The Historic Opportunity in Small-Cap Value

Last week we hosted Chris Meredith, Director of Research, Co-Chief Investment Officer and a portfolio manager at O’Shaughnessy Asset Management (OSAM), on our “Behind the Markets” podcast. OSAM is a systematic factor investor that manages about $5 billion in quantitative strategies. Meredith joined OSAM in 2005 and is co-responsible for research, investing and trading at the firm.

At a time when growth has dominated value as an investment style, causing many to question their devotion to value disciplines, Meredith shared his work on what contributed to value’s underperformance.

Why Does Value Usually Work?

Meredith highlighted his paper “Factors from Scratch” that shows how value stock pricing is often too pessimistic on future earnings trends, where earnings are lower than they are for most other firms but not as low as would be justified by their prices. The average discount is about 17%, but that valuation gap closes over the subsequent three years.

Most often, growth areas of the market are priced at such premium multiples that when those companies grow earnings at premium rates, the prices started so high that future growth rates inevitably disappoint. In other words, faster growth is already priced in, and it is difficult to live up to those elevated expectations. Yet over the last 12 to 13 years, the growth rates have nevertheless surpassed high expectations. Meredith thinks that will be a tough trend to uphold.

Historic Opportunity

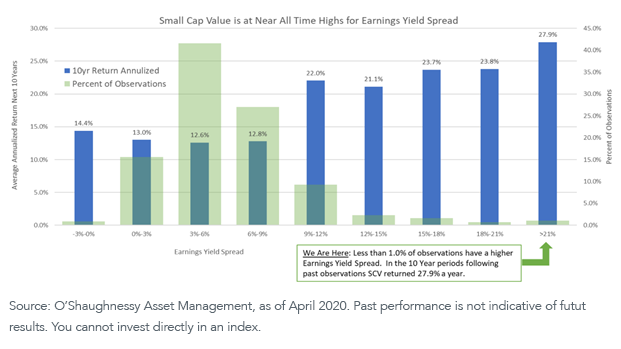

There are a few different charts below that we discussed on the podcast and which illustrate how OSAM sees the current situation as unique for small-cap value investors, from a piece they published in April 2020.

First, when measuring small-cap value earnings yields versus Treasury yields, historical spreads as wide as the current ones have occurred less than 1% of the time.

The 10-year forward-looking returns from various earnings yield spreads is also graphed, and they were dramatically higher the more the earnings yield spread over Treasuries widened.

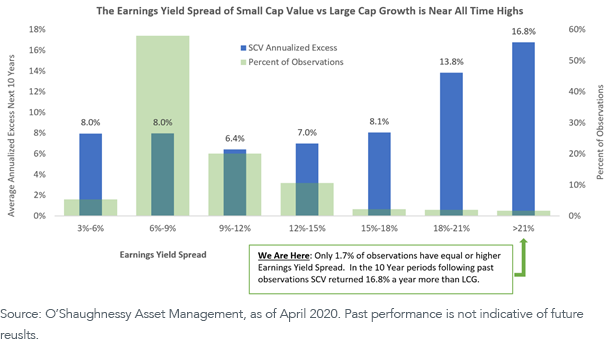

There was a similar relationship that held if one compared small-cap value earnings yields versus large-cap growth earnings yields, where yield spreads were this wide less than 2% of the time.

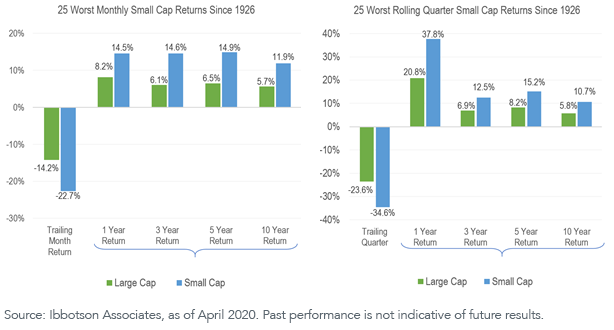

While the future is never exactly like the past, if one does not believe the valuation argument, past return patterns of underperformance similar to first quarter underperformance led to higher returns consistently one, three, five and ten years into the future.

We also talked about Canvas, a new investing platform the OSAM team is developing to help advisors manage their business and offer trading capabilities built on OSAM’s separate account infrastructure. Canvas is still relatively early in its rollout, but the team is seeing strong engagement from their test clients on the platform.

This was a great discussion, and you can listen to the full conversation below.

Share & Comment

Popular Posts

Categories

Related Links

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.