Why ‘Stagflation’ Could Polarize Gold and Silver

With the Federal Reserve maintaining a hawkish tone, bond yields have risen, and the U.S. dollar remains strong. As a result, we have slightly reduced our gold forecasts. But the risk of central banks overdoing it could send gold soaring, especially if inflation remains high while economic growth is suffering. In a base case of inflation moderating without a recession, silver should largely keep up with gold. However, an industrial downturn could hurt silver disproportionately relative to gold.

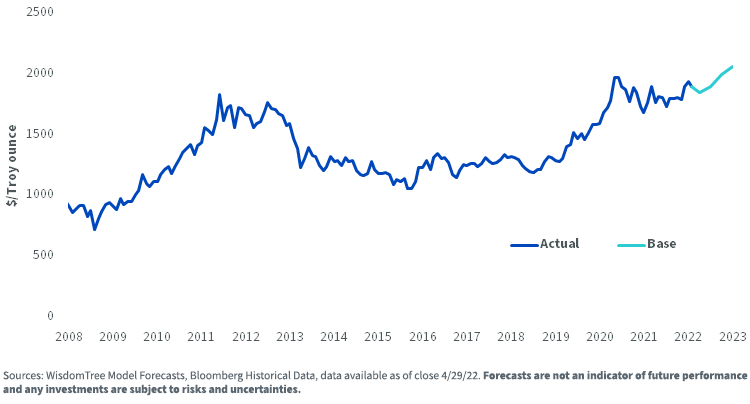

Revising gold forecasts

Using consensus economic forecasts for inflation, bond yields and the U.S. dollar basket from Bloomberg surveys in March 2022, we had projected a consistent gold price of US$2,315/oz by Q1 2023. Since then, consensus economic views have shifted, acknowledging the bond sell-off and a stronger U.S. dollar. Consensus has also revised inflation forecasts upward, acknowledging the stubbornness of prices despite the hawkish actions of central banks. Higher bond yields and a stronger U.S. dollar are negative for gold, while higher levels of inflation are gold price positive.

Our model indicates that by Q1 2023, gold prices will still rise (US$2,060/oz, figure 1), but not as much as we had expected (US$2,315/oz) when the bond and U.S. dollar headwinds were lower. We assume, in our revised forecast, that 10-year bond yields rise to 3.2% (currently 2.80%1), the U.S. dollar basket appreciates to 105 (currently 1022) by Q1 2023 and inflation only moderates to 4.3% (from 8.3% in April 20223).

Figure 1: Gold price forecast

Gold keeps on defying bond headwinds

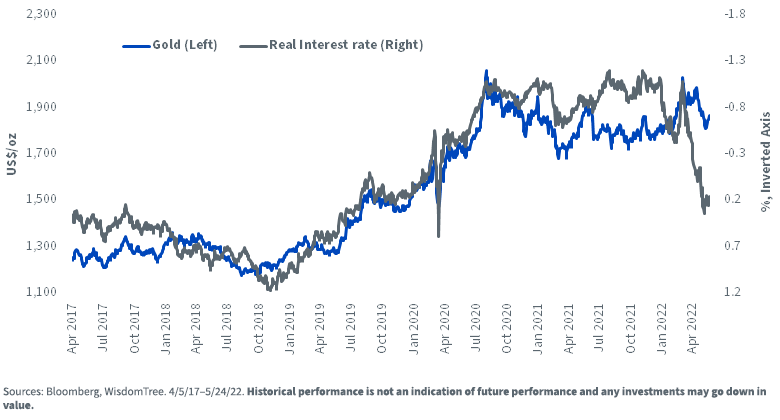

We have observed that gold is holding up well relative to bond markets, breaking down the traditionally strong relationship between gold and Treasury Inflation-Protected Securities (figure 2). Gold is an asset that generally performs well in adverse economic and financial conditions. With fears of a recession rising, investors are increasingly turning to gold as hedge. We have seen 7.3 million ounces of inflows into global gold exchange-traded commodities (ETCs) in the year, to May 24, 2022 (compared to a net outflow of 9.2 million ounces in full year 2021).4

Figure 2: Gold vs real rates (Treasury Inflation-Protected Securities yield)

Stagflation could be good for gold

Traditionally, recessions tend to moderate price pressures. However, when price increases are generated by external shocks, we may not see that come to effect. Market pundits are increasingly talking about ‘stagflation’—a recession combined with high inflation. Today, we are facing energy price shocks and food shortages—consequences of the COVID pandemic and the war in Ukraine. The impact of these events does not appear to be fading as much as many had hoped.

Episodes of stagflation are extremely rare and, therefore, making quantitative conclusions from them is fraught with difficulty. Between Q3 1973 and Q1 1975, U.S. GDP had been declining in real terms and, over that period, inflation rose from 7.4% to 10.3%.5 In the same period, gold prices had risen 73%.6 In the late 1970s, we also saw economic deceleration7 combined with accelerating inflation, with gold prices more than doubling in calendar year 1979.

Silver riding on gold’s coattail, for now

Using our revised base case gold forecast, our silver model indicates that silver prices are likely to rise to US$25.89/oz (from US$21.93/oz8) by Q1 2023. Mining capital expenditure has been rising in recent years and that could drive silver out of a supply deficit in the coming year. We assume that manufacturing activity (proxied by manufacturing Purchasing Manager Indexes) will continue to moderate but won’t fall below 50 (that is, won’t contract in outright terms).

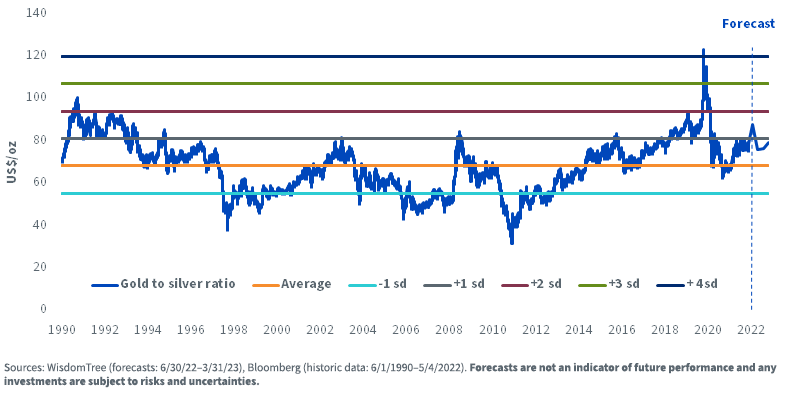

Our silver forecast indicates that the gold-to-silver ratio (figure 3), which is currently elevated,9 could moderate a little.

Figure 3: Gold-to-silver ratio

A recession could treat silver differently to gold

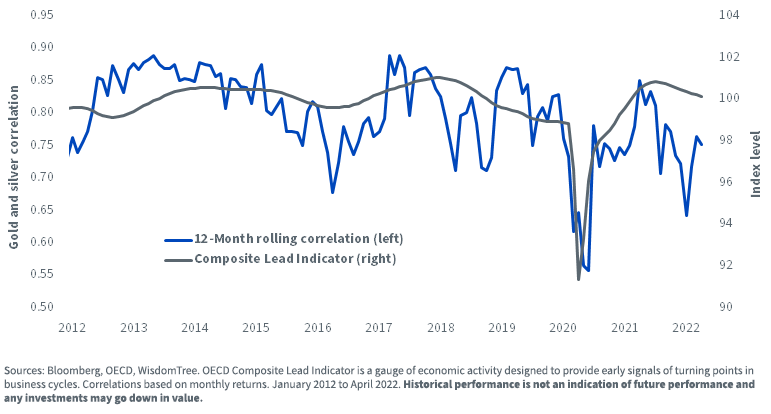

Our silver model assumes that the metal’s sensitivity to gold prices is broadly stable through the economic cycle. However, in reality, the correlation between the two metals fluctuates (figure 4). We believe that if recession becomes the main driver of the gold price, manufacturing activity could contract, placing negative pressure on silver, while gold prices continue to rise. That could send the gold-to-silver ratio higher.

Figure 4: Gold and silver correlations change through the cycle

Conclusions

Gold and silver are facing headwinds from higher bond yields and an appreciating U.S. dollar, but stubbornly high inflation should see their prices continue to rise.

To stress, a recession is not our base case scenario, but markets are increasingly worried about the economy tipping over. Gold could outperform silver in such a scenario.

Accessing gold

Adding gold exposure to a portfolio has become easier with the launch of WisdomTree’s Capital Efficiency family of products. The WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) overlays gold futures on top of traditional large-cap equities. The WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN) does the same for a portfolio of gold mining equities. These strategies aim to deliver exposure to gold with efficiency through the use of futures instead of tying up all capital in the physical metal.

1 Source: Bloomberg, 05/24/22.

2 Source: Bloomberg, 05/24/22.

3 Source: Bloomberg, 05/24/22.

4 Source: Bloomberg, 05/24/22.

5 Source: Bloomberg.

6 Source: Bloomberg.

7 Although the economy was decelerating, the U.S. only fell into the technical definition of a recession in 1980 (that is, with two consecutive quarters of real GDP decline).

8 Source: Bloomberg, 05/24/22.

9 Is more than a standard deviation above the average since 1990.

Important Risks Related to this Article

Nitesh Shah is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree Investments, Inc.

GDMN: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.