DGRW

U.S. Quality Dividend Growth Fund

Published June 25, 2026

Associate, Investment Strategy

NVIDIA’s quarterly earnings reports are usually marquee events for equity markets, and its first-quarter results announcement on May 20 was no different. In addition to reporting record revenue, strong profit margins, and triple-digit year-over-year increases in Generally Accepted Accounting Principles (GAAP) and non-GAAP diluted earnings, it announced one of the greatest dividend growth stories equity markets have ever seen.

The most valuable company in the world, and artificial intelligence (AI) bellwether, announced that it would immediately raise its quarterly cash dividend from $0.01 to $0.25 per share of common stock, a 2,400% increase. With roughly 24 billion common equity shares outstanding, NVIDIA will be on track to pay $24 billion in cumulative dividends during its fiscal year, vaulting it into second place among the largest dividend payers in U.S. equity markets.

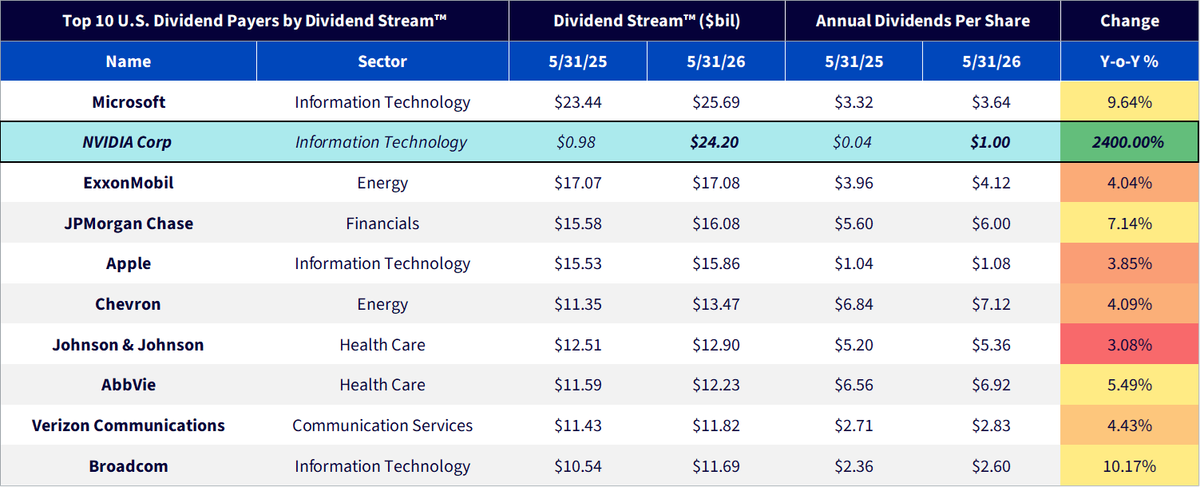

Figure 1: Top 10 U.S. Dividend Payers by Dividend Stream™ After NVIDIA’s Announcement

Source: WisdomTree, MSCI, FactSet, as of May 31, 2026. Dividend Stream = Indicated dividends per share x shares outstanding. Universe based on the MSCI USA Index.

NVIDIA will now only trail Microsoft among U.S. dividend leaders, as its cumulative annual payout of $25.69 billion narrowly maintains first place. The $17 billion in dividend payouts from ExxonMobil, now the third-largest dividend payer, was immediately dwarfed by NVIDIA’s historic increase.

NVIDIA’s announcement further augments the changing composition of the U.S. dividend landscape, as three of the top five dividend-payers now operate within the Information Technology sector (Apple ranks fifth, at $15.86 billion), with a fourth (Broadcom ($11.69 billion) rounding out the top ten.

Historically, the idea of technology companies paying dividends at the expense of potentially reinvesting in their own growth was antithetical to prevailing wisdom, but that no longer holds.

The 2026 U.S. dividend environment reminds us that dividend-centric investment strategies should not rely on rigid frameworks that are becoming increasingly obsolete. Instead, they should utilize flexible, adaptive approaches that evolve with the market, not in spite of it.

Challenging Mainstream Thinking

NVIDIA’s dividend increase reminds us of an important premise for dividend growth investing: Long, consistent histories of dividend growth are not a precondition for further growth, nor protection from a reduction or suspension. More importantly, fixating on yesterday’s leaders ignores today’s initiators and tomorrow’s growers.

The WisdomTree U.S. Quality Dividend Growth Fund (DGRW) debunks the notion that dividend growth history should dictate inclusion investment strategies focused on dividend growth today. Similarly, it counters the idea that a dividend payment is inherently stable simply because of past growth.

No Backward-Looking Growth Requirement

Unlike other dividend growth equity funds, DGRW’s methodology contains no trailing dividend growth requirement that would otherwise ignore NVIDIA and recent Information Technology initiators like Alphabet and Meta. Because they are all high-quality companies (based on our measures of return-on-equity (ROE), return-on-assets (ROA), trailing and forward-looking earnings growth and more), DGRW maintains exposure to all three companies, which are all success stories in their own right:

Growth History Does Not Equal Growth Potential

As the oft-repeated saying in our industry goes, “past performance is not indicative of future results.” But when it comes to dividends, the past is exactly what conventional dividend growth strategies rely upon to justify the perceived stability of their constituents’ payouts going forward. Put another way, they believe that a historical dividend growth trend should necessarily persist.

DGRW challenges conventional thinking and tries to accomplish dividend growth and stability more intelligently. Rather than assuming that a dividend’s past is prologue, it screens for dividend-paying companies that score highly on a variety of quality and growth metrics to identify companies with ample potential to grow those dividends in the future. Look no further than NVIDIA as a validating example.

DGRW relies on quality for its dividend protection because metrics like ROE, ROA and earnings and sales growth across time periods are indications of healthy, resilient, efficient businesses. Stable operations naturally reduce operating uncertainty, which should promote greater consistency in operating results. Since dividends are a discretionary award from management to shareholders, there is no obligation for them to ever be paid, which often puts them under threat when operating results sour.

Quality is therefore our preferred antidote to dividend threats. To the extent we can reduce operating uncertainty within our methodology, we can partially mitigate the uncertainty about the viability of a dividend going forward. That’s how DGRW thrives.

WisdomTree has always sought to deliver more intelligent investment intuition within our products. That’s why we paired ROA along with ROE in our quality framework to counter attractive profitability metrics purely inflated by financial leverage. That’s why we rejected the mainstream thinking that historical dividend growth is a prerequisite for future growth. And that’s why we’ve created a product that adapts to the changing dividend market, rather than resists it. That’s DGRW.

There are risks associated with investing, including possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Quality Dividend Growth Fund

Associate, Investment Strategy

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.