DEM

Emerging Markets High Dividend Fund

Published April 21, 2026

Global Head of Research

Nearly nineteen years is a long time in emerging markets. It spans both commodity price supercycles and commodity price collapses, the rise of China, the so-called ‘taper tantrum,’1 a pandemic shock and recovery, and a new era defined by geopolitics and supply chain realignment.

Through all of it, the WisdomTree Emerging Markets High Dividend Fund (DEM) has been live, navigating environments that have, at times, rewarded growth, punished value and then shifted to the opposite. Ultimately, longevity matters. It offers an observable record of how a rules-based, income-focused approach behaves across cycles. At its core, DEM is built on a simple but often underappreciated idea: in emerging markets, dividends can be a powerful signal of discipline and shareholder alignment. Starting from that premise, the strategy tilts toward companies that are not just attractively valued, but also returning capital along the way, creating a distinct profile that looks meaningfully different from traditional benchmarks, such as the MSCI Emerging Markets Index.

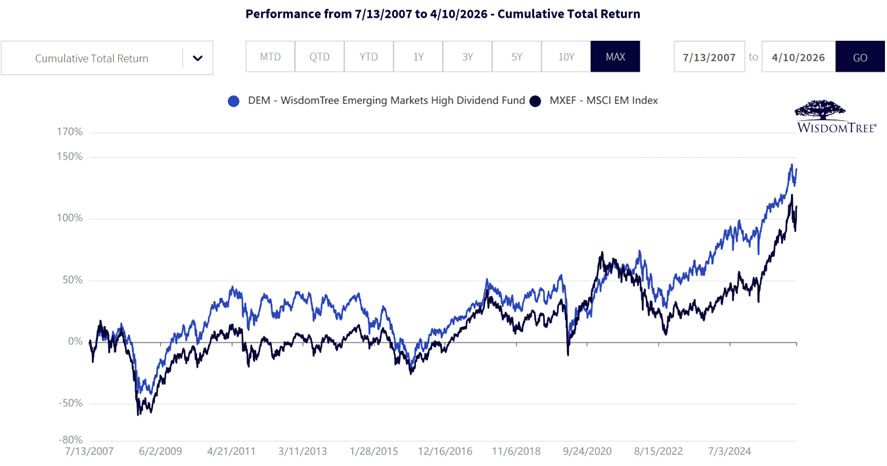

In Figure 1a shows:

Figure 1b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically, data is from the PATH Fund Comparison Tool, accessed as of April 12, 2026, but showing returns for the period ended April 10, 2026 for Figure 1a and March 31, 2026 for 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

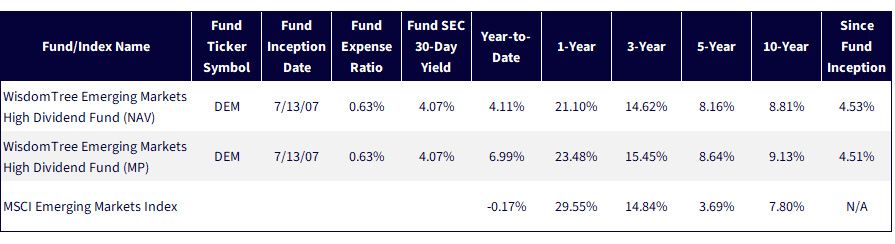

At the core of DEM, which is designed to track the total return performance, before fees and expenses, of the WisdomTree Emerging Markets High Dividend Index, is a deliberate decision: prioritize companies returning cash to shareholders with higher overall dividend yields and weight them by the scale of those distributions.

Importantly, this is not a screen layered on top of a traditional market-cap framework, but rather the foundation of the strategy itself. In emerging markets, where capital allocation discipline can vary widely, dividends offer a tangible signal. They reflect, in our view, potential signals around profitability, governance and a willingness to share earnings rather than simply reinvest or retain them.

By weighting companies based on total cash dividends paid, DEM systematically tilts toward firms with both the capacity and the commitment to generate income. The result is not subtle. It is a structurally higher yield profile that persists across time, shaping both the income characteristics investors receive and the types of exposures they ultimately hold, often leading to a portfolio that looks meaningfully different from traditional benchmarks.

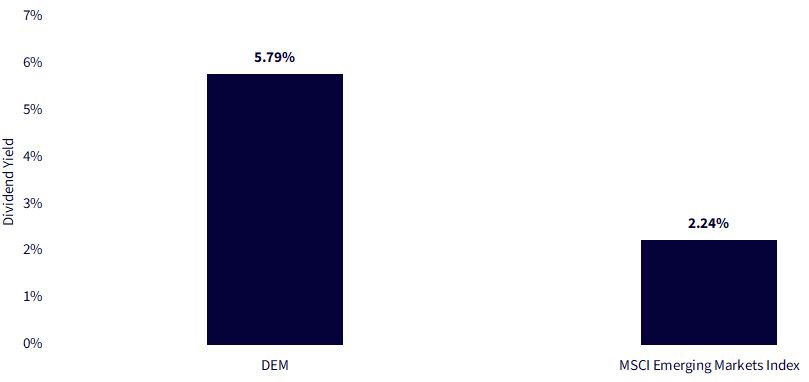

Figure 2 shows the ‘dividend yield difference’ between DEM and the MSCI Emerging Markets Index benchmark, quantified as of March 31, 2026. The picture may not always look like this, but we do note that this is driven by underlying methodology at its core.

Sources: WisdomTree, Morningstar and FactSet, with data as of March 31, 2026. Subject to change. Past performance is not indicative of future results.

When reviewing the total return performance of DEM against that of the MSCI Emerging Markets Index, we recognize that no strategy with almost 19 years of live history should be expected to outperform at all times. The underlying WisdomTree Emerging Markets High Dividend Index has held a consistent focus on relatively higher dividend yielding emerging market stocks. As market leadership shifted and changed, we know that these types of stocks also did not always outperform lower dividend yielding, more growth-oriented equities.

The Strengths of a High Dividend Focus in Emerging Markets

DEM's strength showed up most clearly when emerging markets behaved as a broad, internally driven asset class. In those periods, its design, such as stock selection in India, selective exposure within China, and meaningful participation in Brazil combined with strong stock selection in consumer and communication-oriented businesses. The result is a portfolio that captures domestic growth, benefits from higher-quality balance sheets, and compounds steadily over time.

The Weaker Moments of a High Dividend Focus in Emerging Markets

By contrast, the MSCI Emerging Markets Index benchmark tended to lead when performance narrowed and became dominated by the technology supply chain. Here, DEM's underweight to Taiwan and South Korea, effectively an underweight to semiconductors, became a headwind, amplified by a lower allocation to Information Technology overall. These are not accidental gaps but the byproduct of a different design philosophy: one that prioritizes diversification, income, and quality over concentration in a single sector or region.

The insight, in our opinion, is that both outcomes are logical. DEM is built to win over full cycles, particularly when leadership broadens, while the MSCI Emerging Markets Index has exceled in more concentrated, tech-led environments. Understanding that trade-off is essential to setting the right expectations.

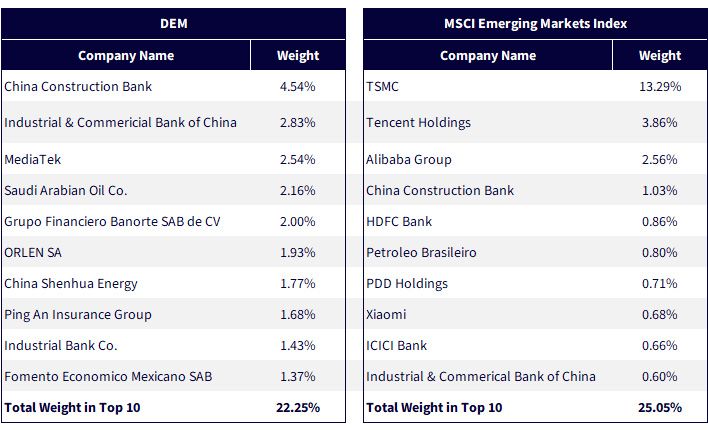

I phrased the ‘conclusion heading’ as a question because as I was looking over the numbers, I saw something that I was surprised by. The reason for my surprise was not that anything was ‘wrong’ or ‘incorrect’, but rather I just hadn’t realized how much TSMC, the company, had run in terms of its performance, thereby increasing its market capitalization relative to the rest of emerging market equities.

The MSCI Emerging Markets Index is weighted by float-adjusted market capitalization. Simply put, larger market cap companies with greater amounts of shares that regularly trade should see larger exposures.

But, as of March 31, 2026, TSMC had a weight above 13% in the MSCI Emerging Markets Index benchmark. I know about TSMC and how important this company is to the most advanced semiconductors on the planet. It makes sense that this is one of the world’s largest companies. But wow, I was surprised to see a single weight above 13% in this benchmark. Figure 3 shows the top 10 holdings of DEM versus the MSCI Emerging Markets Index to emphasize this point. I will clearly state that none of this tells us, with certainty, which of these two strategies will outperform going forward. However, we do know that many investors already have a lot of so-called ‘AI exposure’ and if they are thinking about a strategy that tilts away from that in emerging markets, DEM may warrant consideration.

Sources: WisdomTree, Morningstar, FactSet, with data as of with data as of March 31, 2026. Subject to change.

Source: Sahay, R., Arora, V., Arvanitis, T., Faruqee, H., N’Diaye, P., & Mancini-Griffoli, T. (2014, October 3). Emerging market volatility: Lessons from the taper tantrum (IMF Staff Discussion Note SDN/14/09). International Monetary Fund.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in emerging, offshore or frontier markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation, intervention and political developments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Emerging Markets High Dividend Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.