Don’t Go Chasing Waterfalls

What a whirlwind week for the bond market. Investors were greeted with an historic Fed rate hike, another 40-year high for inflation and a second consecutive negative quarterly reading for real GDP—in other words, a technical recession. There’s no doubt these conflicting storylines present a confusing backdrop for fixed income investors when positioning their bond portfolios. My advice: don’t go chasing waterfalls.

Prior to last week’s disappointing Q2 real GDP report, there had been increasing discussion about whether rates, such as the UST 10-Year yield, had peaked and was it now time to ‘go longer duration.’ Obviously, the back-to-back negative readings for the economy gave that narrative something of a jump-start, as the UST 10-Year yield continued its descent to lower territory.

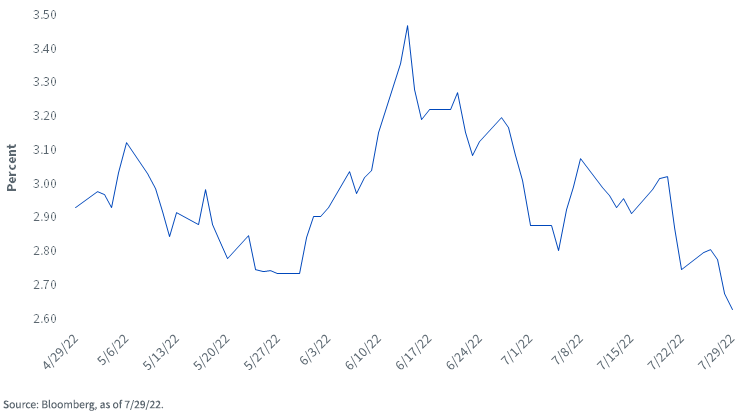

There are two very important considerations to keep in mind when addressing this question. Obviously, the first element is whether bond yields will rise again from current levels, fall further or, at best, remain stable. My concern revolves around the incredible volatility and whipsaw pattern the UST 10-Year yield has shown in the last three months. As highlighted by the graph below, investors have witnessed the UST 10-Year yield go from close to 3.25% back down to 2.75%, only to see it then rise to about 3.50%. It is now back to around 2.60%.

U.S. Treasury 10-Year Yield

Typically, this is not the type of volatility an investor wishes to see in their bond portfolio. And I’m in the camp that believes this elevated volatility will remain a part of the investment landscape during the second half of this year.

Against this backdrop, one has to wonder if the UST 10-Year yield has gotten ahead of itself a bit. From a monetary policy perspective, the Fed seems poised to continue raising rates this year. Quantitative tightening (QT) will soon be kicking into high gear, and as we’ve continued to see, inflation will more than likely remain ‘sticky.’ And, if you believe the latest economists’ projections, real GDP could bounce back into positive territory in Q3. Most estimates are placing growth for this quarter around the 2% vicinity.

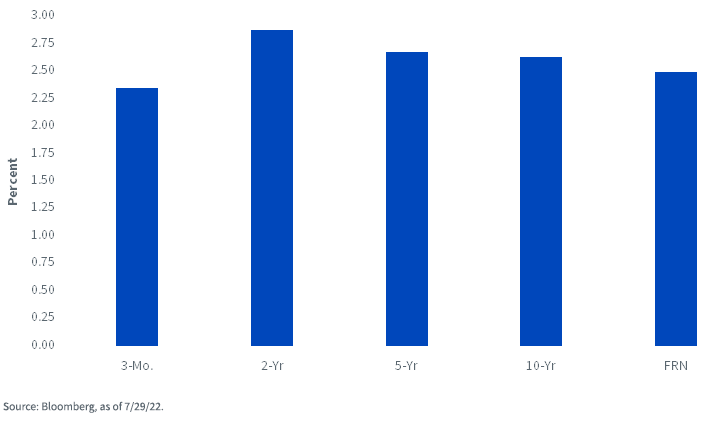

U.S. Treasury Yields

The second consideration is whether an investor is being compensated for the potential added interest rate risk by moving into longer duration. Quite a lot of attention has been centered on how flat and/or inverted the shape of the Treasury yield curve has become (see above). In other words, the present UST 10-Year yield level offers little, if any, cushion for potential mistakes that could result in another move to the upside.

Interestingly, UST floating rate note (FRN) yields have now closed the gap. They are currently higher than 3-month t-bills and within striking distance of the 5- and 10-Year maturities. To provide perspective, the UST FRN yield is only 13 basis points (bps) below the UST 10-Year rate but carries a duration profile of just one week.

Conclusion

With the Fed expected to continue raising rates during its three remaining FOMC meetings this year, it is very likely UST FRN yields could match, or even exceed, some fixed coupon securities along the Treasury yield curve in the not-too-distant future. Against this backdrop, investors may want to consider the risk/reward profile of their fixed income positioning. The WisdomTree Floating Rate Treasury Fund (USFR) offers investors a means of investing in the U.S. Treasury floating rate note space.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new and the amount of supply will be limited. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.Share & Comment

Popular Posts

Categories

Related Links