Should We Care About the Yield Curve Going Forward?

While scant attention is currently being given to the shape of the Treasury yield curve, I wondered what the future would hold. Certainly, there are a lot of other pressing issues making headlines, but what happens the next time the curve inverts—will it still be viewed as having the same predictive value as we have seen in the past?

Depending on the maturities one examines, the Treasury yield curve actually inverted as far back as last March, utilizing the 3-month/10-year measure. My preferred gauge, the 2-year/10-year differential, was historically flat at that time, and it didn’t go into negative territory until August. Needless to say, the narrative once again centered on these inversions as potentially signaling an upcoming recession.

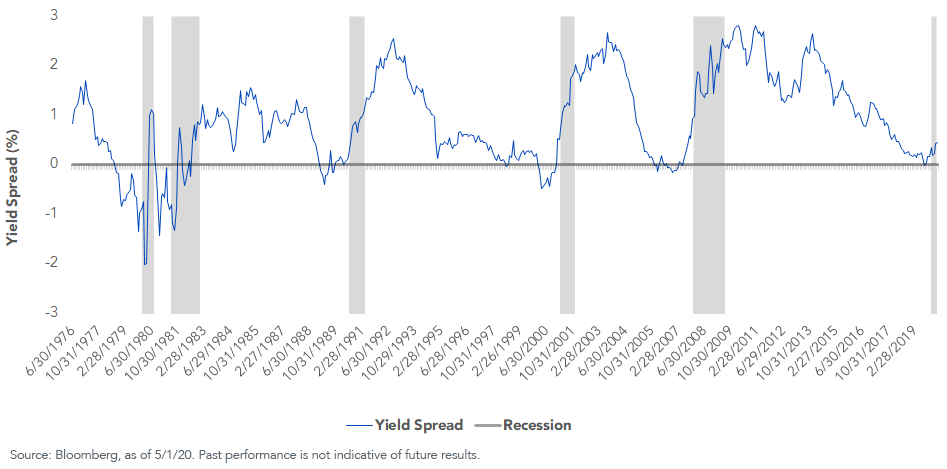

UST 2-Yr/10-Yr Spread

As the graph clearly reveals, the facts don’t lie. Utilizing the UST 2-year/10-year spread, history shows that when this differential went negative, a recession typically ensued. Thus, the expectation from the inverted relationship of about eight months ago would put the U.S. economy on the brink of a contraction right about now, or probably within the next few months at the latest.

Well, guess what? U.S. Q1 real GDP came in at -4.8%, as reported last week. While one quarter does not fit the technical recession definition of two consecutive quarters of negative GDP, I don’t think anyone would argue that Q2 economic activity will be in contraction territory as well. In fact, estimates at this point for are an eye-opening decline of anywhere from -30% to -40% for real GDP in Q2. If you were wondering, this is why my graph has already shaded in a recession coming up.

Okay, so the inverted yield curve kept up its track record of predicting recessions, right? Not so fast, my friend. During last year’s inverted episode, I argued that the Federal Reserve’s (Fed) buying of Treasuries via past quantitative easing (QE) operations, and term a term premium, probably skewed the curve’s predictive value. I was more of a proponent of wanting to see a more prolonged period of inversion with deeper negative spreads to allow for the two aforementioned factors.

By the way, that didn’t happen…. Unfortunately, COVID-19 happened instead. I think it is very reasonable to assume the U.S. economy could have avoided a recession if not for this unfortunate turn of events. While growth was not “knocking it out of the park,” the GDP was still humming along nicely at a +2.1% pace, and the Fed had just cut rates by 75 basis points (bps) during the second half of 2019.

Conclusion

Well, guess what? The Fed is now embarking on a QE program on steroids. Just in the last seven weeks, the policymakers have purchased an incredible $1.4 trillion in Treasuries. In other words, if you thought the Fed’s balance sheet altered the historical relationship between inverted yield curves and recessions before, I can’t imagine you’d think the curve’s predictive value hasn’t been affected perhaps permanently now…. Just some food for thought.

Unless otherwise stated, data source is Bloomberg, as of May 1, 2020.

Share & Comment

Popular Posts

Categories

Related Links