The Price Is Right

Reports on inflation have essentially been “stealth-like” and have garnered little to no attention. Arguably, throughout most of 2019, inflation has had no reason to grab the headlines, but let’s be thought-provoking for a minute—should investors be concerned about whether the price is right?

The most broadly watched inflation gauge is the Consumer Price Index (CPI). This monthly report provides two headline figures: overall inflation at the retail level and this same gauge excluding food and energy (core CPI). I know we have to put gas in our cars, heat our homes and certainly eat, but the bond market’s focus lies with the core measure. Let’s take a look at recent trends to see if there is anything of note.

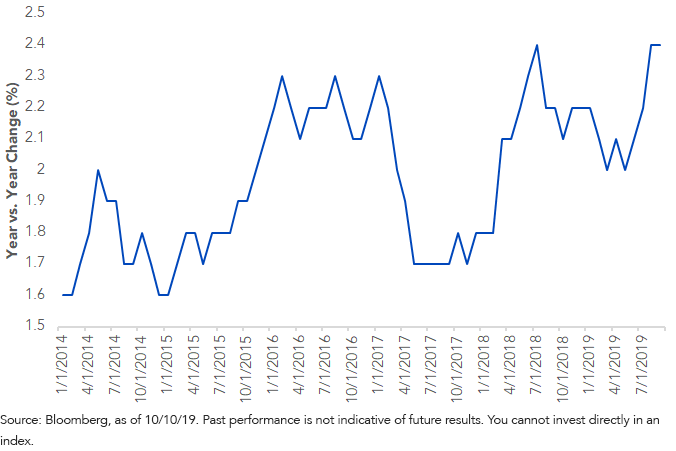

U.S. CPI ex-Food & Energy

The above graph highlights the year-over-year percent change in core CPI over the last five years. Without a doubt, it has had its “ups and downs,” to say the least. I want to focus on the 2019 trend. As you can see, after dropping down to the +2.0% level, core CPI has been on ascending trajectory of late, rising three straight months before leveling out at its September reading of +2.4%. Interestingly, when I bring this fact up in meetings, etc., the audience is not aware of this occurrence. Fun fact: The last time the annual rate of increase for CPI ex-food & energy was above its current reading was in 2008.

Will the Federal Reserve (Fed) or the bond market get “high anxiety” over this trend? More than likely, no, but let’s see if there is any underlying trend to watch out for. The core component is made of goods and services. The core services grouping has registered four consecutive solid monthly showings (coinciding with the aforementioned upward trend), but core goods has been a bit more volatile and actually fell -0.3% in September. This decline may get reversed in the coming month or two, however, as the decline reflected an outsized decrease of -1.6% in the used cars and trucks category. Typically, a negative reading such as this tends to get either reversed or, at a minimum, not replicated in future reports. In other words, it seems plausible an upcoming year-over-year core CPI reading could move above its current level.

Conclusion

The Fed-preferred core inflation measure, personal consumption expenditures excluding food and energy, has continued to remain under the policymaker’s +2% threshold. In fact, the September FOMC minutes cited muted inflation as a justification for the recent rate cut. Thus, I’m not about to go trick or treating in my inflation bogeyman costume, but just the same, maybe it wouldn’t hurt to keep an eye on inflation trends going forward.

Unless otherwise stated, data source is Bloomberg, as of October 11, 2019.

Share & Comment

Popular Posts

Categories

Related Links