The Most Important Charts for 2023

Published February 23, 2023

Global Chief Investment Officer

Equity Strategist

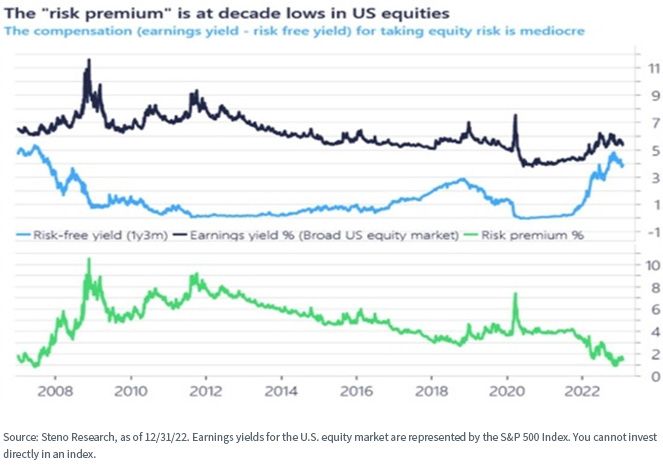

Despite recessionary fears and an uncertain path for monetary policy, investors have embraced equity risk to begin 2023. Some measures of the equity risk premium, or the additional return compensation investors require to hold risky assets (like equities), are now hovering around lows last observed during the middle of the global financial crisis in 2008.

Steno Research recently framed the equity risk premium by analyzing the spread between the earnings yield for the U.S. equity market and those available on U.S. Treasury securities. The Federal Reserve’s rate hike campaign over the past year has trimmed this spread to below 2%.

Equity investors now face a unique question. Are bonds a direct threat to equity allocations just because there is meaningful income back in fixed income, where investors can earn less volatile yields?

If so, how long will these yields last? The short end of the yield curve tends to track Fed policy more closely, and the current inversion of the overall curve suggests that today’s higher rates are not expected to last over the medium- to longer-term once the Fed pivots to rate cuts.

Real Yields Are Key

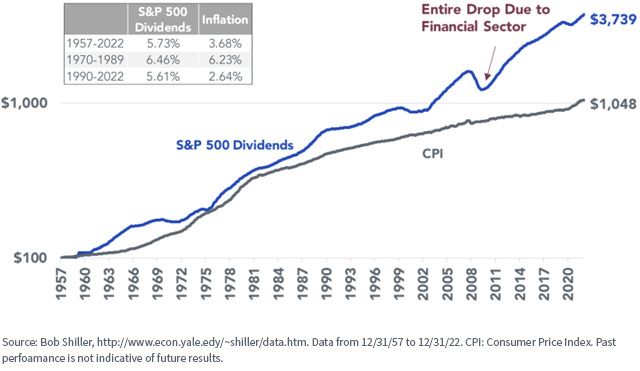

The Fed has been hiking rates because of inflation. We believe stocks are the best long-term hedge for inflation due to the historical risk premium they have exhibited above inflation, but also because companies are able to pass along rising input costs over time to their customers.

This pricing power is evidenced by the long-term earnings and dividend growth of the market, outpacing inflation. Even during the 1970s and 1980s, when inflation averaged over 6% for two decades, dividend growth kept pace with inflation.

Over shorter periods, when the Fed enacts tight monetary policy to combat inflation, stock prices ultimately suffer from higher interest rates, as they did in 2022. But over the long term, equities have innate inflation-hedging characteristics that help compensate for inflationary pressures. For this reason, we view them as real assets.

That compels us to analyze real rates and real bond yields, as opposed to nominal ones, when we observe different measures of equity risk premiums.

We prefer to compare equity earnings yields (or the reward for investors) over those on risk-free, inflation-indexed bonds, like TIPS in the U.S.

This model of equity risk premium is not a perfect guide for markets, but as Professor Siegel explains in the sixth edition of Stocks for the Long Run:

Nevertheless, when earnings yields and real bond yields are at extremes, that often signals a turning point. At the peak of the dot-com bubble in 2000, the earnings yield on stock was just over 3 percent, while the 10-year TIPS bond yielded over 4 percent. This led to an extraordinarily rate negative risk premium (earnings yield minus TIPS yield) and reliably signaled the subsequent decline in equity prices.

By these standards, equity risk compensation is not as dire as implied by the original chart from Steno Research.

Using both trailing and forward S&P 500 earnings yields, less the 10-Year TIPS yield, risk premiums are right at their longer-term averages from the past 25 years.

Contrast this with the tech bubble in 2000, when the earnings yield spread over TIPS turned negative, and it’s apparent that today’s markets have approximately 500 basis points in additional compensation for U.S. equities relative to TIPS.

S&P 500 Equity Risk Premium (Estimated Earnings Yield – 10-Year TIPS Yield)

S&P 500 Equity Risk Premium (Trailing Earnings Yield – 10-Year TIPS Yield)

For much of the last decade, equities comfortably outpaced bonds with rates near 0% and little additional yield to be found in riskier fixed income sectors. This period became known as the “TINA” era, suggesting “There Is No Alternative” to owning stocks when rates are low and yield is scarce.

While there are now some real alternatives—with income back in short-duration fixed income—by historical standards, today’s equity risk premium remains quite reasonable relative to inflation-indexed bonds.

Categories

About the contributors

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.