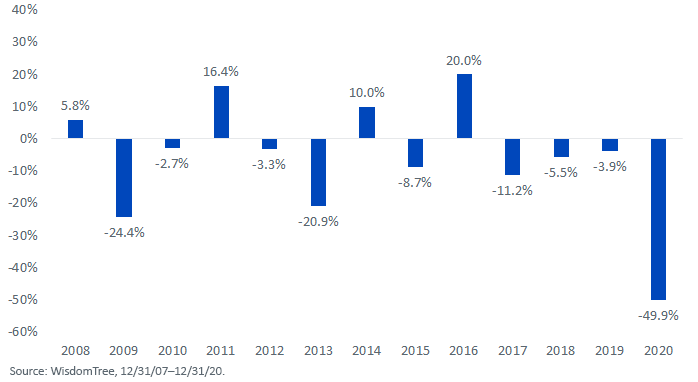

Not to be outdone, mid-cap companies with zero dividends—often in Tech, Healthcare and Communications Services—outperformed the highest-yielding quintile of stocks by 49.9% last year.

Figure 3: Return of Top Dividend Yield Quintile Minus Return of Non-Payers, Russell Midcap Index

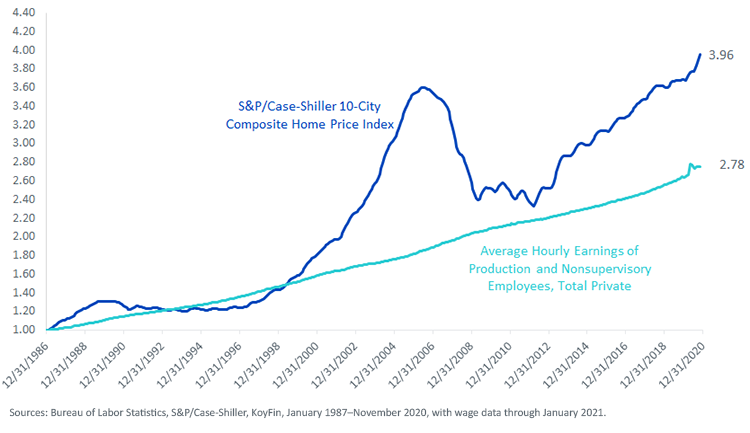

What are the sparks that could provide the catalyst for an embrace of inflationary themes? For one, most housing markets are red hot. It’s a sellers’ market.

Figure 4: Monthly Supply of New Houses in the U.S. (SA)

.png?h=435&w=750&hash=DE6715EFEEA76F863D13BD8CACDA1216)

The S&P/Case-Shiller 10-City Composite Home Price Index is well past the housing bubble peak, at least in non-inflation-adjusted terms. No surprise—Freddie Mac’s national average conforming mortgage rate was about 2.75% in January.

The median U.S. existing home price for December was $309,800, a cool doubling off the January 2012 low of $154,600.

Then again, wages need to catch up.

Figure 5: U.S. Home Prices vs. Wages (January 1987 = 1.00)

The bond market has an upset stomach.

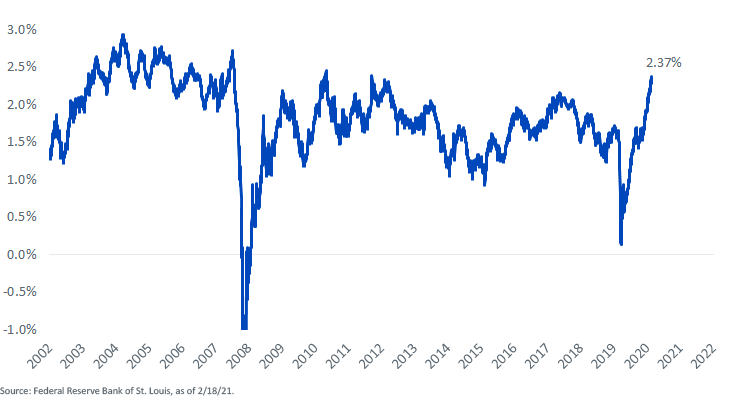

The breakeven inflation rate is derived from a comparison of the yield on vanilla Treasuries and those of Treasury Inflation-Protected Securities (TIPS). The market’s expectation for inflation over the next five years went up through 2% a few weeks ago (figure 6). It’s still tame, yes, but running hotter.

Figure 6: U.S. 5-Year Breakeven Inflation Rate

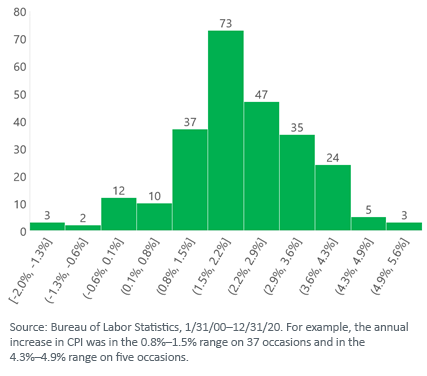

It’s a rare bird on the Street that is penciling in anything like an inflation shock. BofA Merrill Lynch, Barclays, Citi and JPMorgan Chase are all forecasting U.S. Consumer Price Inflation of 2.0%–2.4% for 2021. Look at the histogram of yearly inflation readings since 2000 (figure 7). I suspect many investors are ill-prepared for the very real odds of an upside deviation, perhaps into the 3-4% area.

Figure 7: Yearly U.S. Consumer Price Inflation Frequency (January 2000–December 2020)

Suppose inflation starts to boil, or at least simmer, supporting Energy and Materials at the expense of disinflationary Tech.

Interest rates could also rise in that scenario—after all, bondholders will need a larger yield to justify their positions. With the Fed Funds rate pegged to the 0.00%–0.25% range, the attendant yield curve steepening could be accretive to banks’ profitability.

With one-quarter of the WisdomTree U.S. MidCap Fund (DON) and the WisdomTree U.S. SmallCap Fund (DES) in Financials—and with both having sizable holdings in Materials—we believe they could be primed for outperformance if our post-Covid-19 world starts witnessing the right-hand side of the histogram.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.Share & Comment

Popular Posts

Categories

Related Links