WisdomTree’s Quality Dividend Growth Strategy Turns 10

Published April 27, 2023

Head of Indexes, U.S.

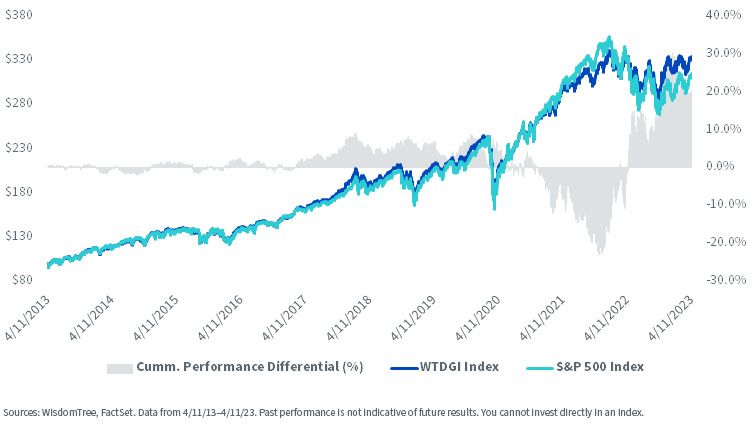

The WisdomTree U.S. Quality Dividend Growth Index (WTDGI) had its 10-year anniversary on April 11.

It was the first of a family of 11 Indexes that span different geographic focuses.

WTDGI is tracked by the WisdomTree U.S. Quality Dividend Growth Fund (DGRW).

The investment objective of the strategy has remained consistent, providing investors with exposure to companies that look attractive across measures of profitability, like return on equity (ROE) and return on assets (ROA), and earnings growth prospects, and weighting them by their dividend stream to maintain valuations at check.

WTDGI’s way of assessing a company’s quality (profitability) and ability to grow dividends has allowed it to outperform the S&P 500 Index by 0.70% annually over these 10 years, doing so with lower volatility and higher risk-adjusted returns.1

Growth of 100

Genesis of the Strategy (Ethos of the Strategy Remains Unchanged)

When WTDGI launched in 2013 after extensive research, our now Global CIO, Jeremy Schwartz, and Global Head of Research, Christopher Gannatti, published two white papers titled “The Dividends of a Quality and Growth Factor Approach” and “Waiting for Dividends vs. Weighting by Dividends.” Jeremy and Chris expanded on the rationale for using ROE and ROA as the measure of quality along with having a forward-looking dividend growth screen instead of a backward-looking one. They also highlighted how a broad quality methodology would be better positioned to compete against the broader market over time.

Quality Factor Rankings: “We have identified higher-quality companies as those that have displayed above-average historical returns on equity and on assets. We have used these criteria as part of our selection methodology, because we believe companies with better profitability metrics are better able to fund growing dividends.… There are also the investment practitioners who focus on ROE. Warren Buffett often says, as he did in his most recent (2014) annual letter, that he looks for “businesses earning good returns on equity while employing little or no debt.” Since high leverage involves the use of debt, our use of a quality ranking that incorporates both return on equity and return on assets enables us to mitigate the use of leverage as a sole driver of what may superficially appear to be a high ROE figure.

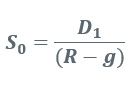

In the finance literature, return on equity is critically linked to dividend growth and intrinsic value of companies through the dividend discount model (DDM). The DDM for (current) stock valuation states:

where D1 represents dividends per share expected to be received in one year, R represents the required rate of return for the investment and g stands for the growth rate in dividends which can be decomposed into ROE x earnings retention.”2

Forward-Looking Dividend Growth Screen: “One of the most critical differences between the WisdomTree U.S. Dividend Growth Index and the NASDAQ US Dividend Achievers Select Index is that the latter requires 10 consecutive years of dividend growth in order to qualify for inclusion, while the former does not. Why does this matter? Because we believe that dividend indexes with backward-looking growth screens may fail to capture growth opportunities—and we believe that performance will bear this out….

A simple example of the difference is the case of Apple. As one of the largest dividend payers in the United States, Apple is included in the WisdomTree U.S. Dividend Growth Index —but it won’t be eligible for inclusion in the NASDAQ US Dividend Achievers Select Index until 2023. Additionally, it is worth noting that not only does WisdomTree require a dividend, it also uses numerous quality screens and weights by dividends.”3

Broad Exposure: “One of the keys, in our opinion, is to not dilute the potential power of what others have mentioned above (characteristics of different quality factor portfolios) by trying to apply too many stock selection rules or complex weighting schemes. The key is to be as simple and broad-based as possible, while still tilting toward companies with low debt and high return on equity, which we believe to be an important common thread across the many varied interpretations of what quality means to different practitioners.”4

Live Performance

Ten years of history allows us to go back and see how some of our initial research has played out in a live period. The below comes from our Index Attribution Tool and shows ROE quintile performance attribution of WTDGI versus the S&P 500 from April 30, 2013, to March 31, 2023.

This image shows how WTDGI’s over-weight in highest-ROE companies and under-weight in lowest-ROE companies have strongly contributed to its outperformance over the past 10 years.

It’s interesting to highlight the right-most column, where we can see that, over this period, the highest-ROE companies in the S&P 500 outperformed the market by more than 300 basis points (bps), while companies with the lowest ROE underperformed the market by close to -200 bps.

WTUSMF - WisdomTree U.S. Multifactor IndexWTEPS - WisdomTree U.S. LargeCap IndexWTDGI - WisdomTree U.S. Quality Dividend Growth IndexWTQGRW - WisdomTree U.S. Quality Growth IndexWTLDI - WisdomTree U.S. LargeCap Dividend IndexWTDI - WisdomTree U.S. Dividend IndexWTHYE - WisdomTree U.S. High Dividend IndexWTSDG - WisdomTree U.S. SmallCap Quality Dividend Growth IndexWTMEI - WisdomTree U.S. MidCap IndexWTSEI - WisdomTree U.S. SmallCap IndexWTSDI - WisdomTree U.S. SmallCap Dividend IndexWTMDI - WisdomTree U.S. MidCap Dividend IndexWTEMSC - WisdomTree Emerging Markets SmallCap Dividend IndexWTEMHY - WisdomTree Emerging Markets High Dividend IndexEMXSOE - WisdomTree Emerging Markets ex-State-Owned Enterprises IndexINXSOE - WisdomTree India ex-State-Owned Enterprises IndexCHXSOE - WisdomTree China ex-State-Owned Enterprises IndexWTIND - WisdomTree India Earnings IndexWTEHIT - WisdomTree Europe Hedged Equity Index (TR)WTIDJTRH - WisdomTree Japan Hedged Equity Index (TR)EMCLOUD - BVP NASDAQ Emerging Cloud IndexWTCDG - WisdomTree Canada Quality Dividend Growth IndexWTMDIC - WisdomTree U.S. MidCap Dividend Index CADWTMDIHC - WisdomTree U.S. MidCap Dividend Index CAD-HedgedWTGDHY - WisdomTree Global High Dividend IndexWTGDXG - WisdomTree Global ex-U.S. Quality Dividend Growth IndexWTIDGH - WisdomTree International Hedged Quality Dividend Growth IndexWTDFA - WisdomTree International Equity IndexWTDFAHD - WisdomTree Dynamic Currency Hedged International Equity IndexWTDHYE - WisdomTree International High Dividend IndexWTILDI - WisdomTree International LargeCap Dividend IndexWTIDG - WisdomTree International Quality Dividend Growth IndexWTIMDI - WisdomTree International MidCap Dividend IndexWTISDI - WisdomTree International SmallCap Dividend IndexWTISDIHD - WisdomTree Dynamic Currency Hedged International SmallCap Equity IndexWTIDJH - WisdomTree Japan Hedged Equity IndexWTEDG - WisdomTree Europe Quality Dividend Growth IndexWTEHIP - WisdomTree Europe Hedged Equity IndexWTGEH - WisdomTree Germany Hedged Equity IndexWTESC - WisdomTree Europe SmallCap Dividend IndexWTESEH - WisdomTree Europe Hedged SmallCap Equity IndexWTJSC - WisdomTree Japan SmallCap Dividend IndexWTJSEH - WisdomTree Japan Hedged SmallCap Equity IndexWTMDPL - WisdomTree Growth Leaders IndexWTDFAH - WisdomTree International Hedged Equity IndexWTDGICT - WisdomTree U.S. Quality Dividend Growth Index CAD (NTR)WTDGIDCT - WisdomTree U.S. Quality Dividend Growth Index Variably CAD-Hedged (NTR)WTDGIHCT - WisdomTree U.S. Quality Dividend Growth Index CAD-Hedged (NTR)WTDXF - WisdomTree U.S. Dividend ex-Financials IndexWTEHITC - WisdomTree Europe CAD-Hedged Equity Index (NTR)WTEMI - WisdomTree Emerging Markets Dividend IndexWTEMXC - WisdomTree Emerging Markets Ex-China IndexWTGRE - WisdomTree Global ex-US Real Estate IndexWTIDGCT - WisdomTree International Quality Dividend Growth Index CAD (NTR)WTIDGD - WisdomTree Dynamic Currency Hedged International Quality Dividend Growth IndexWTIDGDCT - WisdomTree International Quality Dividend Growth Index Variably CAD-Hedged (NTR)WTHYECT - WisdomTree U.S. High Dividend Index CAD (NTR)WTHYEHCT - WisdomTree U.S. High Dividend Index CAD-Hedged (NTR)WTIDGHCT - WisdomTree International Quality Dividend Growth Index CAD-Hedged (NTR)WTIDXF - WisdomTree International Dividend ex-Financials IndexWTISDIH - WisdomTree International Hedged SmallCap Dividend IndexVS.500 - S&P 500 Sector AttributionDividend Yield AttributionEarnings Yield AttributionReturn on Equity AttributionShareholder Yield AttributionSize AttributionVolatility AttributionAs of:12/31/201412/31/201512/30/20166/30/20177/31/20178/31/20179/29/201710/31/201711/30/201712/29/20171/31/20182/28/20183/29/20184/30/20185/31/20186/29/20187/31/20188/31/20189/28/201810/31/201811/30/201812/31/20181/31/20192/28/20193/29/20194/30/20195/31/20196/28/20197/31/20198/30/20199/30/201910/31/201911/29/201912/31/20191/31/20202/28/20203/31/20204/30/20205/29/20206/30/20207/31/20208/31/20209/30/202010/30/202011/30/202012/31/20201/29/20212/26/20213/31/20214/30/20215/31/20216/30/20217/30/20218/31/20219/30/202110/29/202111/30/202112/31/20211/31/20222/28/20223/31/20224/29/20225/31/20226/30/20227/29/20228/31/20229/30/202210/31/202211/30/202212/30/20221/31/20232/28/20233/31/20234/28/20235/31/20236/30/20237/31/20238/31/20239/29/202310/31/202311/30/202312/29/20231/31/20242/29/20243/29/20244/30/20245/31/20246/28/20247/31/20248/30/20249/30/202410/31/202411/29/202412/31/20241/31/20252/28/20253/31/20254/30/20255/30/20256/30/20257/31/20258/29/20259/30/202510/31/202511/28/202512/31/20251/30/20262/27/20263/31/2026MTDQTD1Y3Y5YSince Inception*

Attribution Component

Average Category Weight

Category Performance

Category

Allocation

Stock

Selection

Interaction

Total

Attribution

Index

Weight

Benchmark

Weight

+/- Wgt

WT Index

Return

Benchmark

Return

Industrials

0.01%

0.31%

0.32%

0.64%

18.99%

9.66%

9.33%

13.35%

11.00%

Health Care

0.07%

0.26%

0.13%

0.46%

14.93%

14.47%

0.46%

13.98%

12.52%

Real Estate

0.22%

-0.47%

0.47%

0.22%

0.28%

2.70%

-2.42%

-6.69%

6.86%

Utilities

0.16%

0.12%

-0.06%

0.22%

0.41%

3.05%

-2.65%

4.56%

8.58%

Energy

0.03%

0.01%

0.10%

0.14%

3.62%

6.06%

-2.44%

4.06%

4.50%

Information Technology

0.28%

-0.16%

-0.05%

0.07%

19.48%

18.06%

1.41%

20.56%

21.02%

Consumer Staples

-0.24%

0.13%

0.09%

-0.03%

16.05%

8.38%

7.67%

10.65%

9.70%

Financials

-0.07%

-0.09%

0.00%

-0.16%

7.28%

15.45%

-8.17%

10.44%

10.94%

Materials

-0.06%

-0.12%

-0.06%

-0.23%

3.48%

2.86%

0.61%

7.72%

10.20%

Consumer Discretionary

0.14%

-0.05%

-0.37%

-0.28%

10.99%

9.91%

1.08%

11.10%

12.32%

Communication Services

0.24%

-0.83%

0.18%

-0.41%

4.51%

9.40%

-4.89%

5.15%

10.34%

Total

0.76%

-0.89%

0.76%

0.64%

-

-

-

12.77%

12.14%

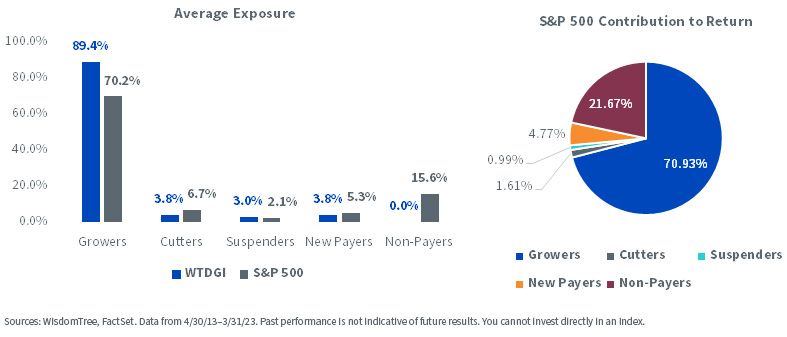

To analyze exposure to and the impact of dividend growers over time, we classified securities in WTDGI’s and the S&P 500’s universe into five groups, comparing their current dividend payments to what they were 10 years ago.

These groups were labeled: Growers, Cutters, Suspenders, New Payers and Non-Payers. Given what we know of equity markets in the past 10 years, it is not surprising to see that more than 70% of the S&P 500’s average exposure during the period was to companies that grew their dividends.

It is also good to see how WTDGI’s methodology has resulted in close to 90% of exposure to dividend Growers and has managed to reduce the exposure to Cutters and Suspenders compared to the S&P 500. If we look at the contribution to the S&P 500’s return during the period, companies that grew dividends contributed proportionally to their exposure, and New Payers contributed more than their exposure, while Cutters and Suspenders contributed less than their exposure.

Index Methodology

WTDGI’s annual rebalance methodology can be explained in the following stages:

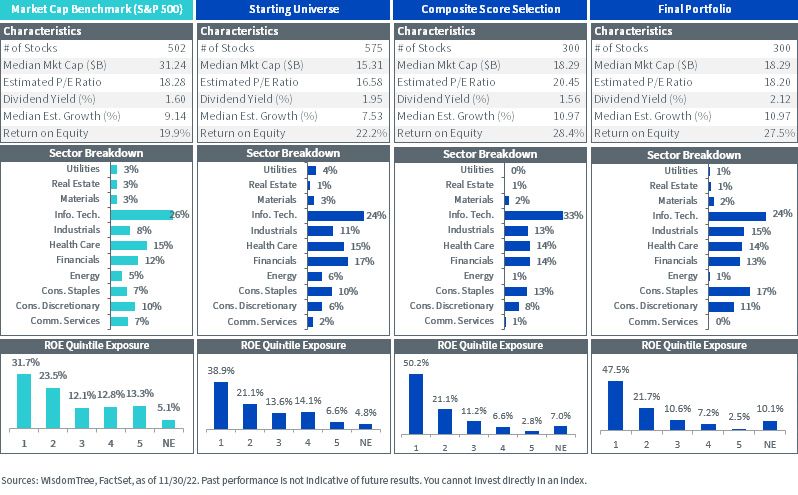

Starting Universe: The Index’s starting universe consists of dividend-paying U.S. equities that meet WisdomTree’s liquidity requirements and whose market caps exceed $2 billion. Companies whose dividend coverage ratios are less than 1 (i.e., dividends exceed earnings) are removed, as are companies flagged as risky by WisdomTree’s Composite Risk Score (CRS).

Composite Score Selection: Companies are then ranked based on an equally weighted composite score of growth and quality. Growth is defined as consensus estimated earnings growth over the next one to three years, while quality is calculated as a 50/50 score of the company’s average three-year ROE and ROA. The top 300 companies are selected for the portfolio.

Final Portfolio: The 300 companies selected are Dividend Stream® weighted to reflect the proportionate share that the aggregate cash divides. An individual holding cap of 7% is applied prior to a 20% sector cap for all sectors except Info. Tech (25%) and Real Estate (10%).

The below chart highlights the different stages of WTDGI’s latest rebalance at the end of 2022 and compares portfolio characteristics versus those of the S&P 500 (teal).

WTDGI’s starting universe already shows an important quality tilt coming from removing non-dividend payers and companies whose dividends exceed earnings or that are at risk of cutting their dividend payments as identified by the CRS score (higher aggregate ROE than the S&P 500 and higher/lower exposure to highest/lowest ROE quintiles).

Upon selecting the 300 best-scoring companies on the composite score of growth and quality, the basket exhibits stronger quality and growth characteristics. Aggregate ROE exceeds the S&P 500 by more than 8%, and the median estimated growth of the portfolio is close to 2% higher. More than half of the weight is allocated to the highest ROE companies. At this stage, the valuation and dividend yield metrics are higher and in line, respectively, with the S&P 500.

After Dividend Stream weighting the basket, we can see that the quality and growth advantages remain while forward valuation is now lower, and the dividend yield is 62 bps higher than the S&P 500. In terms of final sector composition, the model is over-weight in the Industrials and Consumer Staples sectors and under-weight in Communication Services and Energy.

Showing further granularity into the Index methodology, below is an example of the parameters used in the 2022 rebalance for two comparable companies, Morgan Stanley and JP Morgan.

The former made it into the final portfolio rebalance, while the latter was not included as it did not rank in the top 300 names on the composite score of growth and quality.

As seen below, even though both companies had comparable quality scores, it was Morgan Stanley’s growth estimate that made it rank within the top 300 names.

Morgan Stanley’s $5.24 billion of indicated dividends represents 1.74% of the total $302.79 billion of all 300 names selected into the basket. Thus, its final weight after single stock and sector adjustments was 1.79%.

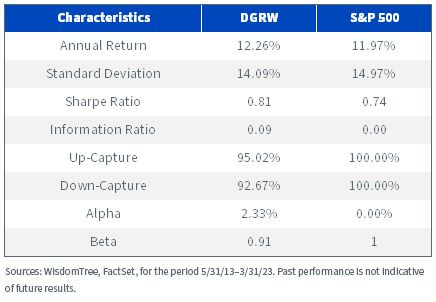

Quality Exposure = Better Risk-Adjusted Returns

As mentioned earlier, WTDGI’s methodology has allowed it to outperform the S&P 500 on both an absolute and a risk-adjusted basis. As we can see below, the risk characteristics for DGRW—which tracks WTDGI—are very attractive for a core exposure in an investor’s portfolio.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end performance, click here. Holdings are subject to change.

1 Sources: WisdomTree, FactSet. Data from 4/11/13–4/11/23.

2 Source: WisdomTree, “The Dividends of a Quality and Growth Factor Approach.”

3 Source: WisdomTree, “Waiting for Dividends vs. Weighting by Dividends.”

4 Source: WisdomTree, “The Dividends of a Quality and Growth Factor Approach.”

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

About the contributor

Head of Indexes, U.S.

Alejandro Saltiel joined WisdomTree in May 2017 as part of the Quantitative Research team. Alejandro oversees the firm’s Equity indexes and actively managed ETFs. He is also involved in the design and analysis of new and existing strategies. Alejandro leads the quantitative analysis efforts across equities and alternatives and contributes to the firm’s website tools and model portfolio infrastructure. Prior to joining WisdomTree, Alejandro worked at HSBC Asset Management’s Mexico City office as Portfolio Manager for multi-asset mutual funds. Alejandro received his Master’s in Financial Engineering degree from Columbia University in 2017 and a Bachelor’s in Engineering degree from the Instituto Tecnológico Autónomo de México (ITAM) in 2010. He is a holder of the Chartered Financial Analyst designation.