DLN

U.S. LargeCap Dividend Fund

Published July 8, 2026

Global Chief Investment Officer

Twenty years ago, WisdomTree launched its first family of exchange-traded funds built on a simple but powerful idea: investors should own companies based on their economic importance rather than their stock market popularity.

At the time, this was a bold departure from conventional indexing.

Most indexes weighted companies by market capitalization. As stocks became more expensive, they automatically received larger weights. As stocks became cheaper, their weights shrank. The market itself determined portfolio construction.

WisdomTree’s founders believed there was a better way.

Drawing on what Professor Jeremy Siegel would later describe as the “Noisy Market Hypothesis,” WisdomTree built indexes around fundamental measures of corporate value. For dividend-paying companies, ownership would be determined by the cash dividends companies paid to shareholders rather than by changing market sentiment.

That principle became the foundation for WisdomTree’s first 20 ETFs.

The launch represented one of the earliest attempts to bring alternative and fundamentally weighted indexing into the ETF structure. While the industry was largely focused on tracking traditional benchmarks, WisdomTree sought to create portfolios that systematically rebalanced toward value and away from overvaluation.

The flagship U.S. Total Dividend Fund (DTD) and U.S. LargeCap Dividend Fund (DLN) embodied this philosophy. Companies paying larger aggregate dividends received larger weights. When stock prices rise faster than dividend growth, weights are rebalanced back to each company’s Dividend Stream—its proportional share of aggregate cash dividends paid. When prices fell relative to dividends, weights are rebalanced back up to their dividend representation. This disciplined process effectively created a mechanism for buying when prices fell below fundamental value and selling when stocks became more expensive measured versus their fundamentals.

The approach was rooted in the belief that markets are not always perfectly efficient. Prices can become disconnected from fundamentals. Investor enthusiasm and market sentiment push securities above intrinsic value, while fear drives prices below it. By anchoring portfolios to dividends, WisdomTree sought to harness those market inefficiencies rather than simply follow them. Market cap weighted indexes do the opposite, simply riding trends higher and lower.

Over the last twenty years, investors experienced nearly every market environment imaginable: the Global Financial Crisis, the post-crisis growth rally, the rise of mega-cap technology, the pandemic shock, inflation’s return, trade-war-driven volatility, and the emergence of artificial intelligence as a dominant investment theme.

Through each cycle, dividend-weighted strategies provided a different lens on equity investing.

The original WisdomTree indexes did not attempt to predict which stocks would outperform next. Instead, they systematically linked portfolio weights to measures of corporate fundamentals and rebalanced back to those fundamentals systematically. That philosophy remains at the core of many WisdomTree strategies today.

Our flagship large cap ETF in this family is the WisdomTree U.S. LargeCap Dividend Fund (DLN), which at $6 billion is the largest AUM ETF of the original U.S. focused launches from 20-years ago. Let’s look at how the strategy played out in the large cap space and how it compares to other traditional value strategies.

First a primer on the index construction and rebalance process.

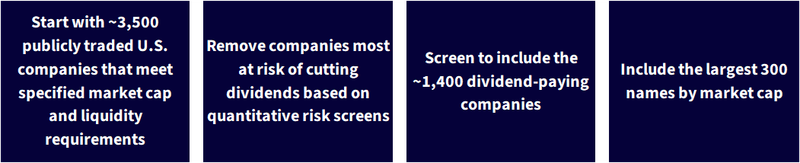

Figure 1: Investment Process: U.S. Large Cap Dividends

One of the appealing features of dividend weighting is that it does not place an arbitrary cutoff on the definition of growth or value stocks—it includes all the dividend payers and just shifts weight to those with more dividends.

In the last 20-years, during a time growth indexes dominated value indexes, DLN was able to out-perform the traditional value cuts because of its more inclusive nature.

Indexes that sort on price-to-book—the Russell Value indexes being the prime historical example—rarely included technology stocks, whose asset-light business models naturally produced low book values.

But many of the leading technology companies have been dividend payers.1

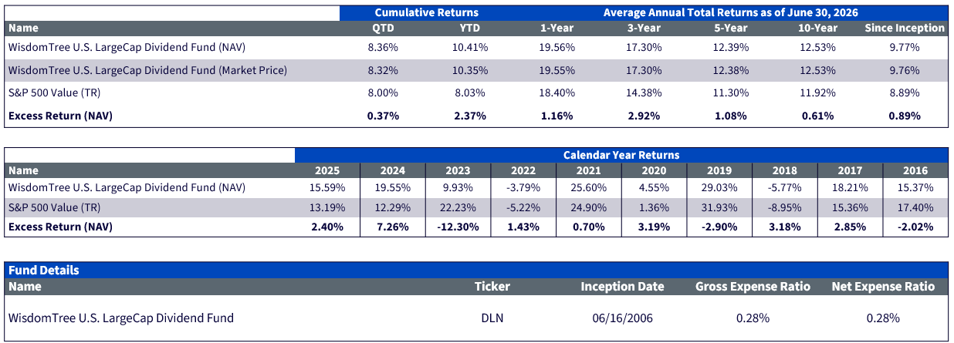

Judged over the last 20-years, DLN out-performed the S&P 500 Value Index by over 80 basis points per year over 20-years.

Figure 2: WisdomTree U.S. LargeCap Dividend Fund Performance

Source: WisdomTree, as of 6/30/26. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

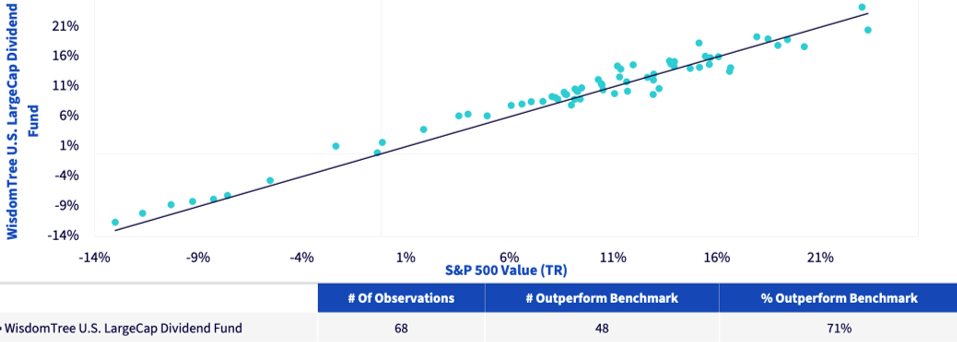

Just as important as the long-term track record is the rolling period performance. We now have nearly 70 rolling 3-year time periods- and DLN out-performed the S&P 500 Value Index 71% of the rolling periods.

There were 20 periods where it under-performed, and generally the under-performance came after extremely strong returns for the benchmark and DLN had a modestly lower beta to the very strong upside. Providing cushion in more challenging times is one feature of dividend investing.

Figure 3: Manager Consistency 3-Year Rolling

Source: WisdomTree, S&P, as of 5/31/2026. Dots represent trailing 3-year rolling returns of the WisdomTree U.S. LargeCap Dividend Fund and the S&P 500 Value (TR) using quarterly observations. Inception date for the fund was 6/16/06. Returns for the fund based on net asset value. Returns for the benchmark index based on total returns. Past performance is not indicative of future results. You cannot directly invest in an index.

Still Paying Dividends

What began with 20 ETFs has grown into a global asset management platform spanning equities, fixed income, commodities, currencies, alternatives and digital assets. Yet the foundational idea remains remarkably consistent: investment portfolios should be anchored in economic reality rather than market excitement.

Twenty years later, the original WisdomTree dividend strategies continue to offer an important reminder. Markets are powerful pricing mechanisms, but they are also influenced by human behavior. A disciplined process that connects ownership to fundamentals can provide a durable framework for long-term investors.

The first 20 funds were not simply the beginning of a company. They represented the launch of a new approach to indexing—one that continues to shape how investors think about fundamentals, valuation, and portfolio construction.

1 Sources for bullet points: WisdomTree, FactSet, MSCI, as of 6/30/2026.

There are risks associated with investing, including possible loss of principal. The Fund invests primarily in the securities of large-capitalization companies. As a result, the Fund’s performance may be adversely affected if securities of these companies underperform securities of smaller capitalization companies or the market as a whole. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.