A Rebalance Review for U.S. Large-Cap Dividends

Published December 31, 2025

Equity Strategist

Key Takeaways

- December’s rebalance saw modest but directional sector shifts, with Information Technology gaining most notably in both the WisdomTree U.S. Dividend Index (WTDI) and the WisdomTree U.S. LargeCap Dividend Index (WTLDI).

- WTDI and WTLDI continue to exhibit value-like tilts versus market cap benchmarks, with key over-weights to dividend-heavy sectors like Energy and Consumer Staples, and notable under-weights to growth-oriented sectors such as Communication Services and Information Technology.

- Both Indexes delivered improved fundamentals post-rebalance, including lower P/E ratios and higher dividend yields, reaffirming the power of WisdomTree’s dividend-weighted strategy to enhance valuation and quality metrics.

Each December, WisdomTree's U.S. dividend Indexes undergo their annual rebalance, an exercise designed to reaffirm our core philosophy: that dividends are a disciplined and transparent measure of corporate fundamentals. Reweighting U.S. equities by their dividend payments, a method involving the total pool of dividends that we call the Dividend Stream®, helps the stock basket evolve with the changing composition of the dividend-paying portion of the equity market.

Two of our flagship domestic dividend strategies, the WisdomTree U.S. Dividend Index (WTDI) and the WisdomTree U.S. LargeCap Dividend Index (WTLDI), share nearly identical construction rules, with the primary distinction being size segmentation. Because of their parallel methodologies, their rebalances tend to follow similar directional patterns across sectors and fundamentals. This year was no exception.

Below, I summarize the major takeaways from the 2025 rebalance across sector shifts, benchmark-relative tilts, and valuation and quality characteristics.

Sector Shifts: Modest Adjustments with a Common Theme

Both WTDI and WTLDI saw incremental minor sector adjustments as the rebalance reassigned weights based on each constituent's proportionate share of the U.S. Dividend Stream®.

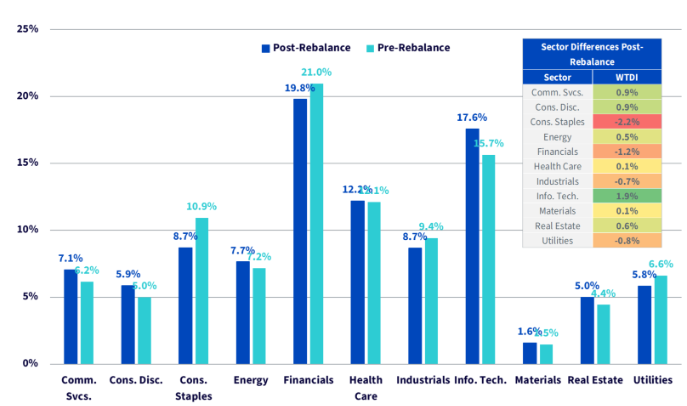

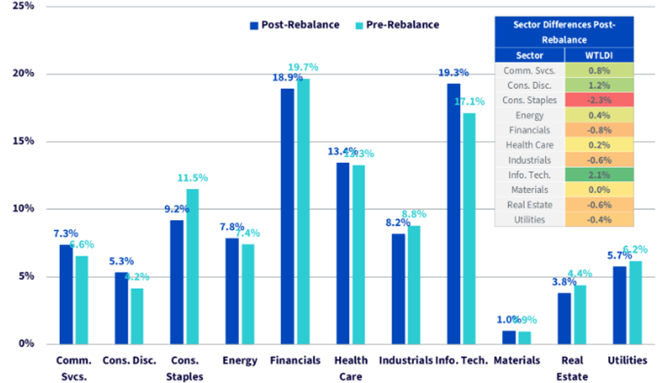

Across both Indexes, Communication Services, Energy and Information Technology exhibited modest increases. Information Technology was the largest gainer in both baskets at about 2% each, primarily due to the addition of Broadcom (AVGO) (see below for more detail).

Financials, Industrials and Utilities all showed modest decreases. Consumer Staples showed the most notable decline, losing over 2% of its pre-rebalance exposure in both Indexes, which was distributed across a broader swath of companies.

Overall, the changes were measured, which is typical of the mature, dividend-paying equity universe within the U.S. and among large caps specifically, but directionally coherent between the two Indexes.

WisdomTree U.S. Dividend Index (WTDI): Sector Allocations After Annual Rebalance

WisdomTree U.S. LargeCap Dividend Index (WTLDI): Sector Allocations After Annual Rebalance

Sources: WisdomTree, FactSet as of 11/30/25. You cannot invest directly in an index.

Benchmark Comparisons: Value-Like Tilts Persist

As expected for fundamentally weighted dividend strategies, both WTDI and WTLDI continue to maintain value-like exposures relative to market cap-weighted benchmarks.

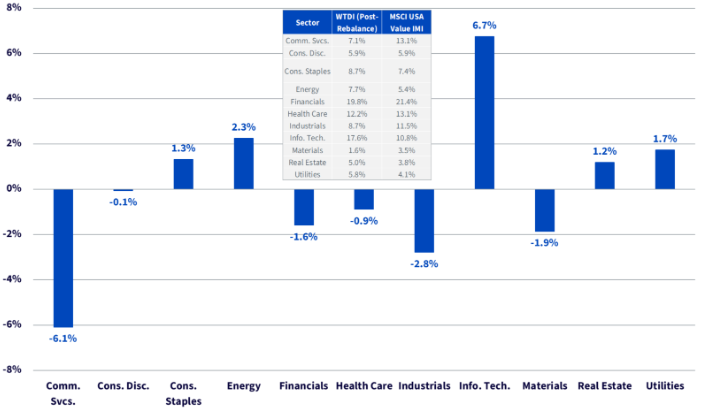

WTDI remains under-weight in high-growth sectors of U.S. markets that are less likely to have large dividend yields, such as Communication Services (-6.1%). The underexposure is offset by over-weights to traditional value and dividend-paying heavyweights, like Energy (+2.3%), Consumer Staples (+1.3%) and Utilities (+1.7%).

The most notable sector differential, however, is a 6.7% over-weight to Information Technology, reflecting how WTDI captures more dividend-paying companies in a sector largely devoid of traditional value stocks.

WisdomTree U.S. Dividend Index (WTDI): Post Rebalance Sector Exposure vs. MSCI USA Value IMI Index

Sources: WisdomTree, MSCI, FactSet as of 11/30/25. You cannot invest directly in an index.

This benchmark-relative footprint reinforces WTDI's role as a diversified, fundamentals-anchored alternative to traditional broad-market exposures.

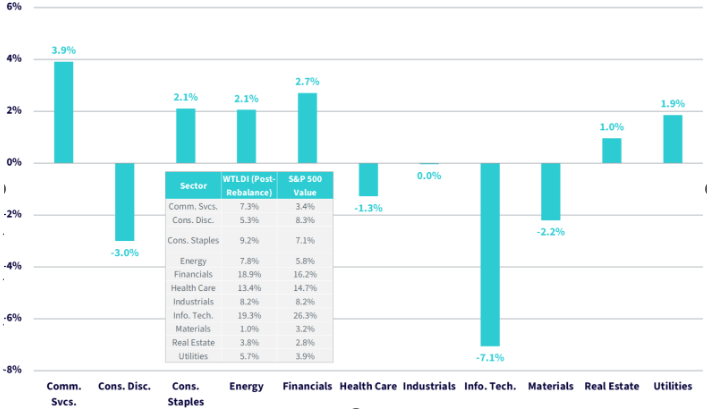

WTLDI exhibits similar tilts compared to the S&P 500 Value Index, which exclusively captures the large-cap value area of the U.S. equity market. Over-weights to Consumer Staples (+2.1%), Energy (+2.1%) and Financials (+2.7%) offset under-weights to Consumer Discretionary (-3.0%) and Information Technology (-7.1%).

These tilts help maintain diversification from conventional value-factor approaches, driven by our dividend-weighted discipline rather than valuation screens alone.

WisdomTree U.S. LargeCap Dividend Index (WTLDI): Post Rebalance Sector Exposure vs. S&P 500 Value Index

Sources: WisdomTree, S&P, FactSet as of 11/30/25. You cannot invest directly in an index.

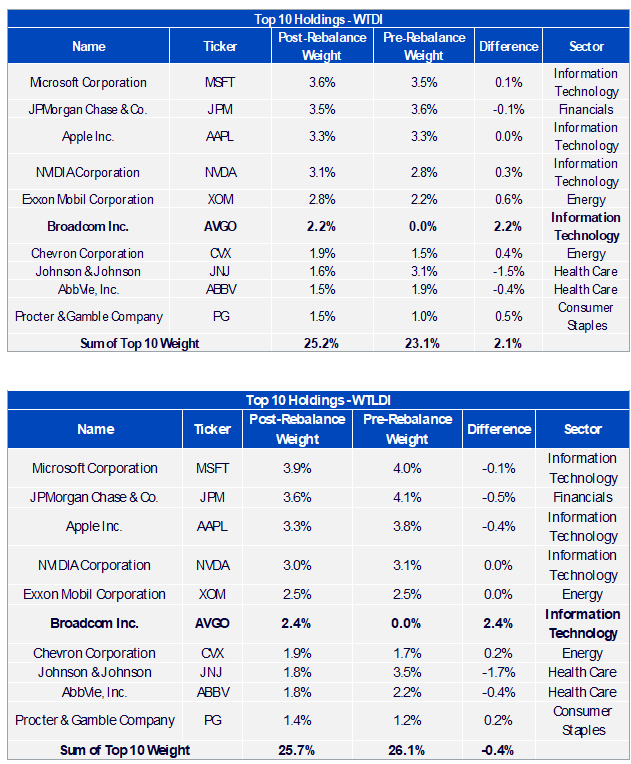

Top Holdings Remain Constant, with One Notable Exception

The top 10 holdings across both Indexes after the rebalance were identical in name and order, though with modestly different weights based on the methodology differences between the mandates. This reflects stability among the top dividend payers in the overall Dividend Stream®, which provides a healthy dose of consistency.

The total weight in the top 10 names in both Indexes is about 25%, which marks a negligible change in WTLDI and a slight increase of 2% in WTDI.

Among companies, however, there was one notable addition. This year, Broadcom, Inc. (AVG) was readded to both Indexes after being screened out in 2024 on our Composite Risk Screen (CRS) parameters.

Broadcom pays about $10.6 billion in total dividends, which makes it the ninth-largest payer in the U.S. equity market. It's also grown its dividend by over 11% between 2024 and 2025, which is atypical and especially valuable for a Technology company. This may be a valuable reintroduction to both Indexes in 2026.

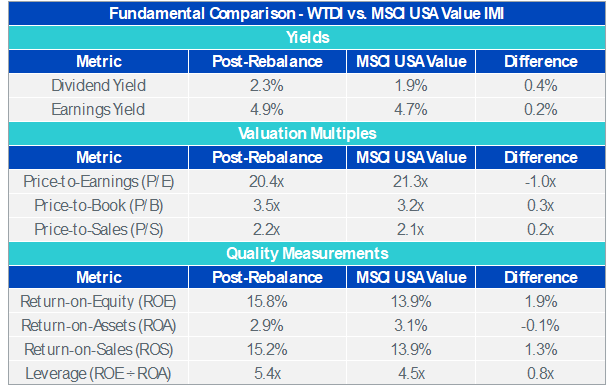

Fundamental Characteristics: Valuation Sensitivity Reaffirmed

One of the defining features of WisdomTree's annual rebalance is its ability to systematically readjust valuations, yields and quality measurements by reconstituting the equity basket. This often results in improved fundamentals once we identify the emerging leaders and initiators among the dividend-paying universe while continuing to reward the mainstay companies of our dividend mandate.

As usual, both Indexes saw fundamental improvements.

Across WTDI and WTLDI, price-to-earnings (P/E) ratios modestly declined by about 0.5 times. Price-to-sales (P/S) ratios also declined across both. Quality metrics also remained broadly stable with return on equity (ROE) and return on assets (ROA) largely unchanged.

However, their advantages versus market cap-weighted U.S. benchmarks are more visible.

WTDI improved on the P/E multiple of the MSCI USA IMI Value Index by a full point, resulting in a 0.2% boost to its earnings yield. ROE, our preferred barometer of quality and profitability, also improved by nearly 2%. Most importantly, however, there is also a 40-basis point (bp) increase in dividend yield, which is critical to our dividend mandate.

Sources: WisdomTree, MSCI, FactSet as of 11/30/25. You cannot invest directly in an index. Past performance does not guarantee future results.

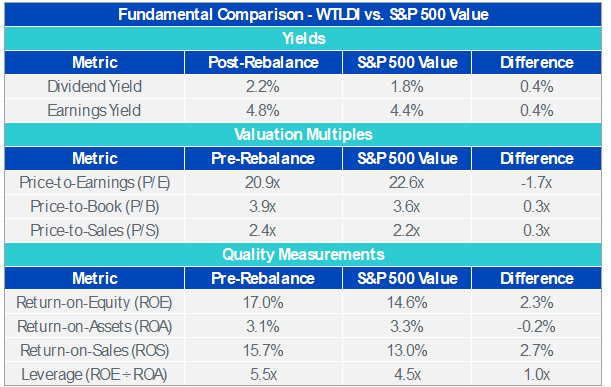

WTLDI exhibited more muted impacts, but that's largely because it's already being compared to a value benchmark in the S&P 500 Value. Still, the fundamental improvements deserve attention.

WTLDI reduced the trailing P/E ratio by nearly two turns, while adding 40 bps apiece to dividend yield and earnings yield. It also delivered a notable pickup in ROE and return on sales (ROS) by over 2% each.

Sources: WisdomTree, S&P, MSCI, FactSet as of 11/30/25. You cannot invest directly in an index. Past performance does not guarantee future results.

Once again, the annual rebalance delivered fundamental advantages that would be absent, or muted, in a market cap-weighted index, highlighting the importance our dividend discipline beyond corporate payouts.

Dividend Weighting Continues to Do Its Job

The 2025 rebalances for WTDI and WTLDI illustrate why WisdomTree continues to rely on fundamental weighting. The Dividend Stream®-weighting process provides measured sector realignments, typical value tilts and a fundamental profile that improves on valuation multiples and quality metrics. Most importantly, it delivers a rules-based approach that adapts to changes in corporate dividend behavior.

Categories

About the contributor

Equity Strategist

Brian Manby is an Equity Strategist at WisdomTree and part of the Investment Strategy team.

He is responsible for developing and communicating equity market insights, investment themes, and portfolio strategies that support the firm’s ETF and investment solutions platform. He evaluates sectors, valuations, fundamentals and equity styles to identify investment opportunities and provide actionable perspectives to clients and advisors. He also helps investors understand how WisdomTree’s equity strategies can be used to achieve long-term investment objectives in evolving market environments.

Brian joined WisdomTree in October 2018 as an Investment Strategy Analyst after a few years as a Consultant for FactSet Research Systems, Inc. He earned a B.A. in Economics and Political Science from the University of Connecticut in 2016 and has been a Chartered Financial Analyst since 2022.